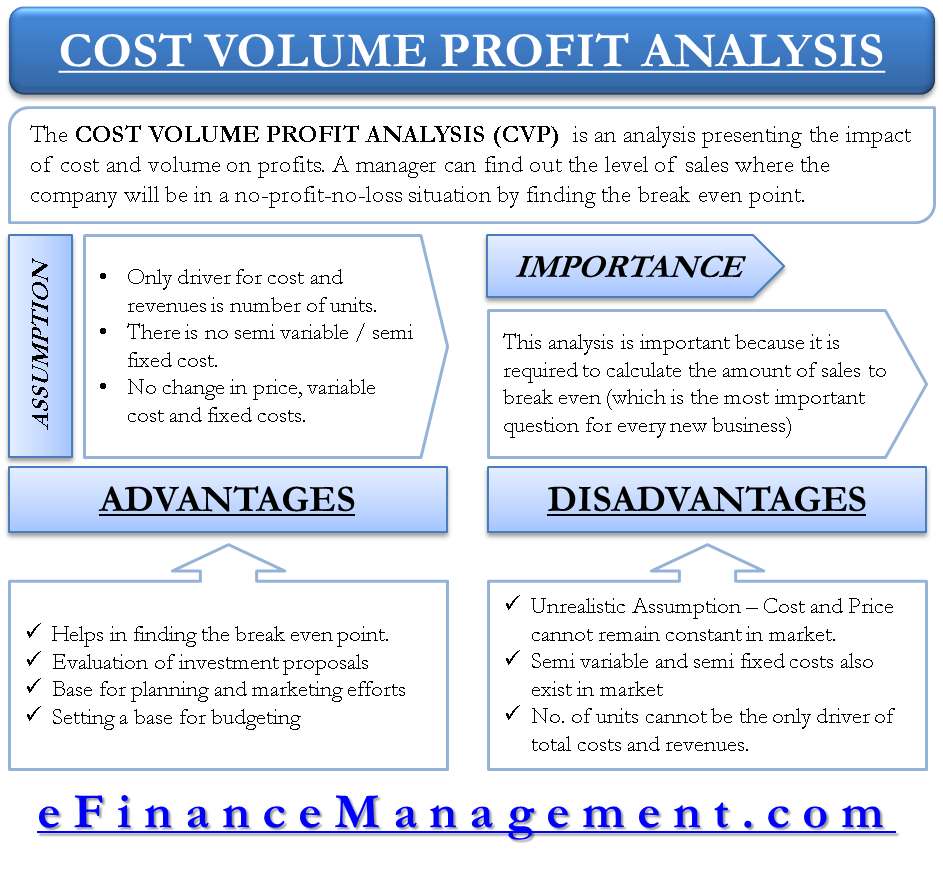

Cost-Volume-Profit (CVP) analysis is a fundamental management accounting tool that examines the relationship between the costs of producing a product or service, the volume of units sold, and the resulting profit. This powerful technique helps businesses understand how changes in sales volume, selling prices, variable costs, and fixed costs impact their profitability. By dissecting these key components, businesses can make informed decisions regarding pricing strategies, cost control measures, sales targets, and overall business planning. CVP analysis is particularly valuable for short-term decision-making and scenario planning, allowing managers to forecast the financial outcomes of various operational adjustments.

At its core, CVP analysis relies on a set of assumptions that simplify the complex realities of business operations. Understanding these assumptions is crucial for interpreting the results of the analysis accurately. The primary assumptions include:

- Linearity: Costs and revenues are assumed to behave linearly within a relevant range of activity. This means that variable costs per unit remain constant, and total variable costs increase proportionally with the number of units produced or sold. Similarly, the selling price per unit is assumed to be constant.

- Relevant Range: The analysis is valid only within a certain range of activity. Beyond this range, fixed costs might change (e.g., needing to rent additional factory space), or variable costs per unit might fluctuate due to economies or diseconomies of scale.

- Fixed vs. Variable Costs: Costs are clearly divisible into fixed and variable components. Fixed costs do not change in total with changes in activity level, while variable costs change in total directly with the level of activity. Mixed costs, which have both fixed and variable elements, are typically separated into their components.

- Constant Sales Mix: For businesses selling multiple products, the proportion in which these products are sold (the sales mix) is assumed to remain constant. This is important when calculating weighted-average contribution margins.

- No Inventory Changes: CVP analysis typically assumes that all units produced are sold within the period, meaning there are no significant changes in beginning or ending inventory levels. If inventory levels fluctuate, the analysis needs to account for the fixed manufacturing overhead assigned to the ending inventory.

