The concept of a grace period is a pivotal, yet often misunderstood, feature of credit cards that can profoundly impact a cardholder’s financial health. Essentially, a grace period is a designated window of time following the close of a billing cycle during which new purchases can be paid off in full without incurring interest charges. It serves as a crucial buffer, offering cardholders a chance to manage their finances proactively and avoid unnecessary costs. Understanding how this period functions and how to leverage it effectively is fundamental for anyone looking to optimize their credit card usage and maintain good financial standing.

Understanding the Grace Period

At its core, the grace period is designed to reward responsible credit card usage. It’s a standard feature on most credit cards, though its specifics can vary slightly depending on the issuer and the card agreement.

The Basic Definition

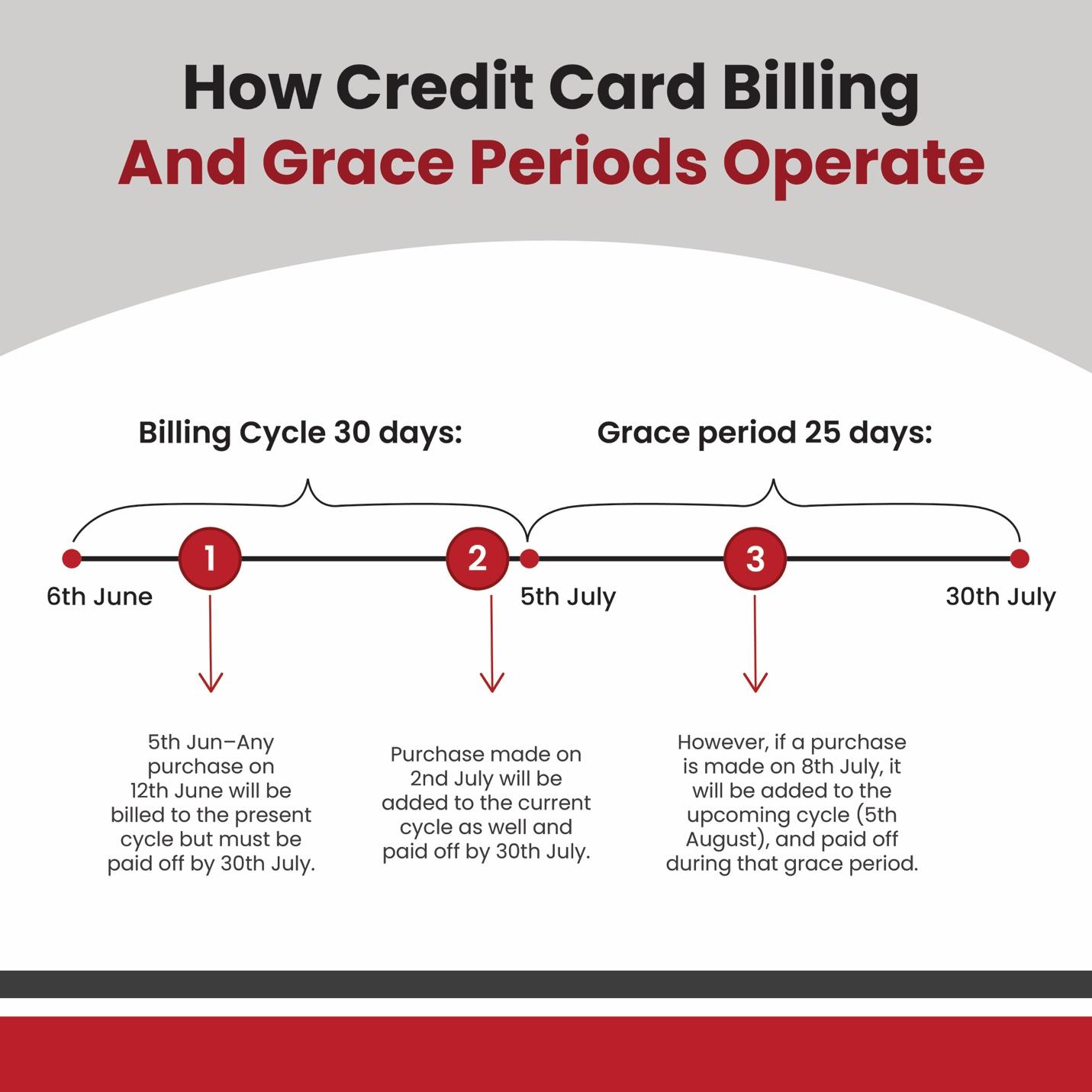

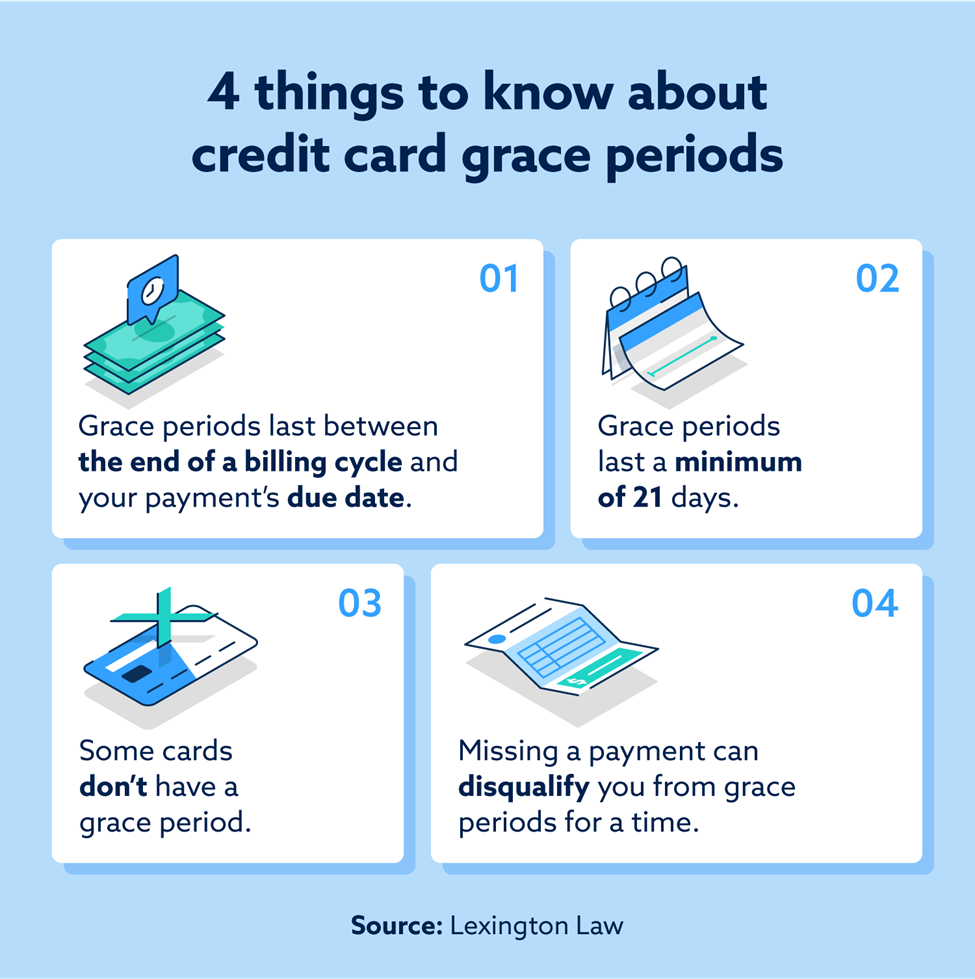

A grace period is the interval between the end of your credit card’s billing cycle and the payment due date, during which you can pay your credit card balance without being charged interest on new purchases. For instance, if your billing cycle ends on January 1st and your payment due date is January 26th, you have a 25-day grace period for any new purchases made within that cycle. If you pay your entire statement balance by January 26th, those new purchases will not accrue interest. It is important to distinguish this from the overall time a bill is outstanding; the grace period specifically relates to interest-free payment.

How It Works

The mechanics of a grace period are straightforward for new purchases. Your credit card statement typically details your billing cycle dates, the closing date, and the payment due date. Let’s consider a practical example:

- Billing Cycle Start: January 1st

- Billing Cycle End (Statement Close Date): January 30th

- Payment Due Date: February 24th

In this scenario, any new purchases made between January 1st and January 30th will appear on the statement generated around January 30th. You then have until February 24th (approximately 25 days) to pay that statement balance in full. If you do, no interest will be charged on those purchases. If you only pay a portion of the balance or miss the due date, interest will typically be applied to the remaining balance from the date of purchase, retroactively eliminating the benefit of the grace period. This is a critical point: the grace period is usually only effective if you pay your entire statement balance by the due date.

Why the Grace Period Matters for Cardholders

Leveraging the grace period can lead to significant financial advantages, transforming a credit card from a potential debt trap into a powerful financial management tool.

Avoiding Interest Charges

The most immediate and obvious benefit of the grace period is the ability to avoid interest charges. Credit card interest rates can be notoriously high, often ranging from 15% to 25% APR or even higher. Without a grace period, interest would start accruing from the moment a purchase is made. By consistently paying off your full statement balance before the due date, you effectively use the credit card as an interest-free loan for up to several weeks, which can save you hundreds or even thousands of dollars in interest over time. This interest-free window is a primary reason many financially savvy individuals prefer using credit cards over debit cards for daily spending.

