The term “Plaid verification code” is likely to be encountered by individuals and businesses involved in integrating financial services into applications, particularly those leveraging APIs for payments and data aggregation. Plaid is a technology company that acts as an intermediary, connecting bank accounts to applications and services. A verification code, in this context, is a security measure designed to confirm the legitimacy of a user’s access to their financial information. While the article title itself doesn’t directly align with the provided niche categories (Drones, Flight Technology, Cameras & Imaging, Drone Accessories, Aerial Filmmaking, Tech & Innovation), the underlying concept of verification codes and secure data access is deeply rooted in Tech & Innovation. Specifically, it relates to the technological underpinnings of secure financial transactions and data handling, which are crucial for many innovative applications, including those that might eventually integrate with or be supported by drone technology or aerial services. Therefore, we will explore the concept of Plaid verification codes through the lens of Tech & Innovation, focusing on the security, implementation, and implications of such codes in the digital landscape.

Understanding Plaid and Its Role in Financial Technology

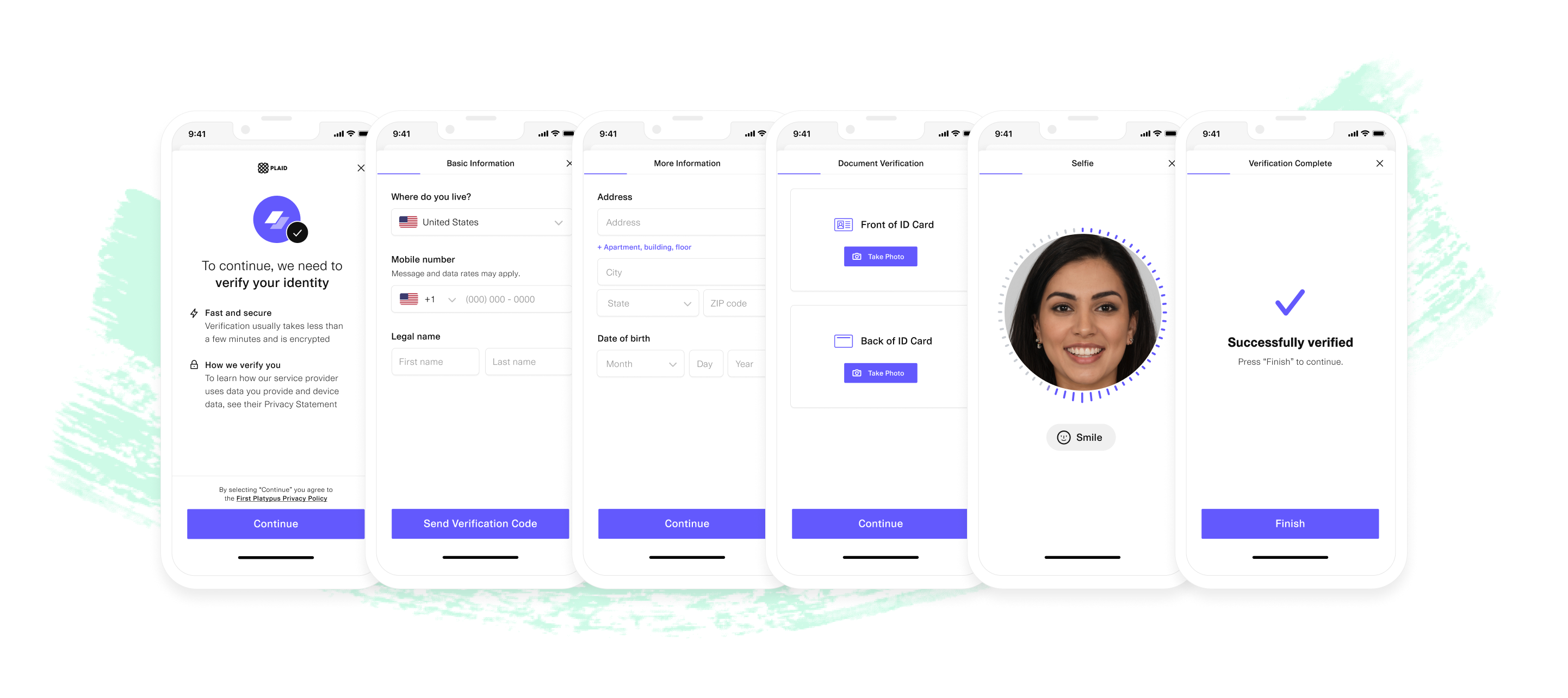

Plaid has emerged as a pivotal player in the fintech ecosystem, enabling a seamless and secure way for developers to connect their applications to users’ bank accounts. The company’s mission is to unlock financial data for everyone, powering the applications that shape modern finance. This includes everything from budgeting apps and personal finance management tools to investment platforms and payment processors. At its core, Plaid provides a secure API (Application Programming Interface) that allows third-party applications to interact with financial institutions. This means users can link their bank accounts to an app without directly sharing their bank login credentials with that app. Plaid handles the complex process of authentication and data retrieval, acting as a trusted intermediary.

The Plaid Link Flow and User Experience

The user experience when linking a bank account through Plaid is designed to be intuitive and secure. This process, often referred to as the “Plaid Link” flow, begins when an application prompts the user to connect their bank account. The user then selects their financial institution from a presented list. Upon selecting their bank, they are presented with an interface that mirrors their bank’s login page. This is a crucial part of the security architecture; the user is actually interacting with their bank’s authentication system, facilitated by Plaid.

