In the complex world of insurance, understanding the terminology and documentation is paramount. Among the many terms that can arise during policy discussions, renewals, or claims, “loss run” stands out as a crucial piece of information for businesses and individuals seeking accurate and competitive insurance coverage. While seemingly straightforward, a loss run represents a comprehensive historical record that profoundly influences underwriting decisions and premium calculations. This article delves into the multifaceted nature of a loss run, exploring its definition, components, significance, and how it is utilized within the insurance industry.

Understanding the Core Components of a Loss Run

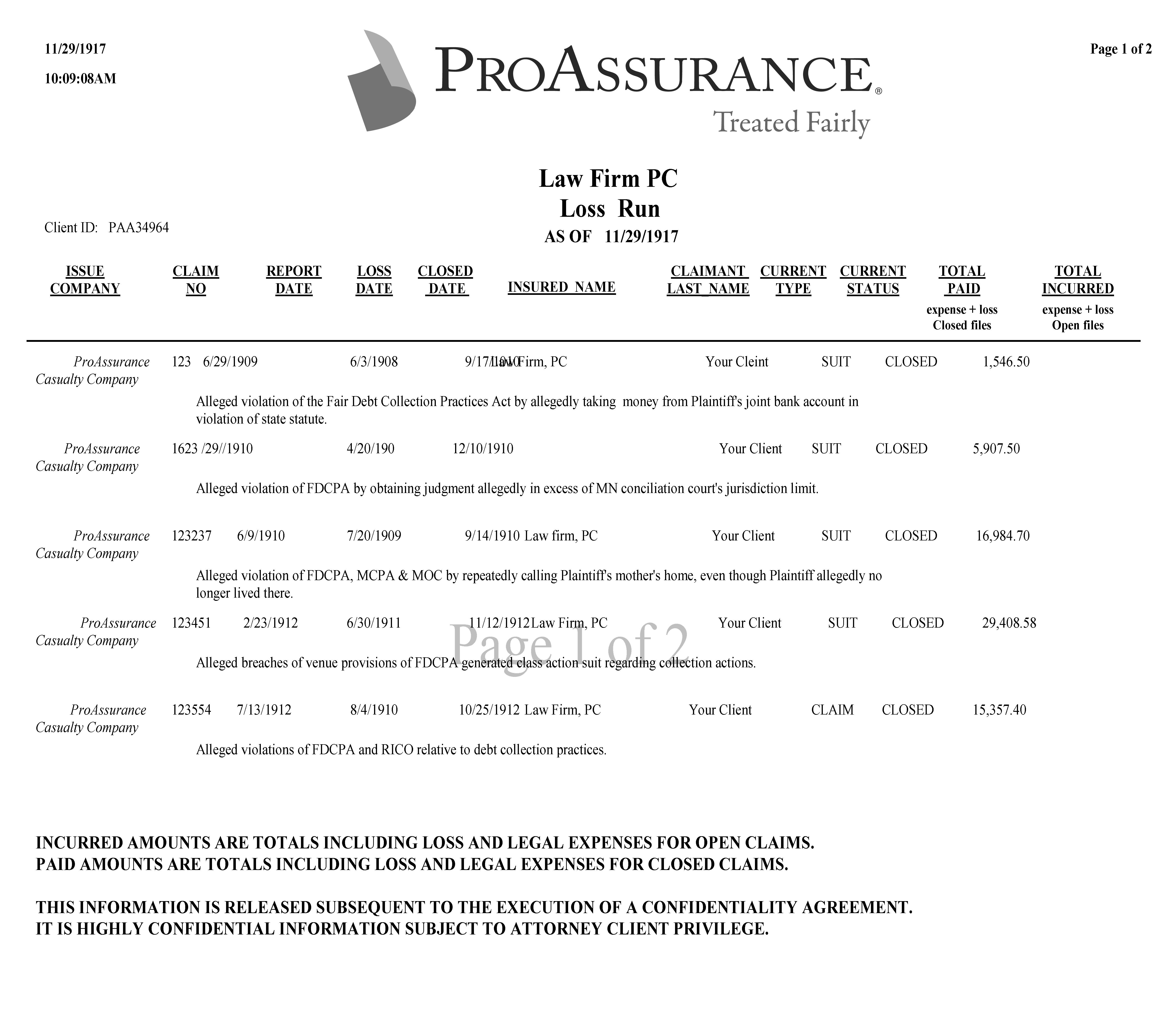

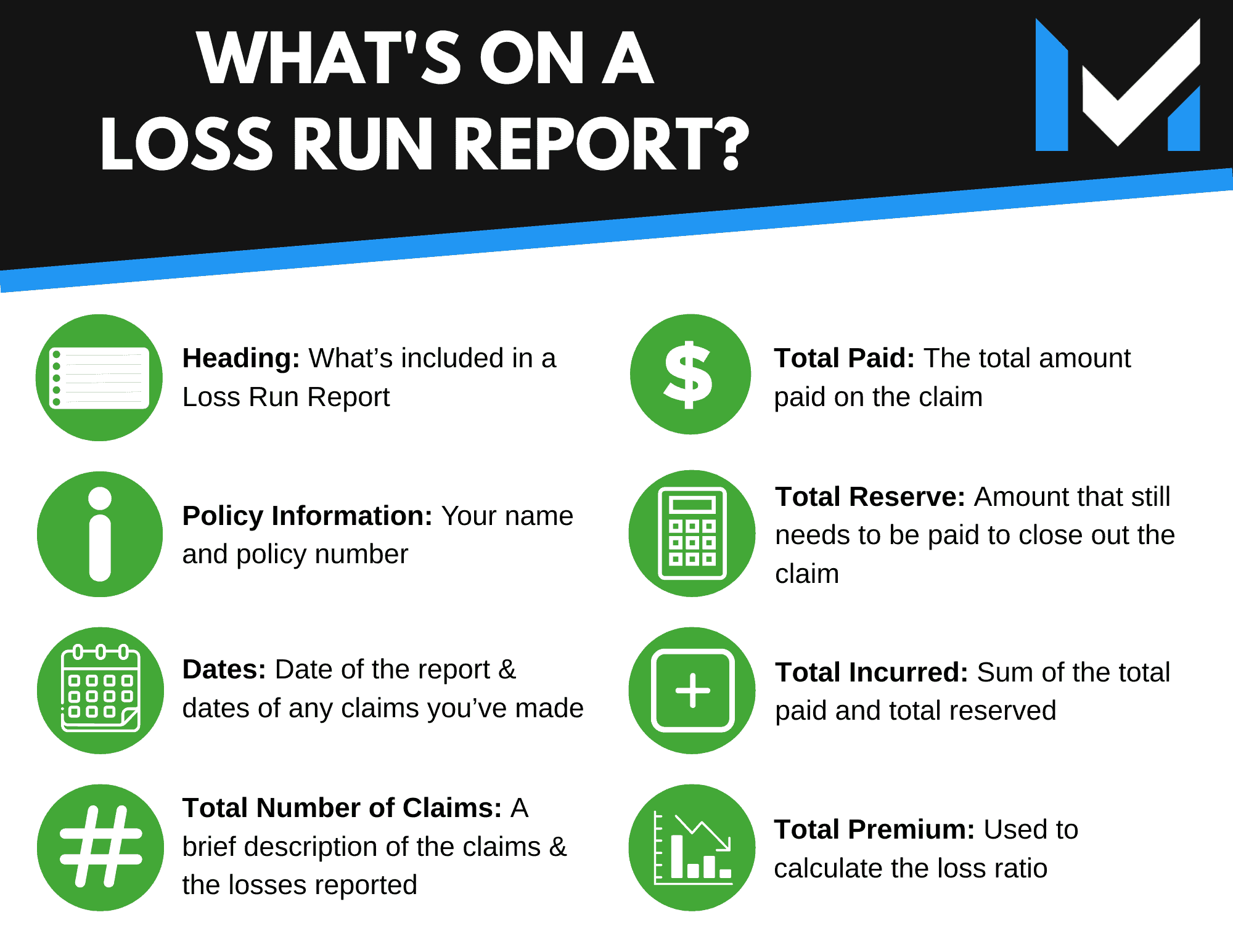

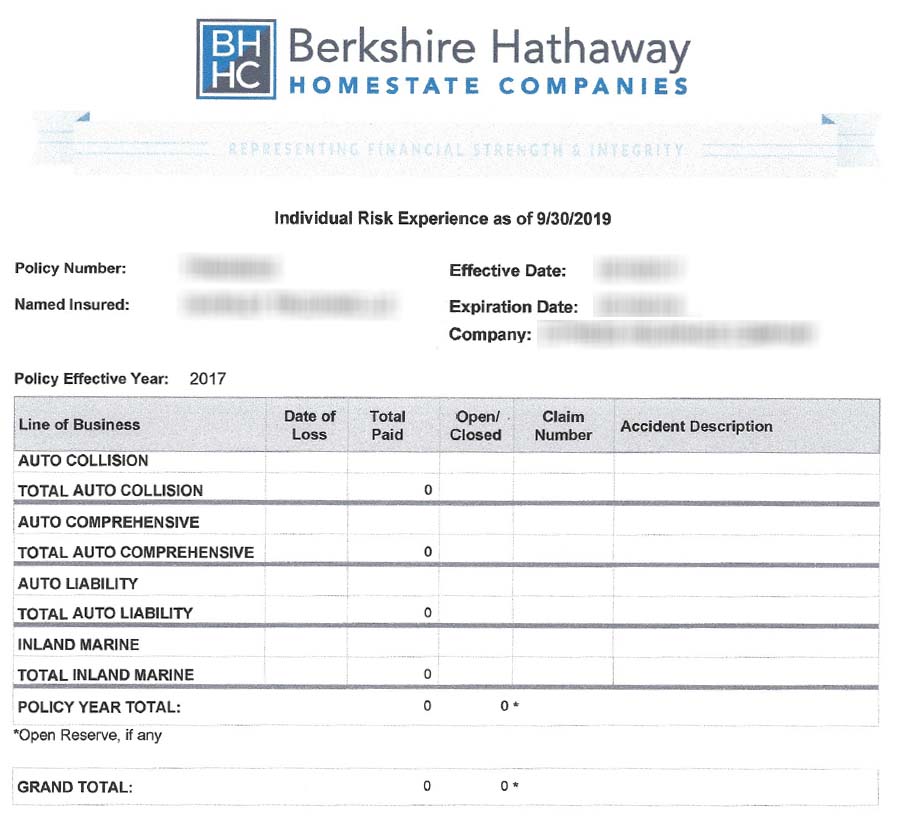

At its heart, a loss run is a standardized report detailing an insurance policyholder’s claims history over a specified period. It acts as a transparent window into past losses, providing insurers with the essential data needed to assess risk and price future policies appropriately. While the exact format and specific details can vary slightly between insurance carriers, several core components are consistently found within a loss run.

Policy Information

