A fiscal period, also known as an accounting period, is a defined span of time over which financial activities are recorded, summarized, and reported. It serves as a crucial framework for businesses and organizations to track their financial performance, assess their economic health, and make informed decisions. Without a standardized period, it would be nearly impossible to compare results over time, measure profitability accurately, or fulfill tax obligations. These periods are fundamental to the principles of accrual accounting, which mandates the recognition of revenues when earned and expenses when incurred, regardless of when cash is actually exchanged. Understanding the concept and structure of fiscal periods is paramount for anyone involved in financial management, from small business owners to large corporate executives and even individual investors seeking to analyze company performance.

The duration of a fiscal period can vary, but the most common are monthly, quarterly, and annually. The choice of period length is often dictated by regulatory requirements, industry norms, and the specific reporting needs of the organization. For instance, publicly traded companies are typically required to report their financial results on a quarterly and annual basis to satisfy investor and regulatory demands. Smaller businesses might opt for monthly reporting to maintain closer oversight of their operations and cash flow. The calendar year (January 1st to December 31st) is a natural choice for many entities, but some organizations elect to use a fiscal year that does not align with the calendar year. This is often done to better match their accounting cycle with their seasonal business operations or to take advantage of specific tax planning opportunities.

Types and Durations of Fiscal Periods

The flexibility in defining a fiscal period allows businesses to tailor their financial reporting to their unique operational rhythms. While standard durations are prevalent, the underlying principle remains consistent: a discrete block of time for financial assessment.

Monthly Fiscal Periods

A monthly fiscal period, as the name suggests, encompasses one calendar month. These periods are valuable for businesses that require granular insights into their financial performance and cash flow on a frequent basis. Small businesses, startups, and companies with rapidly changing market conditions often benefit from monthly reporting.

Advantages of Monthly Reporting

- Timely Performance Monitoring: Monthly reports allow for immediate identification of trends, deviations from budget, and potential issues. This enables swift corrective actions.

- Enhanced Cash Flow Management: Regular monitoring of income and expenses helps businesses proactively manage their cash reserves, preventing liquidity crises.

- Early Detection of Anomalies: Unusual transactions or errors can be spotted and addressed more quickly within a shorter reporting cycle.

- Improved Budgeting and Forecasting: Monthly data provides a solid foundation for refining future budgets and forecasts, making them more accurate and responsive to current realities.

- Facilitates Performance Reviews: Managers can conduct regular performance evaluations of departments or projects, fostering accountability and driving improvements.

Challenges of Monthly Reporting

- Increased Administrative Burden: Compiling and analyzing financial data every month requires significant time and resources, especially for smaller accounting teams.

- Potential for Short-Term Focus: An overemphasis on monthly results might lead to decisions that prioritize short-term gains over long-term strategic objectives.

- Seasonal Fluctuations Can Skew Perceptions: Businesses with highly seasonal sales or expenses might find that monthly comparisons can be misleading without proper seasonal adjustments.

Quarterly Fiscal Periods

A quarterly fiscal period spans three consecutive months. This is a widely adopted reporting cycle, particularly for publicly traded companies and larger organizations. It strikes a balance between the detailed insights of monthly reporting and the broader perspective of annual reporting.

Advantages of Quarterly Reporting

- Regulatory Compliance: Public companies are generally mandated by securities regulators (like the SEC in the US) to file quarterly financial statements (e.g., 10-Q in the US).

- Investor Relations: Quarterly reports provide investors with regular updates on a company’s progress, enabling them to make informed investment decisions.

- Strategic Performance Review: Quarterly periods are long enough to smooth out minor month-to-month fluctuations, offering a more representative view of performance trends.

- Mid-Year Adjustments: The second and third quarters serve as critical junctures for assessing progress against annual goals and making necessary adjustments to strategies.

Considerations for Quarterly Reporting

- Less Granular Than Monthly: While providing a good overview, quarterly reports may miss some of the day-to-day operational nuances that monthly reports can capture.

- Potential for Lag: By the time a quarterly report is released, a significant portion of the subsequent quarter may have already passed, potentially delaying the response to emerging issues.

Annual Fiscal Periods

An annual fiscal period covers twelve consecutive months. This is the most comprehensive reporting period, culminating in the preparation of annual financial statements. It provides a holistic view of a company’s financial performance over an entire year.

