The Internal Revenue Service (IRS) utilizes a variety of forms to manage tax obligations, and one of particular importance for individuals who expect to owe taxes beyond what is withheld from their paychecks is Form 1040-ES, Estimated Tax for Individuals. This form serves as the foundation for calculating and paying estimated taxes throughout the year. Understanding its purpose, how to use it, and when it’s applicable is crucial for avoiding penalties and ensuring smooth tax compliance. Unlike traditional tax payments made with a single annual filing, estimated tax is a pay-as-you-go system designed to allow taxpayers to meet their tax liability in installments, mirroring the way wages are typically taxed through withholding.

Understanding Estimated Tax Obligations

Estimated tax is essentially a method of paying income tax and other taxes, such as self-employment tax and alternative minimum tax, that are not collected through withholding from wages or by other means. If you are an employee, your employer withholds taxes from each paycheck based on the information you provide on Form W-4, Employee’s Withholding Certificate. However, for individuals who earn income from sources where tax isn’t automatically withheld, or if the withholding is insufficient, they are generally required to make estimated tax payments.

Who Needs to Pay Estimated Tax?

Several categories of individuals typically fall under the umbrella of estimated tax payers. The most common scenarios include:

- Self-Employed Individuals: This is arguably the largest group that needs to consider estimated tax. If you operate your own business, work as an independent contractor, or have freelance income, taxes are not withheld by a client or customer. You are responsible for calculating and paying these taxes yourself. This includes income tax and self-employment taxes (Social Security and Medicare taxes).

- Individuals with Significant Investment Income: If you receive substantial income from sources like interest, dividends, capital gains, or rent, and these amounts are not subject to withholding, you may need to pay estimated tax. The threshold for when this becomes applicable often depends on the total amount of income you expect to receive.

- Retirees Receiving Pensions or Annuities: While some pensions and annuities may have withholding options, others do not. If you receive retirement income and taxes are not being withheld, you might need to make estimated tax payments.

- Individuals with Other Income Not Subject to Withholding: This can encompass a broad range of income, including unemployment benefits (in most states, you can elect to have federal income tax withheld, but if you don’t, estimated tax might be necessary), alimony payments received under divorce decrees finalized before January 1, 2019, and income from partnerships or S corporations where you are a partner or shareholder and the entity does not withhold taxes on your behalf.

The IRS has specific guidelines for when estimated tax payments are required. Generally, if you expect to owe at least $1,000 in tax for the year after subtracting your withholding and any refundable tax credits, you are likely required to make estimated tax payments. It’s important to remember that this is a general rule, and specific circumstances can alter the requirement. The goal is to avoid a substantial tax bill at the end of the year and to prevent underpayment penalties.

The “Pay-As-You-Go” System

The concept of estimated tax is rooted in the pay-as-you-go approach to taxation. The U.S. tax system is designed so that tax liability is paid throughout the year as income is earned, rather than all at once when the annual tax return is filed. For most employees, this is achieved through automatic withholding by their employer. For those with income not subject to withholding, Form 1040-ES provides the framework for them to replicate this pay-as-you-go system. By making quarterly payments, taxpayers can distribute their tax burden evenly over the year, which can be more manageable from a budgeting perspective and helps avoid the shock of a large tax bill.

Calculating Your Estimated Tax Liability

The core of using Form 1040-ES involves accurately calculating how much tax you are likely to owe for the entire tax year. This calculation is an estimate, and it’s perfectly normal for it to be adjusted as your income or deductions change throughout the year. The form itself provides worksheets to guide you through this process.

The Estimated Tax Worksheet

The Form 1040-ES package typically includes a worksheet designed to help you determine your estimated tax. The steps involved generally include:

- Estimating Your Adjusted Gross Income (AGI): This involves projecting all your expected income for the year and subtracting certain above-the-line deductions. For self-employed individuals, this would include their business income minus deductible business expenses. For investors, it would include anticipated interest, dividends, and capital gains.

- Calculating Your Taxable Income: From your estimated AGI, you’ll subtract your standard deduction or itemized deductions, whichever is greater, and any qualified business income deduction.

- Determining Your Total Tax: You then apply the appropriate tax rates to your estimated taxable income to calculate your projected income tax liability. This step also requires accounting for any additional taxes, such as self-employment tax, net investment income tax, or alternative minimum tax.

- Subtracting Credits: Any tax credits you expect to qualify for (e.g., child tax credit, education credits) are then subtracted from your total tax liability.

- Calculating Your Estimated Tax Due: The remaining amount is your estimated tax.

Self-Employment Tax Calculation

For individuals who are self-employed, a significant portion of their estimated tax obligation will be self-employment tax. This tax covers Social Security and Medicare contributions. The tax rate for self-employment tax is 15.3% on the first $168,600 of earnings for 2024 (this amount is adjusted annually for inflation), plus 2.9% on all earnings for Medicare tax.

A key aspect of calculating self-employment tax is that you can deduct one-half of your self-employment tax from your gross income when calculating your adjusted gross income. This deduction effectively reduces your overall income tax liability. The worksheet on Form 1040-ES helps integrate this calculation, ensuring that both income tax and self-employment tax are accounted for.

Adjusting Your Estimates

Life is unpredictable, and so is income. It’s important to understand that you are not locked into your initial estimate for the entire year. If your income significantly increases or decreases, or if your deductions or credits change, you should recalculate your estimated tax. You can do this by using the worksheet on a new Form 1040-ES and adjusting your future payments accordingly. This proactive approach can help you avoid overpaying or underpaying your taxes and thus facing penalties.

