The term “EFT debit” might sound like a technical phrase encountered in the realm of cutting-edge flight systems, perhaps relating to propulsion or electronic flight control. However, in the context of financial transactions, an EFT debit refers to an Electronic Funds Transfer initiated as a withdrawal from an account. While its origins and primary application lie firmly within the financial sector, understanding its mechanics can offer insights into the digital processes that underpin many modern technologies, including those used in advanced drone operations.

Understanding Electronic Funds Transfer (EFT)

Electronic Funds Transfer (EFT) is a broad term that encompasses any transfer of funds initiated through electronic means. It represents a significant shift from traditional paper-based transactions, such as writing checks or making cash payments. EFT systems facilitate the movement of money between bank accounts, credit card accounts, or other financial instruments without the direct physical exchange of currency. These systems are the backbone of modern commerce, enabling everything from direct deposit of salaries to online purchases and automated bill payments.

The Mechanics of EFT

At its core, an EFT transaction involves a set of instructions transmitted electronically between financial institutions. When you authorize an EFT, you are essentially giving permission for your bank or financial institution to send funds from your account to another specified account. This process typically involves a secure network, often facilitated by payment processors and clearinghouses, that ensures the accurate and timely transfer of funds. The speed of EFT can vary, with some transfers happening almost instantaneously (like peer-to-peer payment apps) while others might take a business day or two, depending on the banks involved and the type of transaction.

Types of EFT Transactions

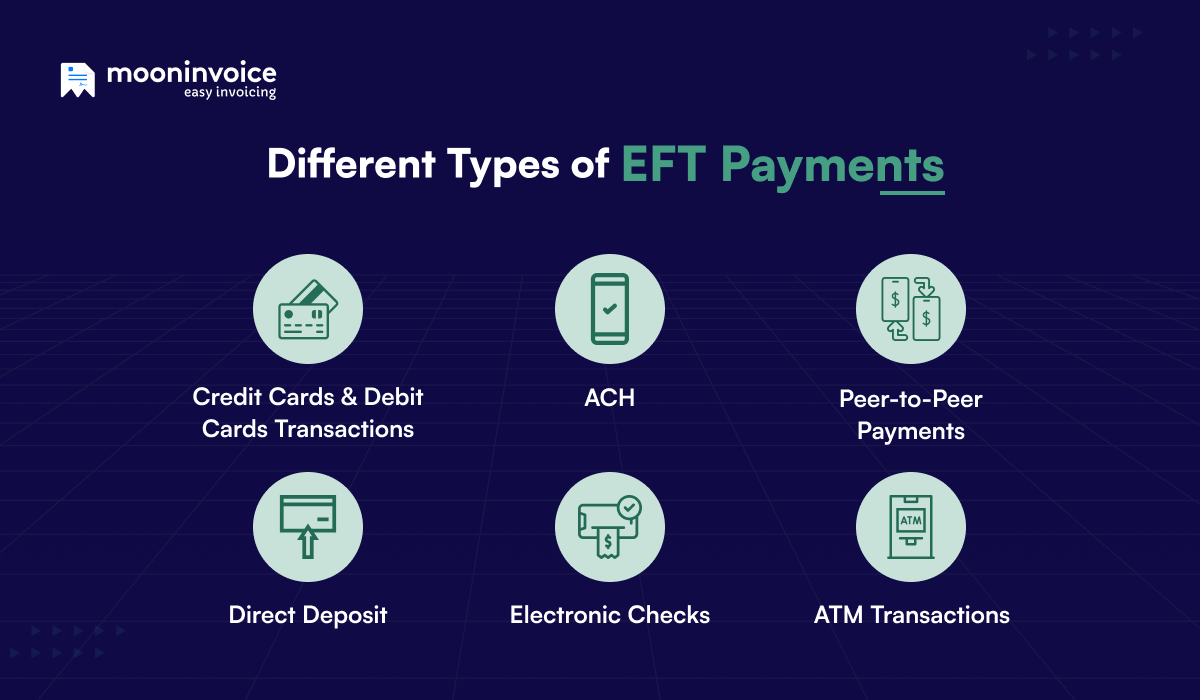

EFT encompasses a wide array of transaction types. These include:

- Direct Deposit: Funds automatically deposited into an account, such as salaries or government benefits.

- Direct Payment (or ACH Debit): Funds automatically withdrawn from an account to pay a bill or service. This is the most common form of “EFT debit” from a consumer’s perspective.

- Wire Transfers: A faster, often more expensive method for transferring large sums of money electronically between banks.

- ATM Transactions: Withdrawals, deposits, and balance inquiries made at automated teller machines.

- Point-of-Sale (POS) Transactions: Payments made using debit or credit cards at retail terminals.

- Online Bill Payments: Payments initiated through a company’s website or a bank’s online portal.

