In the dynamic realm of “Tech & Innovation,” particularly as it pertains to AI, autonomous flight, mapping, and remote sensing, understanding fundamental economic principles can illuminate the broader landscape in which these transformative technologies operate. Among these principles, the concept of a lump sum tax stands as a theoretical cornerstone, offering insights into efficiency, equity, and the potential impact of fiscal policy on innovation. While rarely implemented in its purest form in modern economies, examining “what is a lump sum tax” provides a critical lens through which to consider the ideal and practical challenges of taxing a rapidly evolving sector.

Unpacking the Fundamentals of a Lump Sum Tax in an Innovative Economy

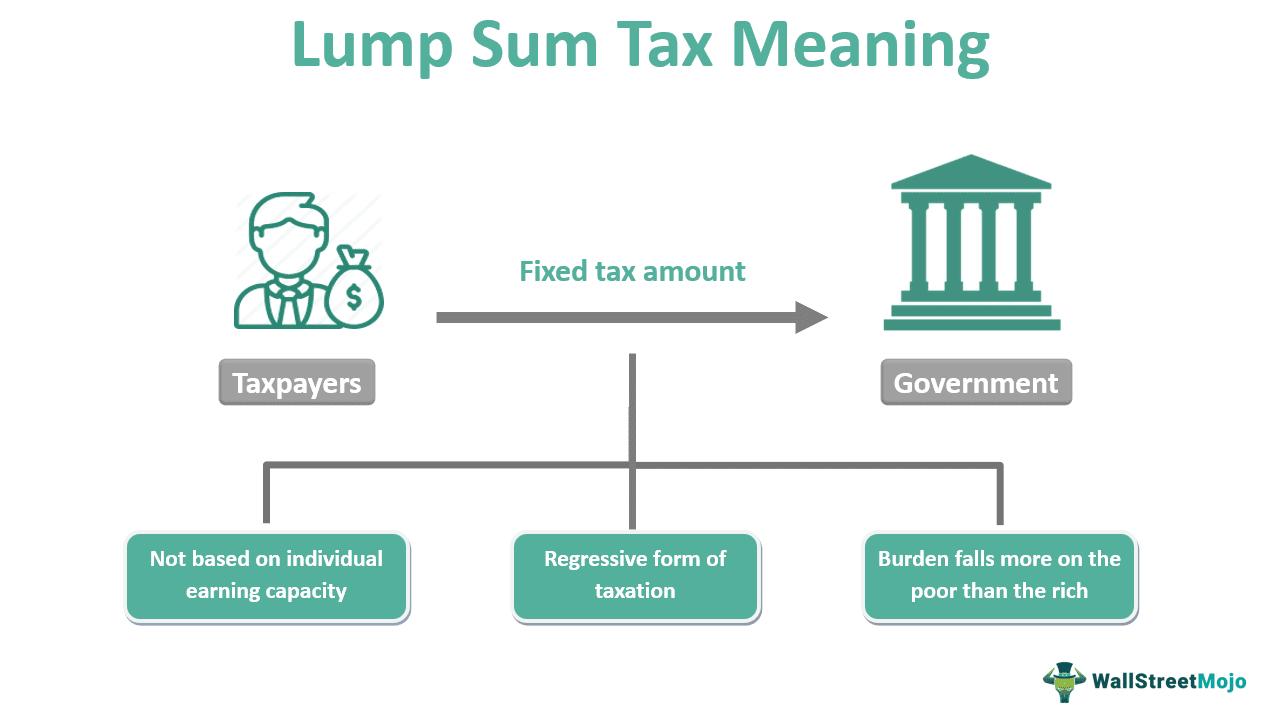

A lump sum tax is, at its core, a fixed monetary amount levied equally on all individuals or entities within a specified jurisdiction or category, irrespective of their income, consumption, wealth, or economic activities. Unlike proportional or progressive taxes, which scale with economic variables, a lump sum tax demands the same payment from everyone subject to it. This seemingly simple construct carries profound implications, particularly when viewed through the prism of fostering or funding technology and innovation.