The Core Components of CVP Analysis

The effectiveness of CVP analysis hinges on understanding its fundamental components: costs, volume, and profit. Each plays a critical role in determining the financial health and future potential of a business.

Fixed Costs

Fixed costs are expenses that do not change in total, regardless of the level of production or sales volume, within a relevant range. These costs are incurred even if no units are produced or sold. Examples of fixed costs include:

- Rent for factory or office space

- Salaries of administrative staff

- Depreciation of machinery (using straight-line method)

- Insurance premiums

- Property taxes

While fixed costs are constant in total, the fixed cost per unit decreases as the volume of production or sales increases. This is due to the spreading of the total fixed cost over a larger number of units. This phenomenon is a key driver of profitability as a business scales.

Variable Costs

Variable costs are expenses that change in total directly and proportionally with the level of production or sales volume. For each unit produced or sold, the variable cost per unit remains constant. Examples of variable costs include:

- Direct materials used in production

- Direct labor wages (paid on an hourly basis tied to production)

- Sales commissions (a percentage of sales revenue)

- Shipping costs per unit sold

The total variable cost increases as more units are produced or sold. Understanding and accurately estimating variable costs is crucial for determining the profitability of each unit sold.

Selling Price Per Unit

The selling price per unit is the amount at which each unit of product or service is sold to customers. In a basic CVP analysis, the selling price per unit is assumed to be constant. However, in reality, businesses may offer discounts for bulk purchases or engage in promotional pricing, which can affect this assumption.

