Navigating the complexities of personal and business finance can often feel like deciphering an ancient code. Among the many terms and concepts that frequently arise, “tax deductions” stand out as a crucial element for managing your financial obligations effectively. Understanding what a tax deduction is, how it functions, and what types are available can significantly impact your tax liability, leading to substantial savings. This article delves into the world of tax deductions, providing a comprehensive overview for individuals and businesses alike.

Understanding the Fundamentals of Tax Deductions

At its core, a tax deduction is an expense that can be subtracted from your taxable income, thereby reducing the amount of income on which you owe taxes. This fundamental concept is a cornerstone of most tax systems, designed to provide financial relief and incentivize certain behaviors or expenditures.

The Difference Between Deductions and Credits

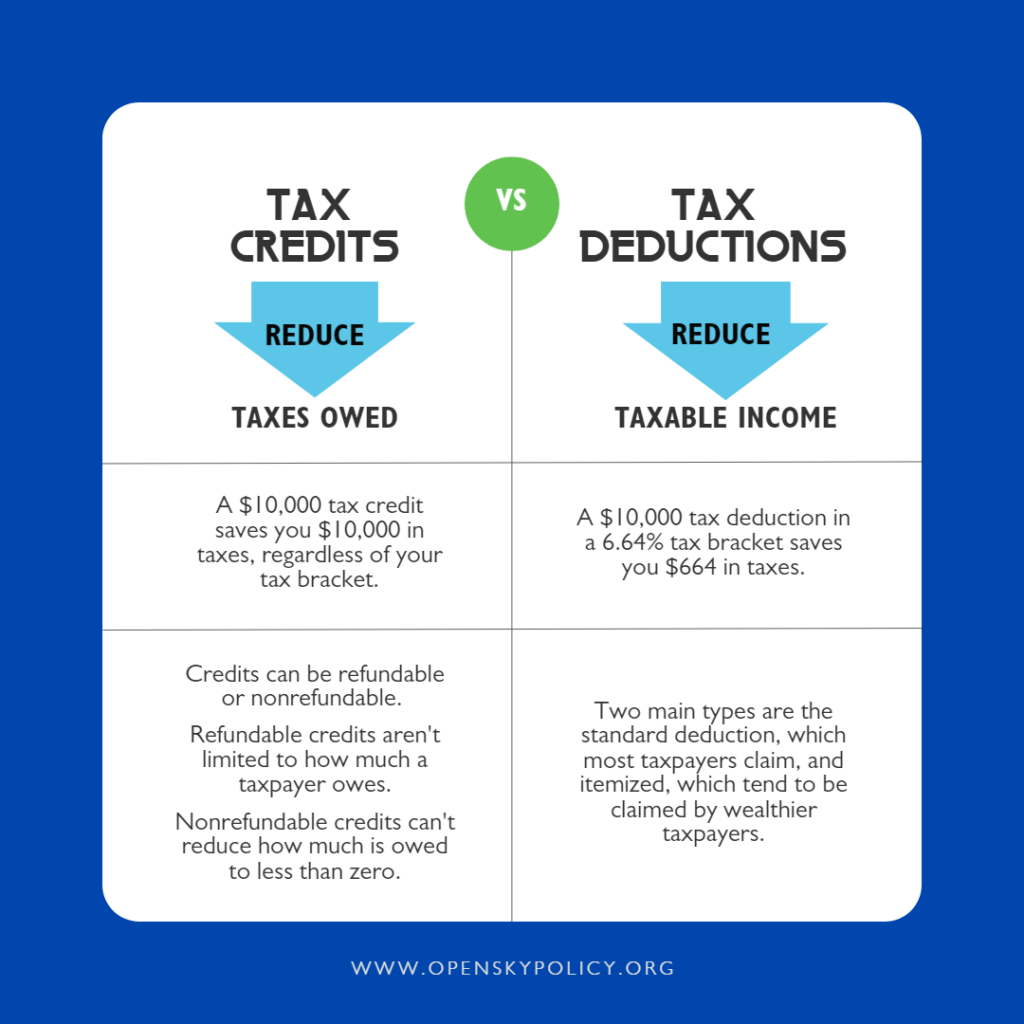

It’s essential to differentiate tax deductions from tax credits, as they serve distinct purposes and have different impacts on your tax bill. While both reduce your tax burden, they do so in fundamentally different ways.