A Core Definition and Its Economic Distinctiveness

To elaborate, imagine a scenario where every registered drone company, regardless of its revenue, profit, or the number of drones sold, had to pay a flat, unchanging annual fee of, say, $10,000. This fixed payment, detached from the firm’s economic performance, is the essence of a lump sum tax. Its most distinctive feature is its “non-distortionary” nature. Economists prize this characteristic because, theoretically, a lump sum tax does not alter economic decisions. For instance, a progressive income tax might disincentivize additional work or investment because a higher marginal tax rate reduces the reward for increased effort. A lump sum tax, however, is a sunk cost; once paid, it does not influence choices about how much to work, invest in R&D, or innovate, as it won’t change based on those activities. This theoretical neutrality makes it an attractive concept for economists seeking optimal efficiency in resource allocation.

Theoretical Efficiency and Equity Debates

The theoretical advantages of a lump sum tax lie primarily in its efficiency. Because it doesn’t distort economic behavior, it allows markets to allocate resources most efficiently. Companies would invest in AI development or autonomous flight systems based purely on their potential returns, not on how those returns might be diminished by escalating tax brackets. This could, in theory, accelerate innovation by removing tax-induced inefficiencies.

However, the significant drawback, and the reason it is seldom fully implemented, is its profound inequity. A fixed tax amount, paid equally by all, is inherently regressive. For a tech giant like a major drone manufacturer, a $10,000 lump sum tax is negligible. For a small startup developing a niche FPV system or a micro-drone racing team just breaking even, that same $10,000 could be an insurmountable barrier. It disproportionately affects those with lower incomes or less capacity to pay, exacerbating economic disparities. In an innovative economy characterized by diverse players ranging from garage inventors to multinational corporations, the equity implications of a pure lump sum tax become a critical point of contention, often outweighing its theoretical efficiency benefits.

The Hypothetical Role of Lump Sum Taxation in Fostering or Hindering Tech & Innovation

While a pure lump sum tax might be an academic ideal, its theoretical underpinnings inform discussions around tax policies designed to interact with the tech sector. Understanding its impact on stimulating investment, fostering entrepreneurship, and addressing resource allocation challenges is crucial.

Stimulating Investment and Entrepreneurship

Consider the potential for a truly non-distortionary tax system to stimulate investment and entrepreneurship. If innovators, from AI engineers to drone mapping specialists, knew that their success would not lead to higher marginal tax rates on their profits or personal income, the incentive to invest heavily in R&D, launch new ventures, and pursue groundbreaking ideas could be immense. The removal of complex tax compliance, often a burden for lean startups, could also free up valuable resources – both capital and human – to be redirected towards core innovation activities. A predictable, fixed cost, rather than a variable one tied to success, might reduce financial uncertainty, encouraging more risk-taking in areas like autonomous flight development or advanced sensor integration, which often require significant upfront capital and long gestation periods.

Potential Disincentives and Resource Allocation Challenges

Conversely, the implementation of a lump sum tax could present significant hurdles. For nascent businesses in the tech sector, especially those in the early, often unprofitable, stages of development (e.g., a startup perfecting AI follow mode algorithms or a company pioneering new remote sensing techniques), a substantial lump sum tax could be a death knell. Such a fixed cost, payable regardless of revenue generation, could drain vital seed capital, discouraging entrepreneurs from even entering the market. This creates a challenging paradox: while aiming for efficiency, it could stifle the very innovation it seeks to nurture by failing to account for the asymmetric financial capabilities within the diverse tech ecosystem. Furthermore, it raises questions about how such a tax would be structured to avoid deterring small-scale innovators while still generating meaningful revenue from established industry players.

Funding Public Goods for the Tech Ecosystem

An interesting application of the lump sum principle, even if not a direct tax, could be in funding public goods essential for the tech ecosystem. If a revenue stream from a modified lump sum levy were dedicated, for example, to establishing and maintaining national drone test ranges for autonomous flight, developing open-source AI frameworks, or curating vast repositories of mapping and remote sensing data, it could represent an innovative funding mechanism. Such public goods are critical for lowering the barrier to entry for smaller firms and accelerating collective progress in tech. The challenge, however, would be to design a system that captures contributions from the industry without crippling its growth, potentially through tiered or capped “lump sum” contributions tailored to different scales of operation.

Strategic Implications for Drone Technology and Autonomous Systems

The unique characteristics of the drone industry and autonomous systems make them a compelling case study for exploring the theoretical relevance of lump sum principles, even if they manifest as fees or levies rather than pure taxes.