Strategic Financial Management

Beyond just saving money on interest, the grace period allows for strategic financial management. It provides flexibility, enabling cardholders to align their spending with their income cycles. For example, if you get paid bi-weekly, you can time your larger purchases to fall early in your billing cycle, giving you nearly a month and a half before the payment is due, coinciding with multiple paychecks. This allows for better cash flow management and reduces the immediate strain on your bank account for large expenses. Furthermore, by using credit cards for all purchases and paying them off within the grace period, cardholders can earn rewards (cash back, points, miles) on all their spending without incurring any interest, effectively getting paid to use their credit. This combination of no interest and earned rewards makes the grace period a cornerstone of intelligent credit card utilization.

Factors Affecting Your Grace Period

While the concept of a grace period is universal, certain conditions and types of transactions can negate or modify its benefits. It’s crucial to understand these nuances to avoid inadvertently incurring interest.

New Purchases vs. Cash Advances

Grace periods almost exclusively apply to new purchases. They typically do not apply to cash advances. When you take a cash advance from your credit card, interest usually begins accruing immediately from the transaction date, with no grace period whatsoever. This is why cash advances are generally ill-advised and considered an expensive way to borrow money, given their high interest rates and often accompanying fees. Similarly, balance transfers sometimes have their own specific interest terms, and while some promotional balance transfers may offer an introductory 0% APR, the standard grace period for new purchases does not extend to them once the promotional period ends.

Balances Carried Over

Perhaps the most critical factor affecting your grace period is whether you carry a balance from one month to the next. If you do not pay your entire statement balance in full by the due date, you typically lose your grace period for new purchases in the subsequent billing cycle. This means that interest on all new purchases will begin accruing immediately from the transaction date, rather than waiting until the next payment due date. To reinstate the grace period, you must pay your total outstanding balance in full for at least one entire billing cycle. This “grace period reset” can take careful planning and disciplined payment to re-establish. Many cardholders fall into the trap of only paying the minimum due, which not only keeps them in debt but also continuously subjects new purchases to immediate interest charges.

Promotional Offers and Balance Transfers

Credit card companies often entice new customers with promotional offers, such as 0% APR on purchases or balance transfers for an introductory period (e.g., 6, 12, or 18 months). During these promotional periods, interest is not charged on the qualifying balances, effectively creating an extended grace period. However, it is vital to read the terms carefully. Once the promotional period ends, standard APRs apply, and if any balance remains, interest will begin to accrue. For balance transfers, the standard grace period for new purchases often remains intact, but the transferred balance itself adheres to its specific promotional terms or standard APR. Understanding these distinct terms is essential to manage different types of balances on a single card effectively.

Maximizing Your Grace Period Benefits

To truly harness the power of your credit card’s grace period, a disciplined approach and clear understanding of your card’s terms are paramount.

Paying Your Statement Balance in Full

The golden rule for benefiting from a grace period is to pay your entire statement balance in full every single month before the payment due date. This might sound simple, but it requires diligent tracking of spending and budgeting. By doing so, you avoid all interest charges on new purchases, maintain an excellent payment history (a key factor in credit scores), and effectively use the credit card as a convenience tool rather than a debt instrument. Automating your full statement balance payment through your bank or the credit card issuer’s portal can be an effective strategy to ensure timely payments and prevent accidental loss of your grace period.

Understanding Your Billing Cycle

Familiarizing yourself with your credit card’s billing cycle is key to strategic spending. Know when your cycle starts and ends, and when your payment due date is. This knowledge allows you to make larger purchases early in the billing cycle, maximizing the interest-free period you receive. Conversely, if you’re approaching the end of a cycle and need to make a significant purchase that you can’t pay off immediately, it might be more strategic to wait for the next billing cycle to begin. This timing can grant you almost an additional month to pay off the purchase without interest. Your monthly statement will clearly outline these dates, making it easy to track.

Monitoring Your Statements

Regularly reviewing your credit card statements is not just about checking for fraudulent activity; it’s also essential for understanding your grace period. Your statement will clearly show your current balance, the minimum payment due, and the total statement balance. It will also indicate your payment due date. By cross-referencing this information with your spending habits and payment schedule, you can ensure that you are always paying the correct amount by the correct date to avoid interest and maintain your grace period benefit. Always pay the “statement balance” shown on your most recent bill, not just the “current balance,” as the current balance may include recent purchases that are part of the next billing cycle. Consistent monitoring empowers you to make informed financial decisions and keep your credit card working for you, not against you.