Tax Credits: Direct Reduction of Tax Owed

Tax credits directly reduce the amount of tax you owe. For example, a $1,000 tax credit will lower your tax bill by exactly $1,000. This makes tax credits incredibly valuable. They can be non-refundable, meaning they can reduce your tax liability down to zero but won’t result in a refund of any unused credit, or refundable, which means if the credit exceeds your tax liability, you can receive the difference back as a refund.

Tax Deductions: Reduction of Taxable Income

Tax deductions, on the other hand, reduce your taxable income. If you are in the 22% tax bracket, a $1,000 deduction would reduce your tax bill by $220 (22% of $1,000). While the direct dollar-for-dollar saving isn’t as impactful as a credit, deductions can still lead to significant savings, especially for individuals and businesses with substantial deductible expenses. The value of a deduction is determined by your marginal tax rate; the higher your tax bracket, the more valuable each deduction becomes.

How Deductions Reduce Your Tax Bill

The mechanism by which deductions work is straightforward. Your gross income, which is all the income you earn from various sources, is the starting point for tax calculations. From this gross income, you can subtract certain allowable expenses, known as deductions. This results in your adjusted gross income (AGI). Certain deductions are taken “above the line” and are subtracted directly from gross income to arrive at AGI. Other deductions are taken “below the line,” typically as itemized deductions or the standard deduction, which are subtracted from AGI to arrive at your taxable income. The final tax liability is then calculated based on this taxable income, applying the relevant tax rates.

Above-the-Line vs. Below-the-Line Deductions

- Above-the-Line Deductions: These are subtracted from your gross income to determine your adjusted gross income (AGI). They are generally considered more beneficial because they reduce your AGI, which can in turn affect your eligibility for other tax benefits or deductions that are limited based on AGI. Examples include contributions to traditional IRAs, student loan interest, and self-employment tax deductions.