The foundational element of any loss run is clear identification of the insured entity and the policies in question. This section typically includes:

- Policyholder Name and Address: This unequivocally identifies the insured party.

- Policy Number(s): Each policy associated with the loss history will be listed with its unique identifier.

- Policy Period(s): The specific dates during which the policies were in effect are crucial for determining the timeframe of the claims data. This allows insurers to understand the historical context of the losses.

- Type of Coverage: The loss run will specify the lines of insurance covered by the policies (e.g., General Liability, Workers’ Compensation, Commercial Auto, Property). This is vital because different coverage types have different risk profiles and claims patterns.

Claims Details

The most significant portion of a loss run comprises the detailed information about each claim filed under the specified policies. This section provides the granular data that insurers analyze to understand the frequency, severity, and nature of past incidents. Key claims details include:

- Claim Number: A unique identifier for each individual claim.

- Date of Loss: The date on which the incident giving rise to the claim occurred. This helps establish the timeline and potential contributing factors.

- Date Claim Reported: The date the claim was officially filed with the insurance company. This can indicate the timeliness of reporting and the potential for mitigation efforts.

- Type of Loss/Claim: A description of the incident that led to the claim. This could range from a slip-and-fall incident for General Liability to a vehicle collision for Commercial Auto.

- Status of Claim: This indicates whether the claim is still open, closed, denied, or pending. Open claims can represent future financial exposure for the insurer.

- Amount Paid: The total amount of money the insurance company has disbursed to settle the claim. This includes payments made to the claimant, legal fees, investigation costs, and any other related expenses.

- Amount Reserved: For open claims, this represents the insurer’s estimate of the future costs associated with settling the claim. This is a critical indicator of potential future financial exposure.

- Amount Paid to Date: The total amount paid out on a claim from its inception until the current date.

- Salvage/Subrogation: Information about any amounts recovered by the insurer through salvage (selling damaged property) or subrogation (recovering funds from a third party responsible for the loss). These can offset the total cost of a claim.