The user then enters their online banking username and password. After successful authentication with the bank, the bank’s system sends a token back to Plaid, which then securely shares this token with the application. This token represents a secure, one-time or ongoing authorization to access specific financial data, as agreed upon by the user. The application does not receive the user’s raw login credentials, significantly reducing the risk of credential theft.

The Necessity of Verification Codes within Plaid

Within this sophisticated system, verification codes play a vital role in enhancing security and ensuring that the person initiating the bank account connection is indeed the authorized owner of that account. While the primary authentication happens via the user’s bank login, there are several scenarios where a Plaid verification code might be employed to add an extra layer of assurance. These codes are typically used for:

- Multi-Factor Authentication (MFA) Enhancement: Many financial institutions already employ MFA, which might involve sending a code via SMS to the user’s registered phone number or requiring a code from a hardware token. Plaid’s integration respects and often incorporates these existing MFA protocols. When the user attempts to link their account, and their bank requires an MFA step, Plaid facilitates the delivery and verification of this code.

- Account Ownership Confirmation: In certain edge cases or for specific financial institutions, Plaid might initiate a secondary verification step to definitively confirm account ownership. This could involve a temporary micro-deposit to a linked account, where the user is asked to confirm the amount. Alternatively, it could be a code sent directly through Plaid’s secure channels if the bank’s system allows for this type of integrated verification.

- Fraud Prevention: Verification codes are a standard tool in the fight against fraud. By requiring a code that only the legitimate account holder would possess or be able to receive, Plaid and its partner applications can significantly reduce the risk of unauthorized account linking and subsequent fraudulent activities.

- Session Security: In some instances, a verification code might be used to ensure the security of the current user session or to re-authenticate the user if a certain period of inactivity has passed. This is a common practice in online banking and financial services to protect against session hijacking.

The Technical Implementation and Security Protocols

The implementation of Plaid verification codes is a testament to the layered security strategies employed in modern financial technology. These codes are not arbitrary numbers; they are part of a robust system designed to protect sensitive financial data.