Significance of Annual Reporting

- Year-End Financial Statements: Annual reports are essential for producing audited financial statements, which are often required by lenders, investors, and regulatory bodies.

- Long-Term Performance Evaluation: They offer the broadest perspective for assessing a company’s profitability, financial position, and cash flows over an extended period.

- Tax Filings: Annual financial data forms the basis for a company’s income tax returns.

- Strategic Planning: The annual report is a critical document for evaluating the effectiveness of strategies implemented throughout the year and for setting the stage for the next fiscal year’s planning.

- Shareholder Communication: Annual reports are a primary means of communicating the company’s performance and future outlook to shareholders, often accompanied by an annual general meeting.

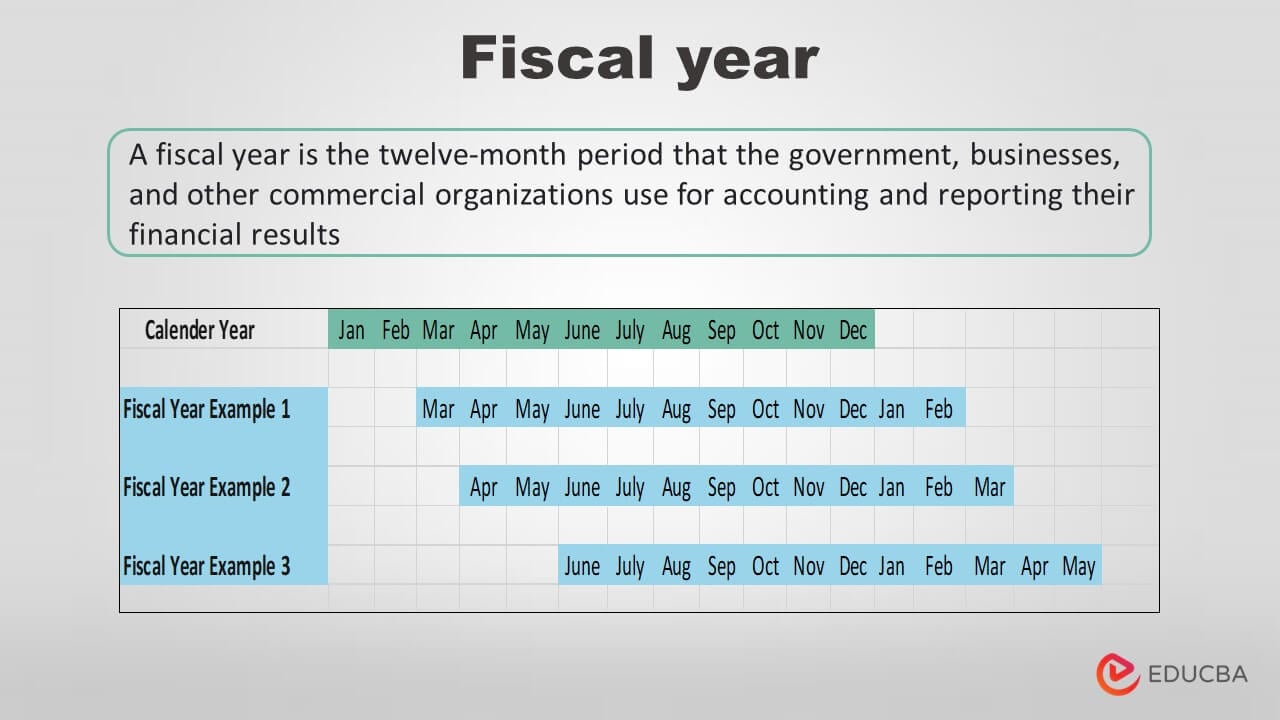

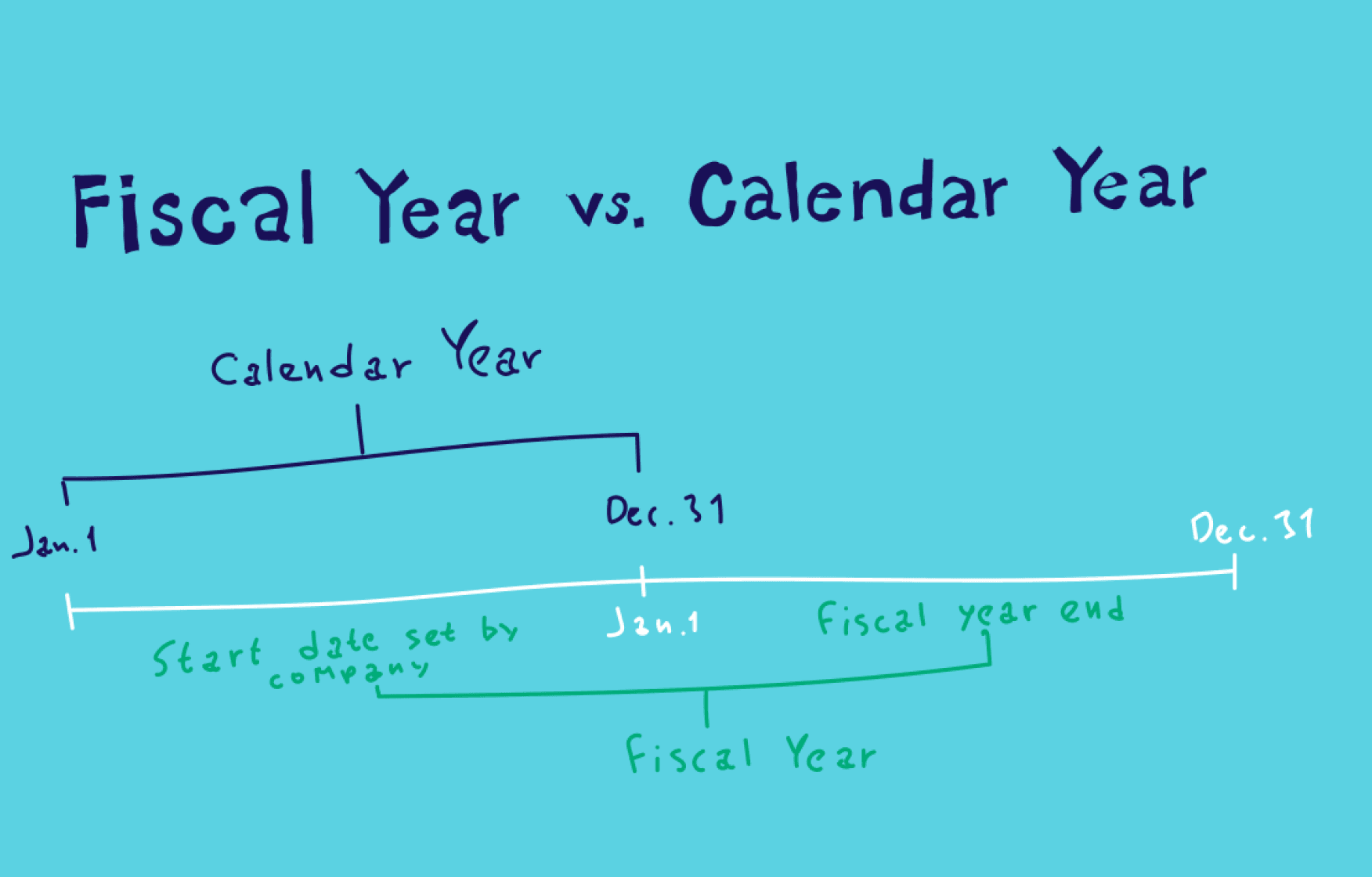

The Fiscal Year vs. Calendar Year Distinction

While many businesses operate on a calendar year fiscal period, others adopt a fiscal year that differs. This decision is strategic and often linked to operational cycles.

- Calendar Year: A fiscal period that aligns with the calendar year, running from January 1st to December 31st. This is common for businesses with operations that are not significantly tied to specific seasons.

- Fiscal Year: A fiscal period of twelve months that does not necessarily coincide with the calendar year. For example, a retail business with its peak sales during the holiday season might choose a fiscal year that ends in January or February to capture the full impact of its busiest period and then have a period of lower activity for year-end closing and inventory. Another example is a company whose primary business is agriculture, where its fiscal year might align with its harvest cycle.

The selection of a fiscal year has implications for tax planning and reporting. Companies must clearly define and consistently adhere to their chosen fiscal year.