Making Your Estimated Tax Payments

Once you have calculated your estimated tax liability, the next step is to make the payments. The IRS provides several convenient methods for submitting these payments.

Payment Due Dates

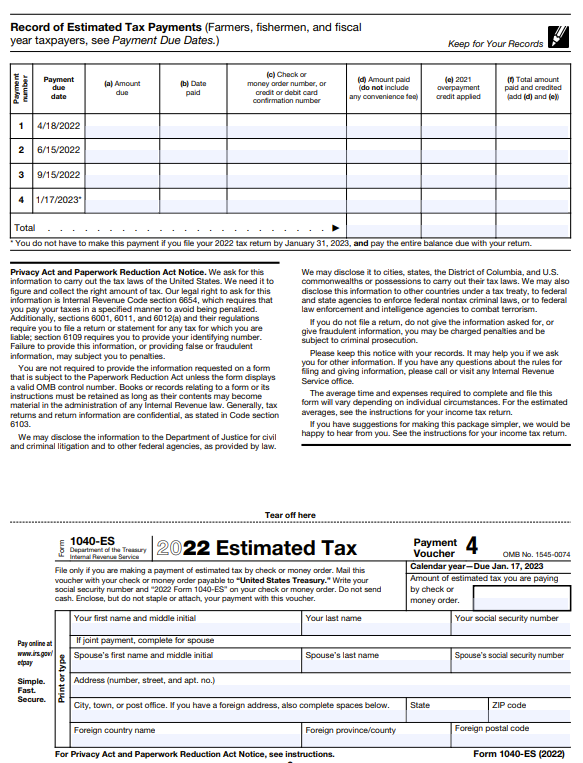

Estimated taxes are typically paid in four equal installments throughout the year. The due dates are generally set as follows:

- Payment 1: For income earned January 1 to March 31 – Due April 15.

- Payment 2: For income earned April 1 to May 31 – Due June 15.

- Payment 3: For income earned June 1 to August 31 – Due September 15.

- Payment 4: For income earned September 1 to December 31 – Due January 15 of the following year.

If a due date falls on a weekend or legal holiday, the payment is due on the next business day. It’s crucial to meet these deadlines to avoid potential penalties for late payments.

Payment Methods

The IRS offers multiple ways to remit your estimated tax payments:

- Online Payment: The IRS website offers the Electronic Federal Tax Payment System (EFTPS), a free and secure service that allows you to make payments directly from your bank account. Many taxpayers find this to be the most convenient and reliable method. You can schedule payments in advance.

- By Mail: You can mail a check or money order along with the payment voucher (Voucher Form 1040-ES) to the address specified in the Form 1040-ES instructions. It’s important to use the correct voucher for the tax year and payment period.

- Phone: Payments can also be made by phone through various methods, often linked to EFTPS or through a third-party payment processor.

- Direct Debit: You can authorize an electronic direct debit from your bank account when filing your return electronically or through a tax professional.

The Payment Voucher

When you download or receive a copy of Form 1040-ES, it includes payment vouchers. Each voucher is for a specific payment period. You would fill out the voucher with your name, address, Social Security number, and the amount of the payment for that period. These vouchers are used when you choose to pay by mail. When using EFTPS or other electronic methods, you typically don’t need to fill out a physical voucher.

Avoiding Penalties and Interest

One of the primary reasons for understanding and diligently using Form 1040-ES is to avoid penalties and interest charged by the IRS. The IRS expects taxpayers to pay their tax liability as they earn income. If you don’t pay enough tax throughout the year through withholding or estimated tax payments, you may be subject to an underpayment penalty.

When the Underpayment Penalty Applies

The penalty is generally applied if you owe at least $1,000 in tax when you file your return, after subtracting your withholding and any tax credits. The penalty is calculated based on the amount of the underpayment, the period it was underpaid, and the applicable interest rate for underpayments.

Exceptions and Waivers

There are specific situations where the IRS may waive the underpayment penalty. These include:

- The 90% Rule: If you owe less than 10% of the tax shown on your tax return for the current tax year.

- The 100% Rule (or 110% Rule for Higher-Income Taxpayers): If the tax you paid through withholding and timely estimated tax payments is at least 100% of the tax shown on your prior-year tax return. For higher-income taxpayers (those with an AGI over $150,000, or $75,000 if married filing separately), this threshold increases to 110% of the prior-year tax.

- Reasonable Cause: The penalty may be waived if you can show that the failure to make payments was due to reasonable cause and not willful neglect. This often applies in cases of casualty events, natural disasters, or unexpected illness or death.

- First Year of Eligibility: If you were a U.S. citizen or resident alien for the entire prior tax year, did not have any tax liability in that prior year, and the prior tax year was a 12-month period, you are not subject to the penalty for the current year.

It’s crucial to stay informed about these rules and to make your payments on time and in sufficient amounts to avoid these penalties. Keeping good records of your income, deductions, and estimated tax payments is essential for demonstrating compliance.

Conclusion

Form 1040-ES is more than just a tax form; it’s an essential tool for financial planning and tax compliance for a significant portion of taxpayers. It empowers individuals with variable income streams to meet their tax obligations responsibly and avoid the potentially significant financial penalties associated with underpayment. By understanding who needs to file, how to calculate their liability, when and how to make payments, and the importance of avoiding penalties, taxpayers can navigate the complexities of estimated taxes with confidence, ensuring a smoother and less stressful tax season. Regularly reviewing your income and tax situation and adjusting your estimated payments as needed is key to effectively managing your tax responsibilities throughout the year.