The world of car insurance can often feel like navigating a complex labyrinth, with a plethora of terms and concepts that can leave even the most seasoned driver feeling perplexed. Among these, the “deductible” stands out as a fundamental component that significantly impacts both the cost of your premium and the financial implications of a claim. Understanding what a deductible is, how it works, and its various implications is crucial for making informed decisions about your auto insurance policy. This article delves into the intricacies of car insurance deductibles, aiming to demystify this essential element and empower you to manage your coverage effectively.

Understanding the Core Concept: What is a Deductible?

At its heart, a deductible is the amount of money you, the policyholder, agree to pay out-of-pocket towards a covered car insurance claim before your insurance company begins to cover the remaining costs. Think of it as your personal contribution to any repair or replacement expenses that arise from an incident, such as a collision, theft, or damage from an event like a falling tree.

The Deductible’s Role in Policy Structure

Insurance policies are structured with deductibles as a risk-sharing mechanism between the insurer and the insured. By agreeing to bear a portion of the loss, you take on some financial responsibility, which in turn influences the overall cost of your insurance. Insurers view policyholders with higher deductibles as taking on more risk, which often translates into lower annual premiums. Conversely, a lower deductible means the insurer will shoulder a larger portion of the claim cost, leading to higher premiums.

Types of Deductibles: A Closer Look

It’s important to recognize that not all deductibles are created equal. The type of deductible you have is typically tied to the specific coverage under your policy.

Collision Deductible

This is perhaps the most commonly understood deductible. It applies when your vehicle is damaged in a collision with another object or vehicle, or if it overturns, regardless of fault. For instance, if you have a $500 collision deductible and your car sustains $3,000 in damage after an accident, you would pay the first $500, and your insurance company would cover the remaining $2,500.

Comprehensive Deductible

This deductible comes into play for damages to your vehicle that are not the result of a collision. This can include events such as theft, vandalism, fire, natural disasters (like hail or floods), or damage caused by falling objects. Similar to the collision deductible, if you have a $500 comprehensive deductible and your car is stolen with $5,000 worth of damage, you would pay $500, and the insurer would cover the rest.

Uninsured/Underinsured Motorist (UM/UIM) Deductible

This deductible is a bit more nuanced. In many states, UM/UIM coverage is mandatory and protects you if you’re involved in an accident with a driver who has no insurance or insufficient insurance to cover your damages. The deductible here typically applies to the “property damage” portion of your UM/UIM claim. For example, if an uninsured driver hits your car and the damage is $2,000, and you have a $250 UM deductible, you would pay $250, and the insurer would cover $1,750. It’s crucial to note that UM/UIM deductibles often do not apply to bodily injury claims.

Fixed vs. Percentage Deductibles

While most deductibles are fixed dollar amounts (e.g., $500, $1,000), some policies, particularly for comprehensive coverage, might offer a percentage-based deductible. This means your deductible would be a percentage of your car’s actual cash value (ACV) at the time of the loss. For example, a 1% deductible on a car valued at $20,000 would result in a $200 deductible. This type of deductible can fluctuate with the value of your vehicle.

The Interplay Between Deductibles and Premiums

The relationship between your chosen deductible and your insurance premium is a fundamental aspect of how car insurance pricing works. This dynamic is driven by the insurer’s assessment of risk and their potential payout in the event of a claim.