The Accounting Cycle and Fiscal Periods

The fiscal period is intrinsically linked to the accounting cycle, the systematic process of recording, classifying, and summarizing financial transactions. Each fiscal period represents a complete iteration of this cycle.

Steps in the Accounting Cycle within a Fiscal Period

- Journalizing Transactions: At the outset of a fiscal period, all financial transactions (sales, purchases, payments, receipts) are recorded chronologically in journals.

- Posting to the Ledger: These journal entries are then transferred to the appropriate accounts in the general ledger, which categorizes the transactions by type (e.g., cash, accounts receivable, sales revenue, rent expense).

- Preparing a Trial Balance: At the end of the fiscal period, a trial balance is prepared. This is a list of all ledger accounts and their balances, ensuring that the total debits equal the total credits.

- Making Adjusting Entries: Before financial statements can be finalized, adjusting entries are made to account for accruals and deferrals, ensuring that revenues and expenses are recognized in the period they are earned or incurred, regardless of cash flow. Examples include accrued expenses, prepaid expenses, and unearned revenues.

- Preparing an Adjusted Trial Balance: A new trial balance is created after the adjusting entries are posted to confirm that debits still equal credits.

- Preparing Financial Statements: Based on the adjusted trial balance, the core financial statements are generated:

- Income Statement (or Profit and Loss Statement): Reports revenues, expenses, and the resulting net income or loss for the fiscal period.

- Balance Sheet: Presents a snapshot of the company’s assets, liabilities, and equity at the end of the fiscal period.

- Statement of Cash Flows: Details the cash inflows and outflows from operating, investing, and financing activities during the fiscal period.

- Closing Entries: At the end of an annual fiscal period (and sometimes at the end of interim periods), closing entries are made to reset temporary accounts (revenues, expenses, dividends) to zero, preparing them for the next fiscal period. These entries transfer the net income or loss to retained earnings.

- Post-Closing Trial Balance: A final trial balance is prepared to ensure that only permanent (balance sheet) accounts have balances and that debits equal credits.

This cyclical process ensures that financial data is accurately captured and presented for each defined fiscal period.

Importance and Applications of Fiscal Periods

The disciplined application of fiscal periods underpins the entire edifice of financial management and reporting. They are not merely arbitrary time segments but essential tools for accountability, analysis, and strategic planning.

Financial Reporting and Compliance

As previously mentioned, fiscal periods are the bedrock of financial reporting. Whether it’s for internal management, external investors, creditors, or regulatory bodies, financial statements are always prepared for a specific period. This standardization is vital for:

- Comparability: Enabling year-over-year, quarter-over-quarter, or month-over-month comparisons of financial performance. This allows stakeholders to identify trends, assess growth, and evaluate the effectiveness of management strategies.

- Auditability: Providing a defined scope for auditors to examine the financial records and express an opinion on the fairness of the financial statements.

- Taxation: Governments require financial information organized by fiscal periods to assess tax liabilities. Businesses use their fiscal period to calculate taxable income.

Performance Measurement and Decision Making

For internal management, fiscal periods serve as critical checkpoints for evaluating operational success.

- Budget Variance Analysis: By comparing actual financial results against budgeted figures for a specific period, management can identify areas where performance is exceeding or falling short of expectations. This allows for timely intervention and adjustments.

- Profitability Analysis: Understanding profit margins and overall profitability within a given period is crucial for making decisions about pricing, product lines, and operational efficiency.

- Resource Allocation: Performance data from fiscal periods informs decisions about how to allocate financial and human resources for future periods.

Strategic Planning

The insights gleaned from analyzing financial performance across multiple fiscal periods are indispensable for long-term strategic planning.

- Trend Identification: Recognizing patterns in revenue growth, cost structures, and cash flows over several fiscal years helps in forecasting future performance and identifying opportunities or threats.

- Goal Setting: Historical performance data provides a realistic basis for setting ambitious yet achievable financial and operational goals for upcoming fiscal periods.

- Investment Decisions: Investors and management use historical financial data, structured by fiscal periods, to assess the long-term viability and potential returns of investments.

In essence, a fiscal period provides the necessary structure to transform raw financial data into meaningful information that drives informed business decisions, ensures accountability, and facilitates transparent communication with all stakeholders. It is the fundamental building block upon which financial health and strategic direction are assessed and managed.