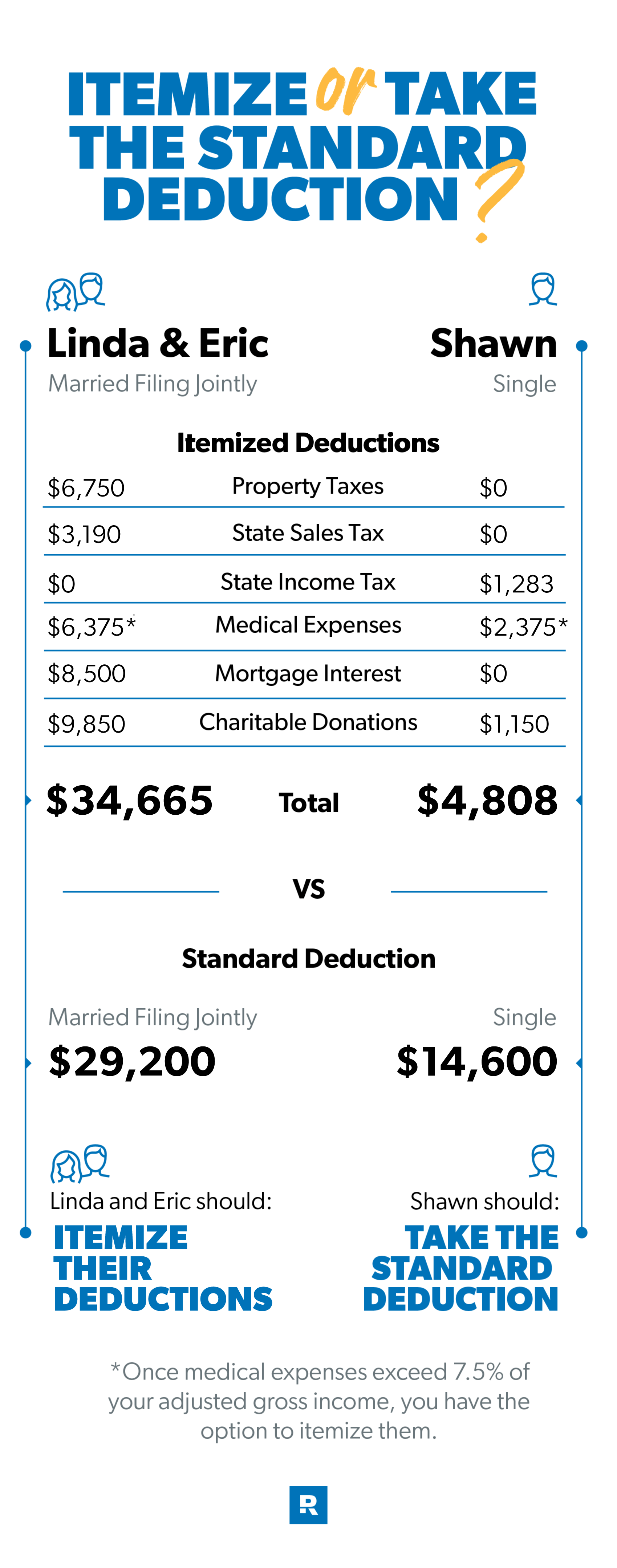

- Below-the-Line Deductions: These are subtracted from your AGI to arrive at your taxable income. Taxpayers generally choose between taking the standard deduction or itemizing their deductions. The standard deduction is a fixed dollar amount that depends on your filing status (e.g., single, married filing jointly). Itemizing involves listing out all your eligible deductible expenses and subtracting the total from your AGI. You would choose to itemize only if your total itemized deductions exceed the standard deduction. Common itemized deductions include medical expenses (above a certain threshold), state and local taxes (SALT) up to a limit, home mortgage interest, and charitable contributions.

Common Types of Tax Deductions

The range of potential tax deductions is broad, encompassing expenses related to personal finance, business operations, and specific societal contributions. Understanding these categories can help individuals and businesses identify opportunities for tax savings.

Deductions for Individuals

For individuals, deductions often relate to personal expenses that are deemed socially beneficial or are considered unavoidable costs of living. These can significantly reduce the tax burden for households.

Standard Deduction vs. Itemized Deductions

As mentioned, individuals have a choice between the standard deduction and itemizing. The standard deduction is a simplified option, offering a fixed dollar amount that reduces taxable income. Its value is adjusted annually for inflation. Itemizing allows taxpayers to claim specific deductible expenses if the total exceeds the standard deduction.

- Choosing the Right Path: To make this decision, you must track your eligible expenses throughout the year. Common itemized deductions include:

- Medical and Dental Expenses: You can deduct qualified medical and dental expenses that exceed a certain percentage of your AGI.

- State and Local Taxes (SALT): This includes state and local income taxes or sales taxes, as well as property taxes. There is a limit to the amount of SALT you can deduct annually.

- Home Mortgage Interest: Interest paid on a mortgage for your primary home or a second home is generally deductible, subject to certain limitations on the loan amount.

- Charitable Contributions: Donations to qualified charitable organizations can be deducted, often with limits based on the type of donation and your AGI.

Other Common Individual Deductions

Beyond the choice between the standard and itemized deductions, several “above-the-line” deductions can further reduce an individual’s taxable income.

- Student Loan Interest: Interest paid on qualified student loans is deductible, up to a certain annual limit.

- IRA Contributions: Contributions to a traditional IRA may be tax-deductible, depending on your income and whether you are covered by a retirement plan at work.

- Alimony Paid: For divorce or separation agreements executed before January 1, 2019, alimony payments are deductible by the payer and taxable to the recipient. For agreements executed after this date, alimony is generally not deductible.

- Health Savings Account (HSA) Contributions: Contributions made to an HSA are deductible, providing a tax-advantaged way to save for medical expenses.

Deductions for Businesses

Businesses, whether sole proprietorships, partnerships, or corporations, can deduct a wide array of expenses incurred in the ordinary course of their operations. These deductions are crucial for determining profitability and managing tax liabilities.