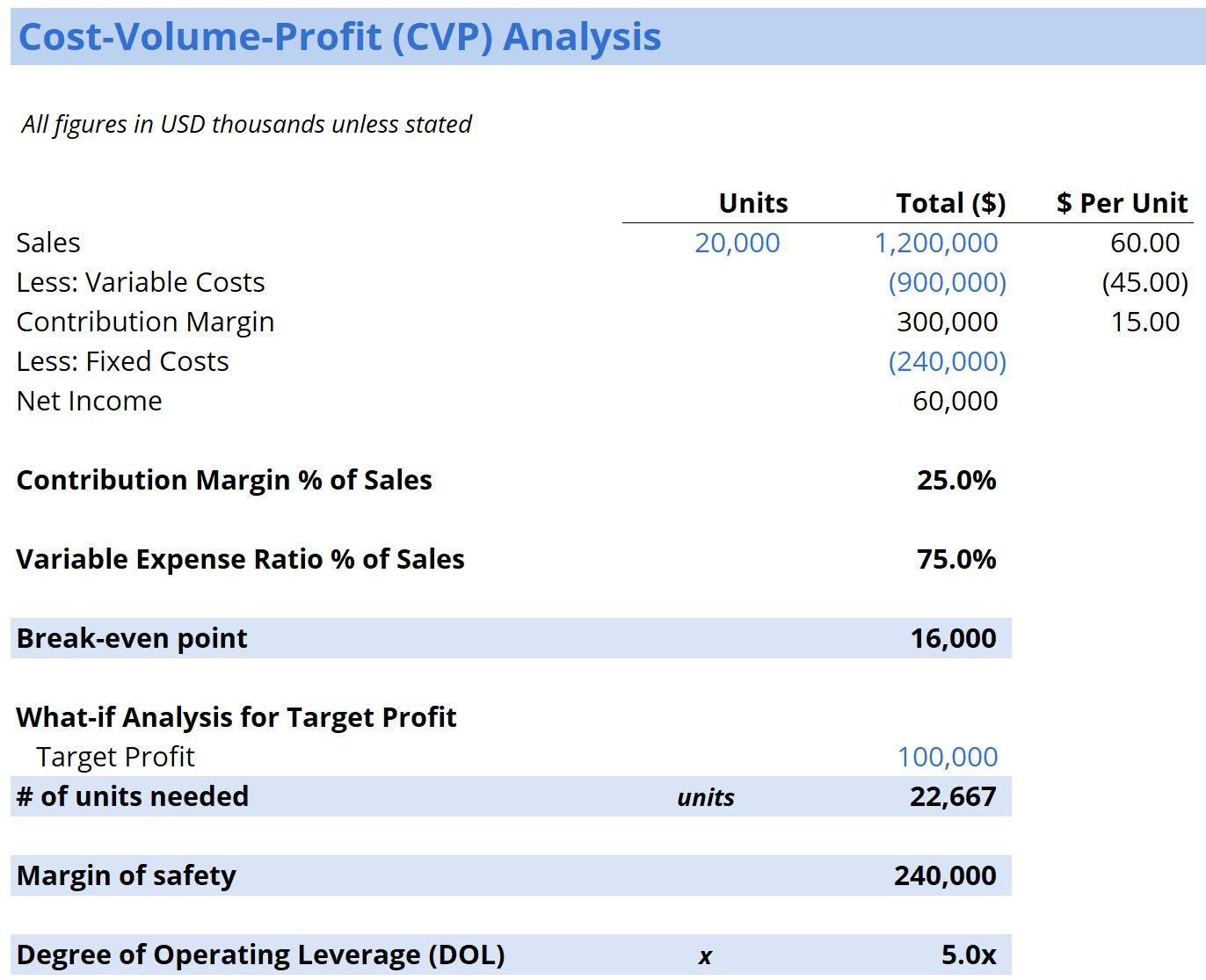

Contribution Margin

The contribution margin is a pivotal concept in CVP analysis. It represents the revenue remaining after deducting variable costs. This remaining amount “contributes” towards covering fixed costs and then generating profit. There are two ways to express contribution margin:

-

Contribution Margin Per Unit: This is calculated as:

- Contribution Margin Per Unit = Selling Price Per Unit – Variable Cost Per Unit

This figure tells us how much each individual unit sold contributes to covering fixed costs and generating profit.

- Contribution Margin Per Unit = Selling Price Per Unit – Variable Cost Per Unit

-

Contribution Margin Ratio: This is calculated as:

- Contribution Margin Ratio = Contribution Margin Per Unit / Selling Price Per Unit

or - Contribution Margin Ratio = Total Contribution Margin / Total Sales Revenue

The contribution margin ratio expresses the percentage of each sales dollar that is available to cover fixed costs and contribute to profit. A higher contribution margin ratio indicates that a larger portion of each sales dollar is available for profit.

- Contribution Margin Ratio = Contribution Margin Per Unit / Selling Price Per Unit

Profit

Profit, or net income, is the ultimate goal of any business. In CVP analysis, profit is calculated after all costs (both fixed and variable) have been accounted for. The fundamental profit equation in CVP analysis is:

- Profit = Total Sales Revenue – Total Variable Costs – Total Fixed Costs

This can also be expressed using the contribution margin:

- Profit = Total Contribution Margin – Total Fixed Costs

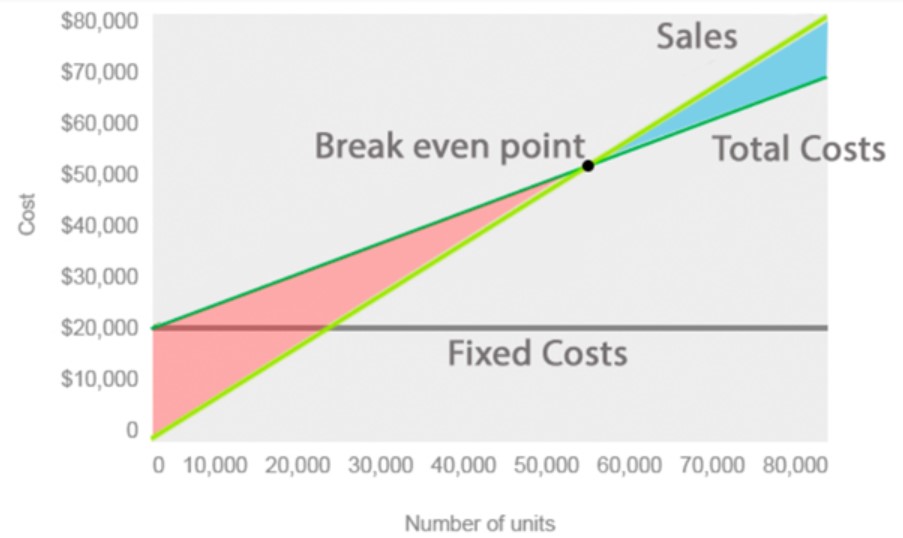

This equation highlights that once the total contribution margin generated from sales equals the total fixed costs, the business breaks even. Any sales beyond the break-even point contribute directly to profit.

Key Applications of CVP Analysis

CVP analysis is not just an academic exercise; it is a practical tool with wide-ranging applications that can profoundly impact business strategy and decision-making.

Break-Even Point Determination

One of the most common applications of CVP analysis is determining the break-even point (BEP). The break-even point is the level of sales (in units or in dollars) at which total revenues equal total costs, resulting in zero profit and zero loss.

-

Break-Even Point in Units:

- BEP (Units) = Total Fixed Costs / Contribution Margin Per Unit

This tells managers how many units they need to sell to cover all their costs.