How Verification Codes are Generated and Delivered

When a Plaid verification code is required, its generation and delivery are typically managed in one of a few ways, depending on the specific bank and the integration setup:

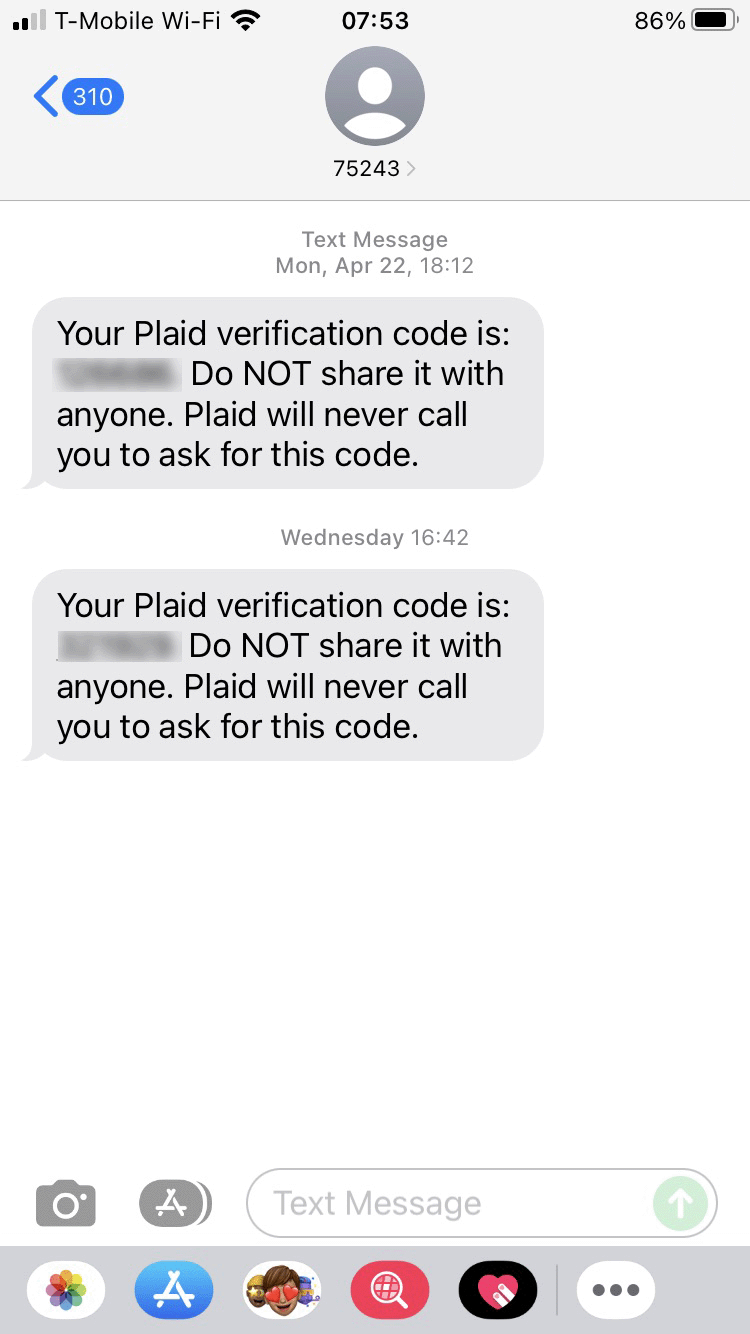

- Bank-Initiated Codes: In the most common scenario, the verification code is generated and sent by the user’s bank. This could be via an SMS message to the phone number linked to the bank account, an email to the registered email address, or through the bank’s dedicated mobile app. Plaid acts as the conduit, prompting the user to enter the code received from their bank within the Plaid Link interface.

- Plaid-Facilitated Codes (Less Common): In some specific integration scenarios, Plaid itself might facilitate the delivery of a verification code. This usually happens when Plaid has a more direct or specialized integration with a particular financial institution. This could involve a push notification to a Plaid-authenticated session or a code sent through a secure message channel that Plaid manages.

- Micro-Deposits: Another method, often used for verification, involves Plaid making two small, temporary deposits into the user’s bank account. The user then checks their bank statement for the exact amounts of these deposits and enters them into the Plaid Link interface. This method directly confirms that the user has access to the bank account and can see its transactions.