Operating Expenses

The most common business deductions are ordinary and necessary expenses incurred to run the business.

- Salaries and Wages: Compensation paid to employees is a significant deductible expense.

- Rent and Utilities: Costs associated with office space, workshops, or retail locations, including electricity, water, and internet, are deductible.

- Supplies and Materials: The cost of goods and materials used in the production of goods or services is deductible.

- Marketing and Advertising: Expenses for promoting products or services, such as online ads, print campaigns, and sponsorships, are deductible.

- Professional Fees: Payments to accountants, lawyers, consultants, and other service providers are typically deductible.

Depreciation

Depreciation is a method of accounting that allows businesses to recover the cost of tangible assets over their useful lives.

- Tangible Assets: This includes machinery, equipment, vehicles, and buildings. Instead of deducting the full cost of an asset in the year it’s purchased, depreciation allows for gradual deduction over several years. This can provide ongoing tax benefits.

- Depreciation Methods: Various methods exist, such as straight-line depreciation and accelerated depreciation, allowing businesses to choose the method that best suits their needs and tax strategy.

Business Travel and Meals

Expenses incurred while traveling for business purposes, and a portion of meal expenses, can be deductible.

- Business Travel: This includes transportation, lodging, and other costs associated with trips taken for legitimate business reasons.

- Business Meals: A significant portion of the cost of meals, if they are not lavish or extravagant and are directly related to the active conduct of the business, can be deducted.

Maximizing Your Tax Deductions

Effectively leveraging tax deductions requires careful planning, diligent record-keeping, and an understanding of the relevant tax laws. By adopting proactive strategies, individuals and businesses can ensure they are taking full advantage of available tax benefits.

The Importance of Record-Keeping

The foundation of claiming any tax deduction is robust and accurate record-keeping. Without proper documentation, deductions can be disallowed by tax authorities, leading to penalties and back taxes.

- Receipts and Invoices: Maintain all original receipts and invoices for deductible expenses. Digital copies are often acceptable, but it’s crucial to organize them logically.

- Mileage Logs: For business travel or deductible commuting, a detailed mileage log is essential, including dates, destinations, purpose of the trip, and miles driven.

- Bank Statements and Credit Card Records: These can serve as supplementary proof of expenses and should be cross-referenced with receipts.

- Categorization: Organize records by category (e.g., medical, charitable, business supplies) to simplify the tax preparation process.

Staying Informed About Tax Law Changes

Tax laws are subject to change, with new legislation, regulations, and court rulings constantly impacting what is deductible. Staying current is crucial for maximizing savings.

- Consult Tax Professionals: Certified Public Accountants (CPAs) or Enrolled Agents (EAs) are invaluable resources. They possess up-to-date knowledge of tax laws and can provide personalized advice.

- Official Tax Agency Resources: Websites of national tax agencies (e.g., IRS in the United States) provide official publications, forms, and guidance on tax laws and deductions.

- Reputable Financial News and Publications: Subscribing to or following reliable financial news outlets can keep you informed about significant tax policy changes.

Strategic Planning for Deductions

Beyond simply tracking expenses, strategic planning can help individuals and businesses proactively structure their finances to take advantage of deductions.

- Timing of Expenses: For some deductions, the timing of when an expense is paid or incurred can impact its deductibility in a given tax year. For example, a business might consider prepaying certain expenses before the end of the year to accelerate deductions.

- Business Structure: The choice of business structure (e.g., sole proprietorship, LLC, S-corp, C-corp) can affect the types of deductions available and how they are claimed.

- Investment Strategies: Certain investments, like those in retirement accounts or tax-advantaged savings plans, are designed with tax deductions or deferrals in mind.

In conclusion, tax deductions are a vital mechanism for reducing tax liability, offering financial relief and encouraging various economic activities. By understanding the fundamental differences between deductions and credits, recognizing the broad categories of available deductions for individuals and businesses, and committing to diligent record-keeping and strategic planning, taxpayers can effectively navigate the tax landscape and optimize their financial outcomes.