- BEP (Units) = Total Fixed Costs / Contribution Margin Per Unit

-

Break-Even Point in Dollars:

- BEP (Dollars) = Total Fixed Costs / Contribution Margin Ratio

This indicates the total sales revenue required to cover all costs.

- BEP (Dollars) = Total Fixed Costs / Contribution Margin Ratio

Knowing the break-even point is essential for setting realistic sales targets, evaluating the feasibility of new products, and understanding the risk associated with a particular business venture. A lower break-even point generally signifies a less risky operation.

Target Profit Analysis

Beyond simply breaking even, businesses often set specific profit objectives. CVP analysis can be used to determine the sales volume required to achieve a desired profit target.

-

Units to Achieve Target Profit:

- Units = (Total Fixed Costs + Target Profit) / Contribution Margin Per Unit

By adding the target profit to the fixed costs, we essentially create a new “total cost” that must be covered by the contribution margin.

- Units = (Total Fixed Costs + Target Profit) / Contribution Margin Per Unit

-

Sales Revenue to Achieve Target Profit:

- Sales Revenue = (Total Fixed Costs + Target Profit) / Contribution Margin Ratio

This helps in understanding the revenue generation needed to meet financial goals.

- Sales Revenue = (Total Fixed Costs + Target Profit) / Contribution Margin Ratio

Target profit analysis is invaluable for strategic planning, budgeting, and motivating sales teams by providing clear financial objectives.

Sensitivity Analysis and Scenario Planning

CVP analysis is inherently a tool for understanding “what-if” scenarios. By changing one or more of the key variables (selling price, variable costs, fixed costs, or sales volume), managers can assess the potential impact on profit.

- Impact of Price Changes: How will a 5% increase in selling price affect profit if sales volume remains constant?

- Impact of Cost Reductions: What is the profit improvement if variable costs per unit are reduced by 10%?

- Impact of Increased Sales Volume: If sales volume increases by 20%, what will be the new profit level?

This ability to perform sensitivity analysis allows businesses to proactively identify potential challenges and opportunities and develop contingency plans. It helps in understanding the leverage of fixed costs, known as operating leverage. High operating leverage means that a small change in sales volume can lead to a large change in profit, making the business more sensitive to sales fluctuations.

Pricing Decisions

CVP analysis provides crucial insights for making informed pricing decisions. By understanding the contribution margin per unit and the break-even point, businesses can:

- Evaluate the impact of price changes on profitability: A price increase will boost profit per unit, but could it also reduce sales volume? CVP helps quantify this trade-off.

- Determine minimum acceptable prices: For special orders or promotional offers, CVP can help determine the lowest price that will still contribute positively towards fixed costs and profit.

- Analyze the effects of competitor pricing: How might a competitor’s price reduction impact our sales volume and overall profitability?

Product Mix Decisions

For companies offering multiple products, CVP analysis can be extended to consider the impact of different sales mixes on overall profitability. This involves calculating a weighted-average contribution margin based on the expected sales volume of each product. By understanding the relative profitability of different product combinations, businesses can focus marketing and sales efforts on the most lucrative mixes.

Limitations of CVP Analysis

While CVP analysis is a powerful tool, it’s important to be aware of its limitations to avoid misinterpretations and ensure its effective application.

- Assumption of Linearity: In reality, costs and revenues may not always behave linearly, especially over very large ranges of activity or in the long term. Variable costs per unit can change due to bulk purchasing discounts or production inefficiencies, and fixed costs can change in steps.

- Difficulty in Separating Costs: Accurately separating mixed costs into their fixed and variable components can be challenging and may require sophisticated statistical techniques.

- Constant Sales Mix: For businesses with many products, maintaining a constant sales mix can be difficult. Changes in customer preferences, market trends, or marketing campaigns can alter the sales mix, requiring recalibration of the analysis.

- No Consideration of Time Value of Money: CVP analysis is a static tool that does not account for the time value of money, which is important for long-term investment decisions.

- Focus on Short-Term: CVP is generally best suited for short-term decision-making. Long-term strategic decisions often require more complex analysis that considers factors like market share, competitive advantage, and economic conditions.

- Inventory Fluctuations: The standard CVP model assumes that production equals sales. If there are significant changes in inventory levels, adjustments are needed to account for the fixed manufacturing overhead allocated to inventory.

Despite these limitations, CVP analysis remains an indispensable technique for managers seeking to understand the core drivers of profitability and make sound operational decisions. By applying it thoughtfully and being mindful of its assumptions, businesses can gain valuable insights into their financial performance and chart a course towards greater success.