The intricate dance of estate planning often involves navigating a landscape far more complex than simply listing possessions. One critical concept that frequently surfaces, yet can be easily misunderstood, is that of a “non-probate asset.” Understanding what constitutes a non-probate asset is paramount for ensuring your estate is distributed according to your wishes, smoothly and efficiently, bypassing the often lengthy and public probate process. This exploration delves into the definition, types, and implications of non-probate assets within the broader context of estate planning, aiming to demystify this crucial element.

Defining the Probate and Non-Probate Divide

At its core, probate is the legal process through which a deceased person’s will is validated and their assets are distributed to beneficiaries. This court-supervised procedure involves identifying and appraising the deceased’s assets, paying off debts and taxes, and then distributing the remaining property as directed by the will or, in the absence of a will, by state law.

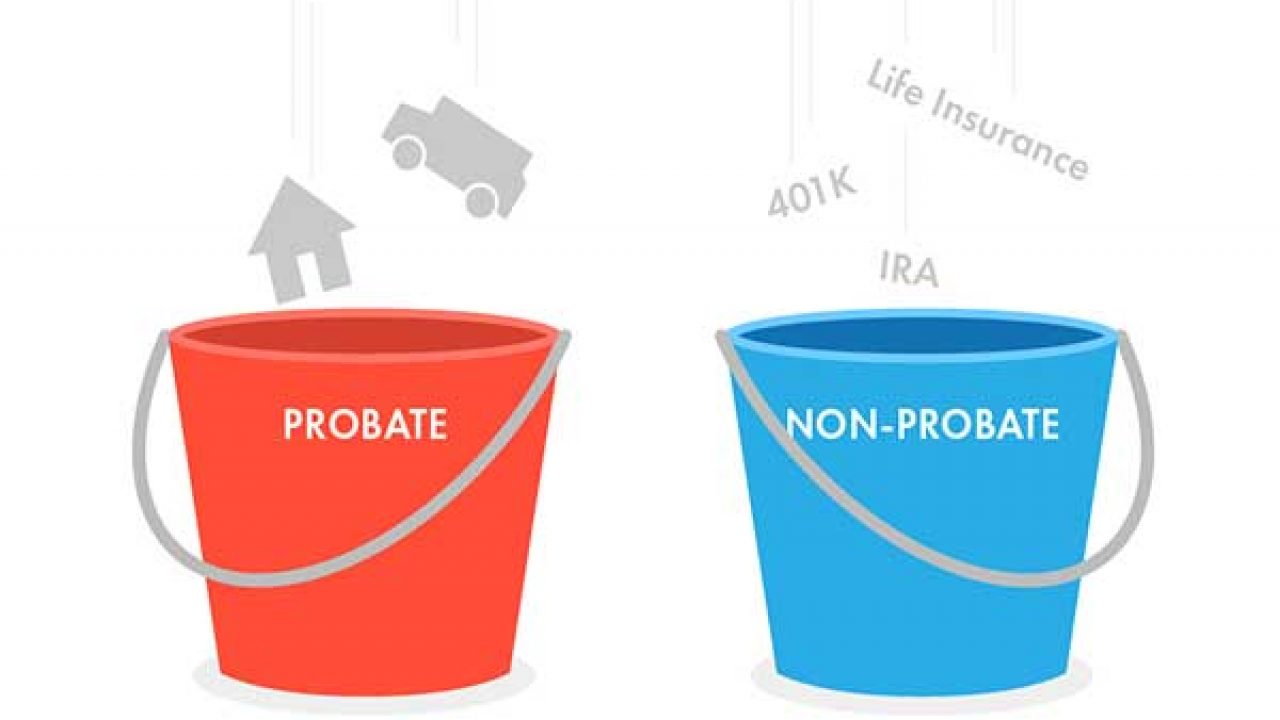

However, not all assets owned by an individual at the time of their death are subject to this probate process. Assets that bypass probate are known as non-probate assets. These assets pass directly to a designated beneficiary or joint owner outside of the will and the court’s jurisdiction. This distinction is fundamental because it dictates how and to whom these assets will ultimately transfer.

The primary characteristic that defines a non-probate asset is the existence of a beneficiary designation or a form of co-ownership that automatically transfers ownership upon death. This pre-determined transfer mechanism is designed to expedite the distribution of these assets, shielding them from the potentially cumbersome and time-consuming probate court proceedings.

Conversely, probate assets are those that do not have a beneficiary designation or joint ownership with survivorship rights. These assets are solely owned by the deceased and will therefore need to go through the probate process to be legally transferred to heirs or beneficiaries as outlined in the will or by intestacy laws. Examples of typical probate assets include:

- Solely owned bank accounts

- Solely owned real estate

- Stocks, bonds, and other investments held in your name alone

- Personal property (vehicles, jewelry, art) not held in joint ownership or with beneficiary designations.