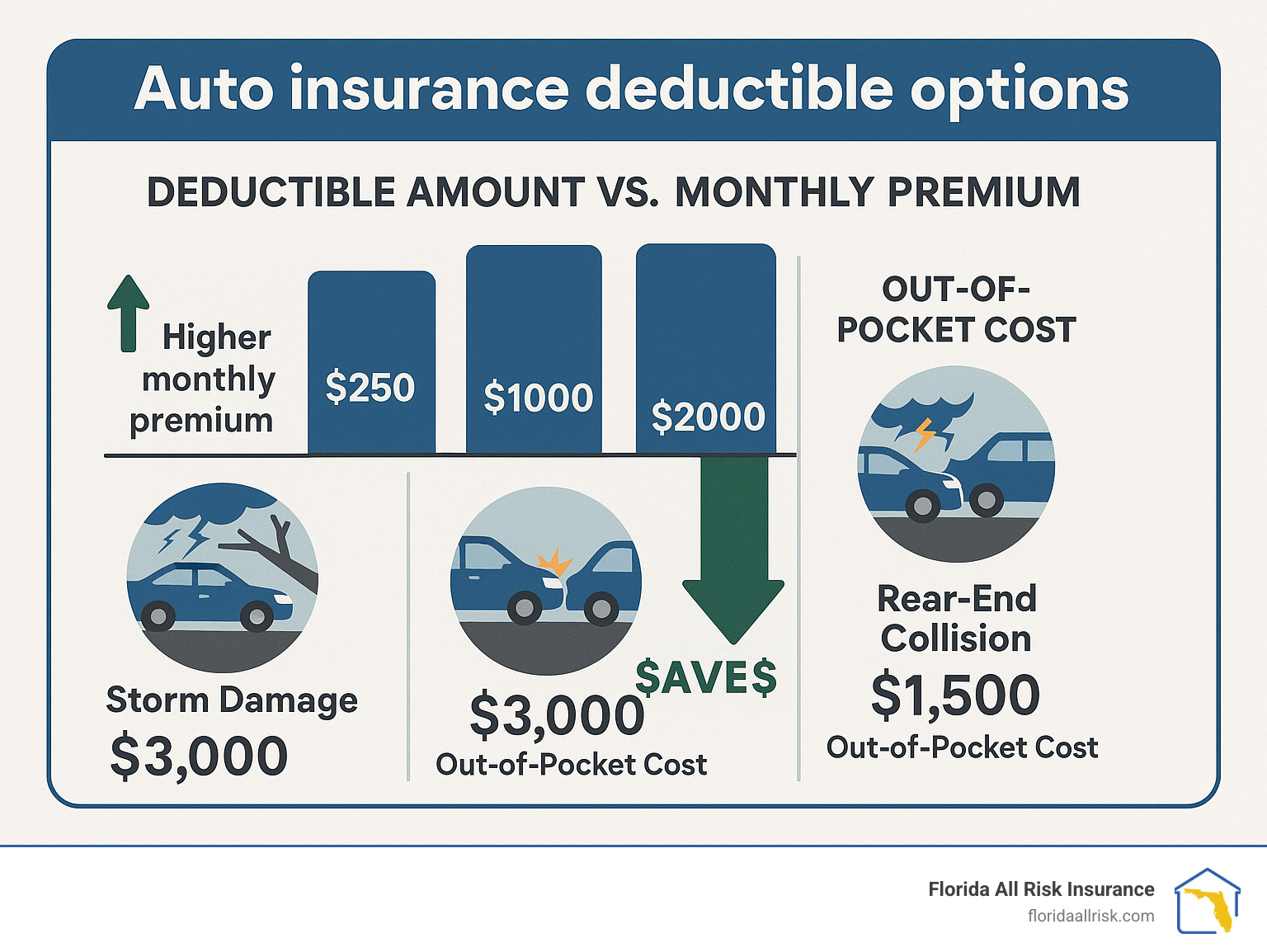

Higher Deductible, Lower Premium

Opting for a higher deductible is a direct strategy to lower your insurance premiums. When you agree to pay more out-of-pocket, you are essentially self-insuring a larger portion of potential losses. This reduces the financial risk for the insurance company, and they pass that savings onto you in the form of lower monthly or annual payments. For example, increasing your collision deductible from $500 to $1,000 could lead to a noticeable reduction in your overall premium.

Lower Deductible, Higher Premium

Conversely, selecting a lower deductible will result in higher premiums. With a lower deductible, the insurance company assumes a greater financial burden in the event of a claim. This increased risk is factored into the premium calculation, making your policy more expensive. While a lower deductible offers greater financial peace of mind for immediate out-of-pocket expenses after an incident, it comes at the cost of higher ongoing insurance payments.

Balancing Your Financial Needs

The optimal deductible for you is a personal decision that hinges on your financial situation and risk tolerance. Consider the following:

- Emergency Fund: Do you have sufficient savings to comfortably cover the deductible amount if you need to file a claim? If not, a lower deductible might be a wiser choice to avoid financial strain.

- Risk Tolerance: How comfortable are you with bearing a larger portion of the repair costs? Some individuals prefer the security of a lower deductible, even if it means paying more in premiums.

- Vehicle Value: For older, lower-value vehicles, the potential payout from a claim might be less than the cost of a higher deductible. In such cases, it might make more financial sense to pay for minor repairs out-of-pocket.

- Driving Habits and Risk Factors: If you drive frequently in high-traffic areas or live in a region prone to severe weather, you might be at a higher risk of filing a claim. This could influence your decision on the deductible level.

When Do You Pay Your Deductible?

Your deductible is only invoked when you file a claim for a covered loss. This means if you have a minor fender-bender that costs less to repair than your deductible, you would likely opt to pay for the repairs yourself rather than file an insurance claim. Filing a claim for a small amount can also lead to an increase in your premiums, making it less cost-effective.