Encryption and Secure Data Handling

The entire process, from the initial request to link an account to the eventual exchange of tokens, is underpinned by strong encryption protocols. When a user enters their credentials or a verification code into the Plaid Link interface, this information is transmitted using industry-standard Transport Layer Security (TLS) encryption. This ensures that the data is unreadable to anyone who might intercept it during transit.

Furthermore, Plaid itself does not store users’ bank login credentials. Instead, it stores encrypted tokens. These tokens are specific to the application that initiated the link and grant access only to the permissions that the user has explicitly authorized. If a verification code is involved, it serves as a temporary key or confirmation within this secure exchange, ensuring that only the rightful account holder can complete the linking process. The use of such codes significantly mitigates risks associated with phishing, credential stuffing, and other forms of cyberattacks.

The Importance of User Vigilance

While Plaid employs robust security measures, the ultimate responsibility for safeguarding financial information also lies with the user. It is crucial for users to be aware of how verification codes are used and to remain vigilant against potential scams.

- Never Share Codes Unsolicited: Users should never share verification codes with anyone who contacts them unexpectedly, even if they claim to be from Plaid or their bank. Legitimate institutions will not ask for these codes outside of the secure linking process initiated by the user.

- Verify the Source: Always ensure that the request for a verification code comes from a legitimate Plaid Link interface or a direct communication from your bank. Be wary of suspicious emails, text messages, or phone calls.

- Understand the Context: Understand why you are being asked for a verification code. It should be in direct response to an action you have taken, such as linking an account to a new application.

Use Cases and Implications in Modern Tech Applications

The ability to securely verify and access financial data through Plaid, often involving verification codes, has opened up a vast array of innovative applications that are transforming how we manage our finances and interact with digital services.

Personal Finance and Budgeting Applications

One of the most common use cases is in personal finance and budgeting applications. By securely linking bank accounts, these apps can automatically categorize transactions, track spending, monitor savings goals, and provide users with a comprehensive overview of their financial health. The verification code, in this context, is a critical step that builds trust and ensures the accuracy of the data being fed into these powerful analytical tools. Without such robust verification, the integrity of the financial insights provided would be compromised.

Investment and Trading Platforms

Modern investment platforms, from robo-advisors to cryptocurrency exchanges, often rely on Plaid to facilitate easy and secure funding. Users can link their bank accounts to deposit funds into their investment portfolios. The verification code ensures that the individual initiating the deposit is the legitimate account holder, preventing unauthorized withdrawals or transfers. This seamless integration allows for quicker entry into the market and more dynamic management of investments.

Payment Processing and Fintech Solutions

For businesses and developers building payment solutions, Plaid’s verification capabilities are invaluable. It allows for the secure initiation of one-time or recurring payments, transfers, and direct debits. A verification code might be used to confirm a user’s intent to authorize a payment, adding an extra layer of security and compliance for merchants and service providers. This is particularly important in regulated industries where the integrity of financial transactions is paramount.

Lending and Credit Scoring

In the realm of lending, Plaid enables platforms to securely access a user’s transaction history and account balances for credit assessment and underwriting. This allows for more accurate and potentially faster credit decisions, moving beyond traditional credit scores to offer a more holistic view of a borrower’s financial behavior. Verification codes are instrumental in ensuring that the financial data used for these crucial decisions is accessed with the explicit consent and confirmation of the individual.

The Future of Secure Financial Integrations

The ongoing evolution of Plaid’s technology, including its sophisticated use of verification codes and other security protocols, points towards a future where financial data can be accessed and utilized more broadly and securely. As more innovative applications emerge, particularly those that aim to integrate financial services into diverse platforms, the underlying technologies for secure verification will become even more critical. This includes applications that might leverage drone technology for inventory management, logistics, or even financial transactions in remote locations, where secure and verified access to financial accounts will be indispensable. The focus on robust security, exemplified by the use of verification codes, is not merely a compliance requirement; it is the bedrock upon which the trust and functionality of the entire digital financial ecosystem are built.