Summary Statistics

Beyond individual claim details, many loss runs also provide aggregated summary statistics to offer a quick overview of the policyholder’s loss experience. These can include:

- Total Number of Claims: The total count of claims filed within the reporting period.

- Total Amount Paid: The sum of all amounts paid out on all claims.

- Total Amount Reserved: The aggregate of all reserves for open claims.

- Loss Ratio: This is a critical metric calculated as (Total Amount Paid + Total Amount Reserved) / Total Premiums Earned. A higher loss ratio generally indicates a riskier policyholder.

- Average Cost Per Claim: Calculated by dividing the total amount paid by the number of closed claims.

The Profound Significance of Loss Runs in the Insurance Ecosystem

A loss run is far more than a mere historical document; it is a cornerstone of the insurance underwriting process and a vital tool for risk management. Its significance permeates various aspects of the insurance relationship, impacting both the insurer’s assessment and the policyholder’s ability to secure coverage.

Underwriting and Risk Assessment

For insurance carriers, the loss run is the primary source of information for evaluating the risk associated with insuring a particular entity. Underwriters meticulously analyze the claims history to:

- Predict Future Losses: By examining past trends, insurers can develop a more informed projection of potential future losses. A history of frequent or severe claims suggests a higher likelihood of similar incidents occurring in the future.

- Identify Risk Factors: The loss run can highlight specific areas where a business or individual may have a higher propensity for claims. For example, a recurring pattern of vehicle accidents for a trucking company might indicate issues with driver training, maintenance, or routing.

- Determine Insurability: In some cases, the loss history might be so concerning that an insurer deems the risk uninsurable through standard markets. This could lead to the policyholder needing to seek coverage from surplus lines carriers or even a residual market mechanism.

- Set Premiums: The data within the loss run directly influences the premium charged for a new policy. A favorable loss history with few or low-cost claims typically results in lower premiums, while a history of significant losses will almost invariably lead to higher premiums.

Pricing and Coverage Adjustments

The insights gleaned from a loss run allow insurers to tailor their pricing and coverage strategies to the specific risk profile of the applicant.

- Premium Adjustments: As mentioned, premiums are directly affected. Insurers may also apply specific surcharges or discounts based on the loss history.

- Deductible Negotiations: A history of frequent, smaller claims might lead an insurer to suggest a higher deductible on future policies. This shifts some of the financial burden for minor incidents to the policyholder, incentivizing risk mitigation. Conversely, a clean loss history might allow for lower deductibles.

- Coverage Limitations or Exclusions: In instances of specific, recurring types of losses, an insurer might impose limitations or even exclusions on certain coverages within the new policy. For instance, if a business has a history of product liability claims related to a specific product line, that line might be excluded from coverage.

- Risk Management Recommendations: A proactive insurer might use the loss run data to identify areas where the policyholder can improve their risk management practices. This collaborative approach can benefit both parties by reducing future losses.

The Policyholder’s Perspective

For the policyholder, obtaining and understanding their loss run is equally important. It empowers them to:

- Shop for Competitive Quotes: By providing accurate loss runs to multiple insurance brokers or carriers, businesses can ensure they are receiving comparable quotes based on their actual risk profile. Inaccurate or incomplete loss runs can lead to inaccurate quotes.

- Negotiate Terms and Premiums: Armed with their loss history, policyholders can engage in more informed discussions with their insurers regarding premiums, deductibles, and coverage terms.

- Identify Areas for Improvement: Reviewing their own loss run can highlight patterns and trends that the policyholder may not have been aware of, prompting them to implement risk mitigation strategies. This proactive approach can lead to a safer workplace and fewer insurance claims.

- Prepare for Policy Renewals: Understanding past claims can help businesses anticipate potential changes in their renewal premiums and coverage options.

Obtaining and Utilizing Your Loss Run Effectively

The process of obtaining and then effectively utilizing a loss run is crucial for any business or individual involved with insurance. It requires diligence, accuracy, and a strategic approach.

The Process of Requesting a Loss Run

Requesting a loss run is a standard procedure, but it’s essential to follow the correct channels and provide the necessary information.

- Contact Your Current Insurer: The most direct way to obtain your loss run is to contact your current insurance carrier. They are obligated to provide it upon request.

- Contact Your Insurance Broker/Agent: If you work with an insurance broker or agent, they can facilitate the request on your behalf. In fact, many brokers proactively obtain loss runs for their clients in anticipation of renewal periods.