The decision to structure asset ownership in a way that creates non-probate assets is a strategic choice within estate planning, often aimed at simplifying the inheritance process for loved ones.

Key Types of Non-Probate Assets

The realm of non-probate assets is diverse, encompassing various financial instruments and property titling arrangements. Recognizing these categories is the first step towards effectively planning their disposition.

Life Insurance Policies

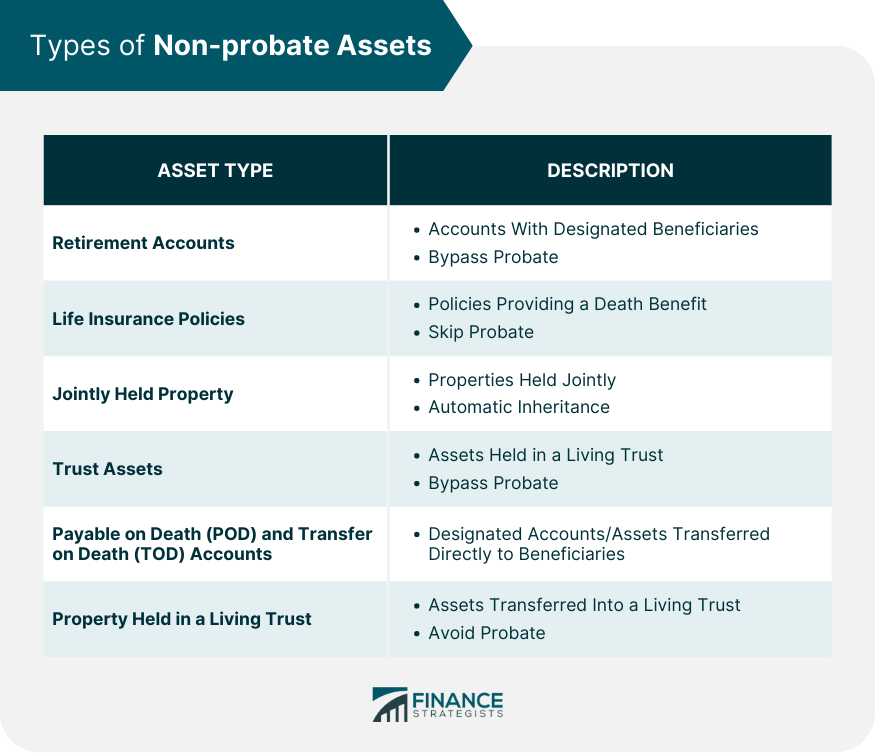

Life insurance policies are a classic example of a non-probate asset. Upon the death of the insured, the death benefit is paid directly to the named beneficiary(ies) specified in the policy. This payout typically occurs relatively quickly and is not subject to the probate process, making it a valuable tool for providing immediate financial support to beneficiaries. It’s crucial to periodically review and update beneficiary designations on life insurance policies to ensure they align with current wishes and circumstances.

Retirement Accounts

Retirement accounts, such as 401(k)s, 403(b)s, IRAs (Traditional and Roth), and pensions, are almost universally designed as non-probate assets. These accounts have specific beneficiary designations that are established when the account is opened or updated over time. Upon the account holder’s death, the remaining balance is transferred directly to the designated beneficiary(ies). This direct transfer allows for the continuation of tax-deferred growth for some account types and provides a straightforward inheritance mechanism. As with life insurance, maintaining accurate beneficiary information is vital.

Payable-on-Death (POD) and Transfer-on-Death (TOD) Designations

Many financial institutions offer the ability to designate beneficiaries for bank accounts and investment accounts through POD and TOD designations, respectively.

Payable-on-Death (POD) Accounts

When you open a bank account (checking, savings, or money market), you can often designate a POD beneficiary. This means that upon your death, the funds in that account will automatically transfer to the named POD beneficiary without going through probate. The account holder retains full control of the funds during their lifetime, and the POD designation only becomes active upon their death.

Transfer-on-Death (TOD) Accounts

Similarly, TOD designations can be attached to brokerage accounts, stocks, bonds, and mutual funds. This allows these securities to pass directly to the named TOD beneficiary upon your passing, bypassing the probate court. This is a highly effective way to ensure that your investment portfolio is transferred efficiently to your chosen heirs.

Jointly Owned Property with Right of Survivorship

Certain forms of joint ownership of property ensure that the deceased owner’s share automatically passes to the surviving joint owner(s). The most common form is joint tenancy with right of survivorship (JTWROS).

Joint Tenancy with Right of Survivorship (JTWROS)

When property, such as real estate or a bank account, is held in JTWROS, each owner has an undivided interest in the entire property. Upon the death of one joint tenant, their ownership interest automatically passes to the surviving joint tenant(s), regardless of what a will might state. This is a powerful estate planning tool for married couples or others who wish for their property to pass automatically to the surviving co-owner.