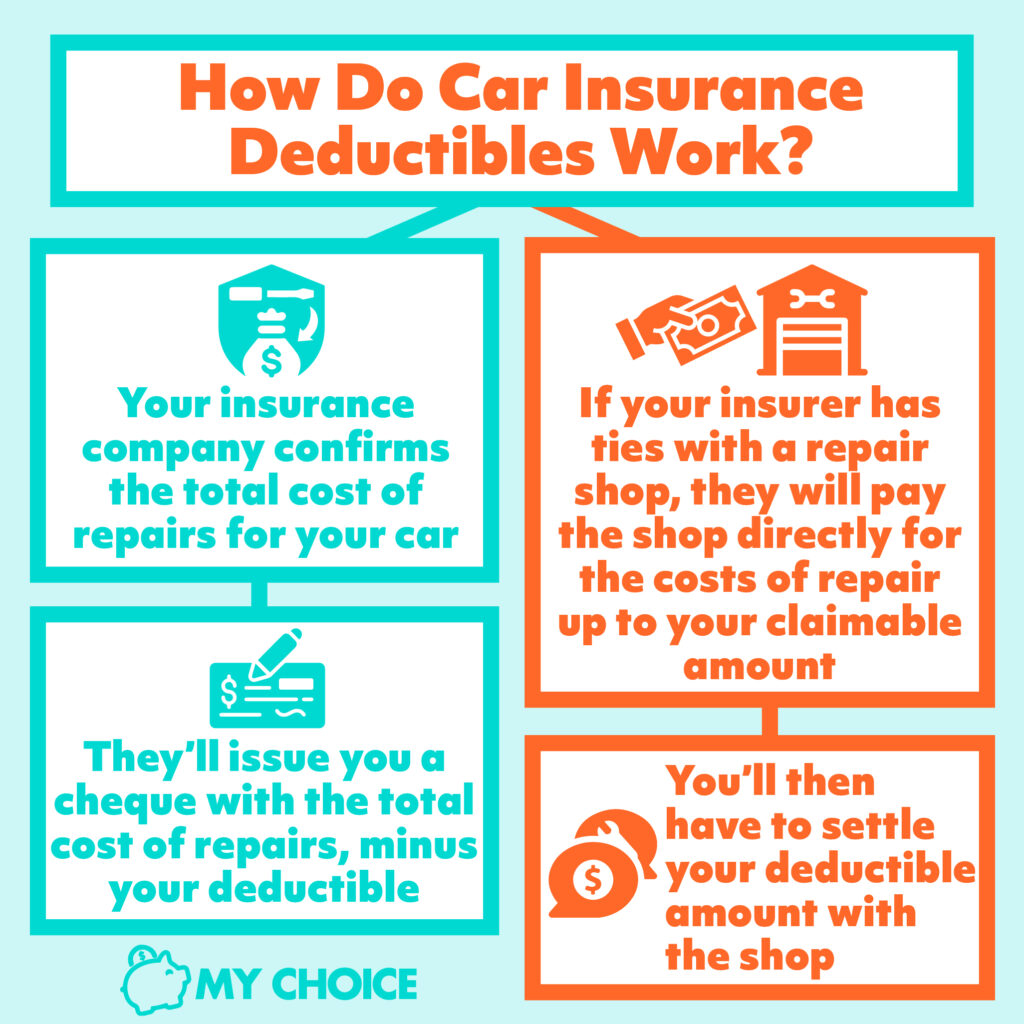

The Claim Process and Deductible Payment

Once a claim is initiated and deemed valid by your insurance company, they will assess the total cost of the damages. Before the insurer disburses any funds for repairs or replacement, you will be required to pay your deductible amount. This payment is typically made directly to the repair shop or dealership at the time of service. In some cases, especially with total loss settlements (like theft or an irreparable vehicle), the deductible is subtracted from the total payout by the insurance company.

Deductible Waivers: A Rare Exception

While not common, there are certain situations where a deductible might be waived. This usually occurs when the at-fault party in an accident is clearly identified and has insurance. In such scenarios, their insurance company would be responsible for covering the damages, and your deductible might not apply. However, the specifics of deductible waivers vary significantly by insurer and policy. It’s crucial to consult your policy documents and discuss this with your insurance agent.

Strategies for Optimizing Your Deductible

Choosing the right deductible is not a one-time decision. It’s a component of your insurance that can be reviewed and adjusted as your circumstances change.

Regular Policy Review

It’s advisable to review your car insurance policy, including your deductible selections, at least annually or whenever you experience a significant life event. This includes changes in income, savings, vehicle ownership, or driving patterns. A policy review ensures that your coverage still aligns with your current financial capabilities and risk tolerance.

Comparing Quotes with Different Deductible Levels

When shopping for new insurance or considering a switch, always compare quotes for various deductible options. This will give you a clear picture of the premium savings associated with higher deductibles and the cost of lower deductibles. This comparative approach is essential for finding the most cost-effective coverage for your needs.

Understanding Deductible Maximums

Be aware that your deductible is typically capped by the amount of the covered loss. You will never be asked to pay more than the actual cost of the damage, up to the limits of your coverage. For instance, if your deductible is $1,000 and the repair cost is $700, you will only pay $700.

In conclusion, understanding your car insurance deductible is paramount to managing your auto insurance effectively. It’s not merely a number on your policy; it’s a key factor that influences your financial exposure and the overall cost of your coverage. By grasping the nuances of deductibles, their impact on premiums, and the scenarios in which they apply, you can make well-informed decisions that provide both adequate protection and financial prudence. Regularly reviewing your policy and understanding your options will ensure your car insurance remains a valuable asset, safeguarding you against the unexpected without breaking the bank.