- Specify the Time Period: When requesting a loss run, clearly state the desired time period. Typically, insurers will provide a three-year or five-year history, but longer periods may be available upon request. The most common request is for the past five years.

- Provide Necessary Identification: Be prepared to provide your policy number, business name, and other identifying information to ensure the correct loss run is generated.

- Allow Sufficient Time: The generation of a loss run can take some time, especially if there are many open claims or a complex claims history. It’s advisable to request it well in advance of your policy renewal date.

Best Practices for Reviewing and Using Your Loss Run

Once you have your loss run in hand, a thorough review and strategic utilization are key.

- Verify Accuracy: The first and most critical step is to meticulously review the loss run for any inaccuracies. Check policy numbers, dates of loss, claim status, and amounts paid. Discrepancies can significantly impact future quotes. If you find errors, immediately contact your insurer or broker to have them corrected.

- Understand Each Claim: Don’t just look at the numbers; try to understand the circumstances surrounding each claim. What happened? Were there contributing factors? What measures were taken to prevent recurrence?

- Analyze Trends: Look for patterns in the claims data. Are there specific types of losses occurring repeatedly? Are claims concentrated in a particular department or location? This analysis is crucial for identifying areas where risk management can be improved.

- Benchmark Against Industry Averages: If possible, try to benchmark your loss experience against industry averages for similar businesses. This can provide valuable context for your loss ratio and overall risk profile.

- Share with Your Broker/Agent: Provide your loss run to your insurance broker or agent and discuss its implications. They can help you interpret the data, advise on risk mitigation strategies, and use it to secure the best possible coverage terms.

- Use for Risk Management: The loss run is a powerful tool for identifying areas where your business operations may be exposing you to unnecessary risk. Use this information to implement targeted safety programs, training, or operational changes.

The Evolving Landscape of Loss Runs and Claims Data

The way loss runs are generated and utilized is continuously evolving, driven by advancements in technology and a growing emphasis on data analytics within the insurance industry.

Technology’s Impact on Loss Run Generation

Modern insurance carriers are leveraging technology to streamline the process of generating and disseminating loss runs.

- Digital Platforms and Portals: Many insurers now offer online portals where policyholders and their brokers can access and download loss runs directly. This provides faster and more convenient access to this critical information.

- Data Standardization and Analytics: Advancements in data management allow for more standardized loss run formats across different carriers, making it easier for brokers and analytics firms to aggregate and analyze data from multiple sources. Sophisticated analytics are used to identify subtle trends and predict future loss probabilities with greater accuracy.

- Integration with Risk Management Software: Increasingly, loss run data is being integrated with broader risk management software solutions, allowing businesses to gain a more holistic view of their risk exposures and claims history alongside other operational data.

The Future of Claims Data Utilization

The role of claims data, as represented by loss runs, is expanding beyond traditional underwriting.

- Predictive Analytics and AI: Artificial intelligence and machine learning are being used to analyze vast datasets, including loss runs, to develop more sophisticated predictive models. These models can forecast claim frequency and severity with greater precision, enabling insurers to make more informed pricing decisions and proactively identify high-risk policyholders.

- Telematics and IoT Data: In areas like commercial auto and workers’ compensation, the integration of telematics (e.g., GPS, driver behavior monitoring) and Internet of Things (IoT) devices provides real-time data that complements historical loss run information. This offers a more dynamic and granular understanding of risk.

- Focus on Proactive Risk Mitigation: As the industry shifts towards a more proactive approach, loss run data will become an even more critical tool for guiding risk mitigation efforts. Insurers and policyholders will collaborate more closely to address the root causes of claims, rather than simply reacting to them.

- Data-Driven Insurance Products: The insights derived from comprehensive claims data are fueling the development of more customized and data-driven insurance products. This could lead to policies that are dynamically priced based on real-time risk factors and offer tailored risk management services.

In conclusion, a loss run is an indispensable document in the realm of insurance. It serves as a detailed historical record of claims, offering invaluable insights for both insurers and policyholders. By understanding its components, significance, and how to effectively obtain and utilize it, businesses and individuals can navigate the insurance landscape with greater confidence, secure more appropriate coverage, and ultimately mitigate risks more effectively. As technology continues to advance, the role and sophistication of loss runs and the data they represent will undoubtedly continue to grow, shaping the future of risk management and insurance.