However, it’s important to distinguish JTWROS from tenancy in common, where each owner holds a distinct share and their share would pass according to their will or intestacy laws upon their death, thus becoming a probate asset.

Trusts

Assets properly transferred into a living trust during the grantor’s lifetime are also considered non-probate assets. A living trust is a legal entity created to hold assets. The grantor typically acts as the trustee during their lifetime, managing the assets. Upon the grantor’s death, a successor trustee takes over and distributes the trust assets to the named beneficiaries according to the trust’s terms, without the need for probate. This is a highly effective method for avoiding probate and maintaining privacy.

The Advantages of Non-Probate Assets in Estate Planning

The strategic use of non-probate assets offers several compelling advantages for individuals planning their estates and for their intended beneficiaries.

Avoiding the Probate Process

The most significant advantage is the avoidance of probate. Probate can be a lengthy, costly, and public process. Court dockets can be crowded, leading to significant delays in asset distribution. Legal fees, court costs, and executor fees can erode the value of the estate. Furthermore, probate records are typically public, meaning that details about your assets, debts, and beneficiaries can become accessible to anyone. Non-probate assets bypass this entirely, offering a more efficient and private transfer of wealth.

Speed of Distribution

Because non-probate assets pass directly to beneficiaries outside of the court system, their distribution is generally much faster than that of probate assets. This can be crucial for beneficiaries who rely on these assets for immediate financial needs, such as covering living expenses or funeral costs.

Reduced Estate Administration Costs

By reducing the size of the probate estate, the associated costs of administration, such as legal fees and court filing fees, can be significantly lowered. While there may be costs associated with setting up certain non-probate structures (like trusts), these are often a one-time expense that can lead to substantial savings in the long run.

Flexibility and Control

Non-probate mechanisms, such as beneficiary designations and living trusts, offer a degree of flexibility and control. You can update beneficiary designations as your life circumstances change, ensuring your estate plan remains relevant. Trusts also provide a high level of customization, allowing you to set specific conditions or timelines for distributions to beneficiaries, offering protection and guidance.

Considerations and Potential Pitfalls

While non-probate assets offer numerous benefits, it’s crucial to be aware of potential considerations and pitfalls to ensure your estate plan functions as intended.

Inaccurate or Outdated Beneficiary Designations

One of the most common errors leading to unintended consequences is having outdated or inaccurate beneficiary designations. Life events such as marriage, divorce, the birth of children, or the death of a beneficiary can render your existing designations obsolete. If a beneficiary has predeceased you and you haven’t updated the designation, the asset might fall into your probate estate or pass to contingent beneficiaries who may not be your current preference.

Lack of Coordinated Estate Planning

While non-probate assets pass automatically, they are still part of your overall estate for tax and planning purposes. It’s essential to integrate your non-probate assets into your comprehensive estate plan. For instance, relying solely on non-probate assets without a will to cover specific bequests or to manage any remaining probate assets can leave gaps in your distribution plan.

Impact on Estate Taxes

While non-probate assets bypass probate, they are generally still included in the taxable estate for federal and state estate tax purposes. If your estate is large enough to be subject to estate taxes, having a significant portion of your assets in non-probate form will not shield them from this liability. Careful planning is needed to manage potential estate tax obligations, regardless of whether assets are probate or non-probate.

Creditor Claims

While probate assets are typically the primary target for creditors, in some jurisdictions and under certain circumstances, creditors may still be able to make claims against non-probate assets, particularly if the estate is insolvent. This is a complex area of law that can vary by state, and consulting with an estate planning attorney is advisable.

Understanding Joint Ownership Nuances

The specific type of joint ownership is critical. As mentioned, joint tenancy with right of survivorship (JTWROS) ensures automatic transfer. However, if property is held as “tenants in common” or as “community property without right of survivorship,” the deceased’s share will likely go through probate. Similarly, simply adding a person’s name to a deed without specifying survivorship rights can create unintended legal consequences.

Conclusion: Integrating Non-Probate Assets into Your Estate Plan

Non-probate assets play a vital role in modern estate planning, offering a streamlined and efficient pathway for wealth transfer, thereby bypassing the complexities and delays of the probate process. Understanding the various forms these assets can take—from life insurance and retirement accounts to POD/TOD designations and jointly owned property—is the foundational step in leveraging their benefits.

However, the effective utilization of non-probate assets is not a standalone strategy. It requires careful integration into a comprehensive estate plan. Regularly reviewing and updating beneficiary designations, understanding the implications of different ownership structures, and coordinating these assets with any wills or trusts are crucial to ensuring your wishes are honored. By proactively addressing these elements with the guidance of experienced legal counsel, individuals can create an estate plan that is not only efficient and cost-effective but also provides peace of mind, knowing their legacy will be passed on as intended to their loved ones. The strategic management of non-probate assets is a cornerstone of a well-crafted estate plan, empowering individuals to dictate the future of their assets with clarity and precision.