The common thread uniting these diverse transactions is the use of electronic signals to move money, eliminating the need for paper checks or physical cash.

Delving into EFT Debits

An EFT debit, specifically, refers to an electronic transfer of funds out of a specific account. This means money is being withdrawn or debited from your account. In the context of a consumer, this most frequently occurs when you authorize a company to automatically withdraw funds from your bank account to cover recurring expenses. This is commonly known as a direct debit or an automated clearing house (ACH) debit.

How Direct Debits Work

To set up a direct debit, you typically provide your bank account details (account number and routing number) and authorize the company to initiate electronic withdrawals. This authorization is crucial and is usually done by signing a form or agreeing to terms and conditions online. Once authorized, the company can then electronically request funds from your bank on predetermined dates. This is incredibly convenient for managing regular payments such as:

- Utility Bills: Electricity, gas, water, and internet services.

- Mortgage or Rent Payments: Ensuring timely housing payments.

- Loan Repayments: Car loans, student loans, or personal loans.

- Subscription Services: Gym memberships, streaming services, or software subscriptions.

- Insurance Premiums: Health, car, or home insurance.

The primary benefit for consumers is the elimination of late fees and the hassle of remembering to make manual payments each month. For businesses, it ensures a predictable cash flow and reduces administrative overhead associated with processing manual payments.

The Role of ACH in EFT Debits

The Automated Clearing House (ACH) network plays a pivotal role in facilitating EFT debits. The ACH network is a U.S. electronic network for financial transactions. It is managed by Nacha (formerly the National Automated Clearing House Association) and is used by financial institutions to process electronic payments and direct deposit. When you authorize an EFT debit, the originating company’s bank sends a request through the ACH network to your bank, which then debits your account and credits the originating company’s bank. This process is highly automated, efficient, and secure.

Security and Consumer Protection in EFT Debits

While EFT debits offer convenience and efficiency, security and consumer protection are paramount. Regulations are in place to safeguard consumers from unauthorized debits and to provide recourse if an error occurs.

Regulation E and Consumer Rights

In the United States, Regulation E of the Consumer Financial Protection Bureau (CFPB) governs electronic fund transfers. This regulation provides consumers with specific rights and protections related to EFTs, including EFT debits. Key protections include:

- Disclosure Requirements: Financial institutions must provide consumers with clear disclosures about their EFT rights and responsibilities. This includes information on how to report errors and unauthorized transactions.

- Error Resolution: Consumers have the right to report suspected errors or unauthorized transactions. Financial institutions are required to investigate these claims promptly and provide a resolution within a specified timeframe.

- Unauthorized Transaction Liability: Regulations limit consumer liability for unauthorized EFT transactions. If an unauthorized transaction is reported promptly, the consumer’s liability is typically capped or eliminated entirely.

- Periodic Statements: Consumers receive periodic statements from their financial institutions that detail all EFT transactions, allowing them to review their account activity and identify any discrepancies.

Preventing and Reporting Unauthorized Debits

While EFT debit systems are generally secure, the risk of unauthorized debits exists. This can happen due to identity theft, data breaches, or errors. Consumers can take several steps to protect themselves:

- Monitor Bank Statements Regularly: Reviewing account statements frequently is the first line of defense. Look for any transactions you don’t recognize.

- Set Up Account Alerts: Many banks offer real-time alerts for transactions above a certain amount or for any debit activity.

- Be Cautious with Personal Information: Share bank account details only with trusted and reputable companies.

- Understand Authorization: Always understand what you are authorizing when you agree to direct debits. Keep records of your authorizations.

If an unauthorized debit is discovered, it’s crucial to act quickly. Contact your bank or financial institution immediately to report the transaction. They will guide you through the process of disputing the charge and initiating an investigation.

The Broader Implications of EFT Debits

Beyond individual consumer convenience, EFT debits have had a profound impact on the financial landscape and the broader economy. Their widespread adoption has contributed to:

- Increased Efficiency in Business Operations: Companies can automate their billing and payment collection processes, reducing administrative costs and improving cash flow management. This efficiency can translate into lower prices or improved services for consumers.

- Reduced Paper Usage: The shift from paper checks to electronic transfers significantly reduces the environmental impact associated with paper production and transportation.

- Enhanced Financial Inclusion: EFT systems can make financial services more accessible to a wider population, especially in developing economies where traditional banking infrastructure may be limited.

- Facilitation of New Business Models: Many modern subscription-based services and online platforms rely heavily on the ease and automation provided by EFT debits to manage recurring payments.

While the term “EFT debit” might initially sound complex, it fundamentally describes a straightforward and highly beneficial method of electronic money transfer. Its pervasive integration into our daily financial lives underscores its importance as a cornerstone of modern digital commerce and financial management. By understanding how EFT debits work and the protections in place, consumers can leverage their benefits while staying secure.