Licensing and Regulatory Fees for Drone Operations

While not strictly a governmental tax, many current regulatory frameworks for drone operations, autonomous vehicles, and specific technological certifications embody aspects of a lump sum payment. For instance, a fixed annual fee for an operational license for commercial drone pilots or for companies operating autonomous delivery fleets represents a lump sum cost. These fees are typically designed to cover the administrative costs of regulatory oversight, ensure safety standards, manage airspace, or maintain digital infrastructure for navigation (like GPS accuracy monitoring). They are generally independent of the number of hours flown or the specific profit generated from each operation, embodying the “fixed amount regardless of activity” principle. Such fees are intended to ensure a baseline level of compliance and contribution towards the shared infrastructure that enables these innovative technologies to function safely and effectively.

Addressing Externalities and Societal Impact

The rise of AI, autonomous flight, and pervasive mapping and remote sensing capabilities also brings potential societal externalities—issues like privacy concerns from widespread data collection, ethical dilemmas in AI decision-making, or increased airspace congestion. One could hypothetically envision “lump sum” levies on companies that develop technologies with significant potential externalities. This isn’t necessarily a punitive tax but rather a fixed contribution earmarked for mitigating these negative impacts or investing in research for ethical AI and privacy-enhancing technologies. Such a mechanism could be seen as an innovative approach to ensure that the creators of disruptive technologies contribute tangibly to managing their broader societal footprint, akin to a “social dividend” for technological advancement.

Innovation Funding through Novel Mechanisms

Beyond traditional taxation, the concept of a lump sum can inspire novel funding mechanisms for cutting-edge innovation. Imagine a collective “Innovation Acceleration Fund” for the drone industry, where every major player (e.g., manufacturers, software developers for autonomous systems, large service providers) contributes a fixed, predetermined annual amount. This pooled capital could then be directed towards high-risk, pre-competitive research in areas like next-generation battery technology, robust urban air mobility infrastructure, or universally compatible AI communication protocols. Such a lump sum contribution model, distinct from a government tax, could foster collaborative innovation by spreading risk and ensuring sustained investment in foundational research that benefits the entire sector.

Reimagining Taxation for Future Tech Landscapes

The conceptual exploration of a lump sum tax, despite its practical limitations, offers valuable insights for designing fiscal and regulatory frameworks that can keep pace with the unparalleled speed of “Tech & Innovation.”

Adaptive Tax Models for Dynamic Sectors

The rapid evolution of technologies like AI, autonomous flight, and sophisticated mapping requires tax systems that are flexible and adaptive, rather than rigid and outdated. While a pure lump sum tax is likely too blunt an instrument, its theoretical appeal—its non-distortionary nature—highlights the desirability of tax models that minimize interference with innovative impulses. Future tax policies for the tech sector may incorporate hybrid models, perhaps combining elements of lump sum contributions (for regulatory compliance or public good funding) with more traditional, progressive taxation on profits, ensuring both efficiency and equity. The goal should be to create a stable, predictable, and supportive financial environment that encourages, rather than constrains, technological breakthroughs.

The Pursuit of Economic Neutrality in Tech Policy

A central takeaway from examining the lump sum tax is the importance of economic neutrality. Ideal tech policy should aim to create a level playing field where no specific technology (e.g., FPV vs. autonomous drones, thermal vs. optical imaging) or business model is artificially advantaged or disadvantaged by the tax code. By striving for neutrality, governments can ensure that innovation flourishes based on its inherent merit and market demand, rather than being skewed by tax incentives or disincentives. The lump sum tax, in its theoretical purity, represents the ultimate form of neutrality, serving as a benchmark against which all other, more complex, tax policies can be measured for their efficiency and impact on innovation.

Global Perspectives on Tech Taxation

The discussions around “what is a lump sum tax” also resonate within the ongoing global debate about taxing multinational tech giants. As countries grapple with how to fairly tax digital services and large technology corporations that often operate across borders with complex profit allocation strategies, proposals sometimes emerge that incorporate “lump sum”-like elements. These might include fixed minimum tax contributions or simplified tax regimes aimed at ensuring a baseline contribution from highly profitable tech entities, irrespective of intricate accounting maneuvers. This global dialogue underscores the continuous quest for tax systems that are transparent, efficient, and equitable, capable of supporting a globalized and innovation-driven economy.