The realm of higher education often involves navigating a complex landscape of financial documentation, and among these, the Form 1098-E, Tuition Statement, plays a crucial role for students, parents, and educational institutions alike. This document serves as a vital piece of information for tax purposes, specifically concerning the deductibility of student loan interest. Understanding what a 1098-E is, who issues it, and how to interpret its contents is essential for anyone involved in financing post-secondary education.

The Purpose and Issuance of Form 1098-E

Form 1098-E is an informational tax return that is filed by educational institutions and lenders who receive student loan interest payments exceeding a certain threshold. Its primary purpose is to report the amount of student loan interest paid by a borrower during the tax year to the Internal Revenue Service (IRS) and to the borrower themselves. This information allows taxpayers to claim a deduction for the student loan interest they have paid, which can significantly reduce their overall tax liability.

Who Issues a 1098-E?

Several entities are responsible for issuing Form 1098-E. These typically include:

- Educational Institutions: Colleges, universities, and vocational schools that directly offer or administer student loans may issue a 1098-E if they receive more than $600 in interest from a student.

- Financial Institutions: Banks, credit unions, and other lending organizations that provide student loans are obligated to issue a 1098-E to borrowers if they have paid more than $600 in interest during the tax year. This includes private student loans and, in some cases, federal student loans serviced by private companies.

- Loan Servicers: Companies that manage the repayment of student loans on behalf of lenders or the government are also responsible for issuing Form 1098-E if the $600 interest threshold is met.

The threshold for issuing a 1098-E is generally $600 in student loan interest received by the payer. However, even if less than $600 in interest is paid, the institution or lender may still choose to issue the form. It is important to note that the 1098-E does not report the principal amount of the loan, nor does it report any amounts paid for tuition, fees, or other educational expenses. Its sole focus is on the interest paid on qualified student loans.

Key Information Contained Within Form 1098-E

The Form 1098-E is a relatively straightforward document, designed to present the essential information required for tax deductions. Understanding each section of the form is crucial for accurate tax preparation.

Identifying Information

At the top of the form, you will find the identifying information for both the payer (the institution or lender) and the recipient (the student or borrower). This includes names, addresses, and identification numbers (like the payer’s Employer Identification Number or the recipient’s Social Security Number). This ensures that the information is correctly associated with the right individuals and entities.

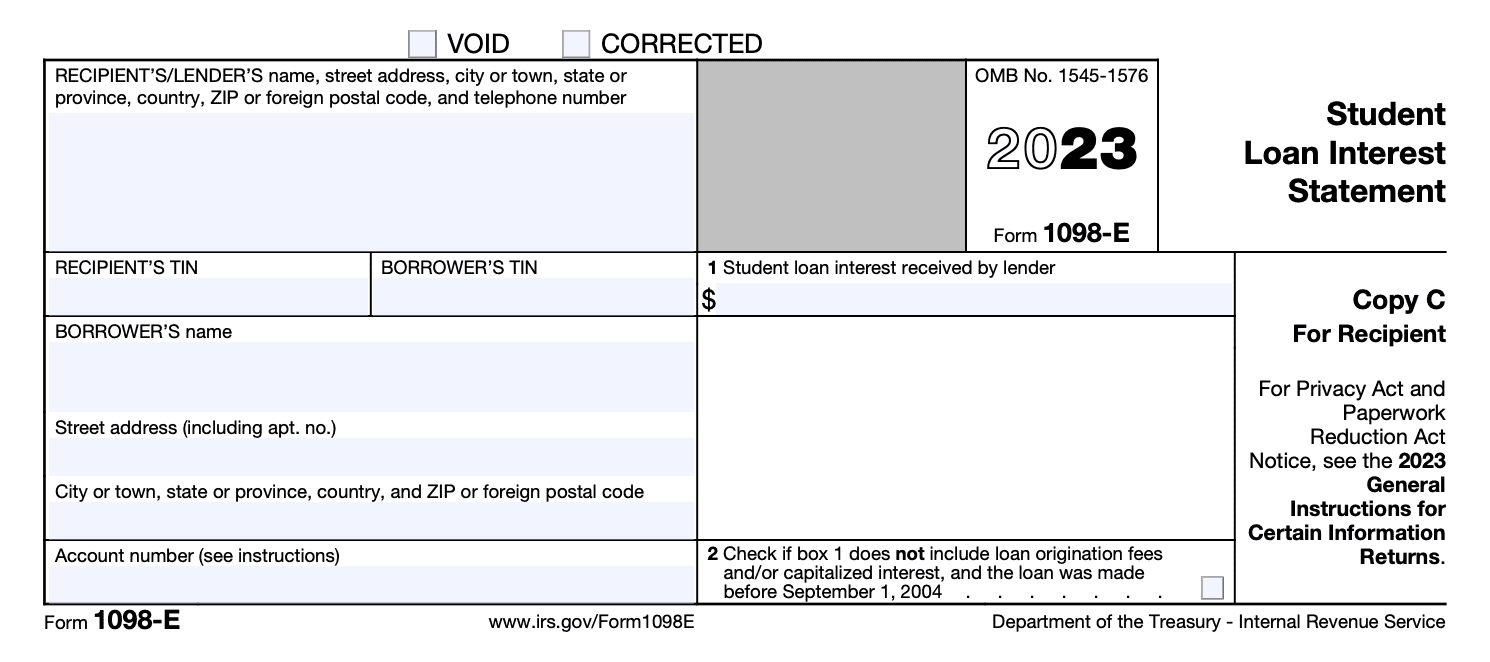

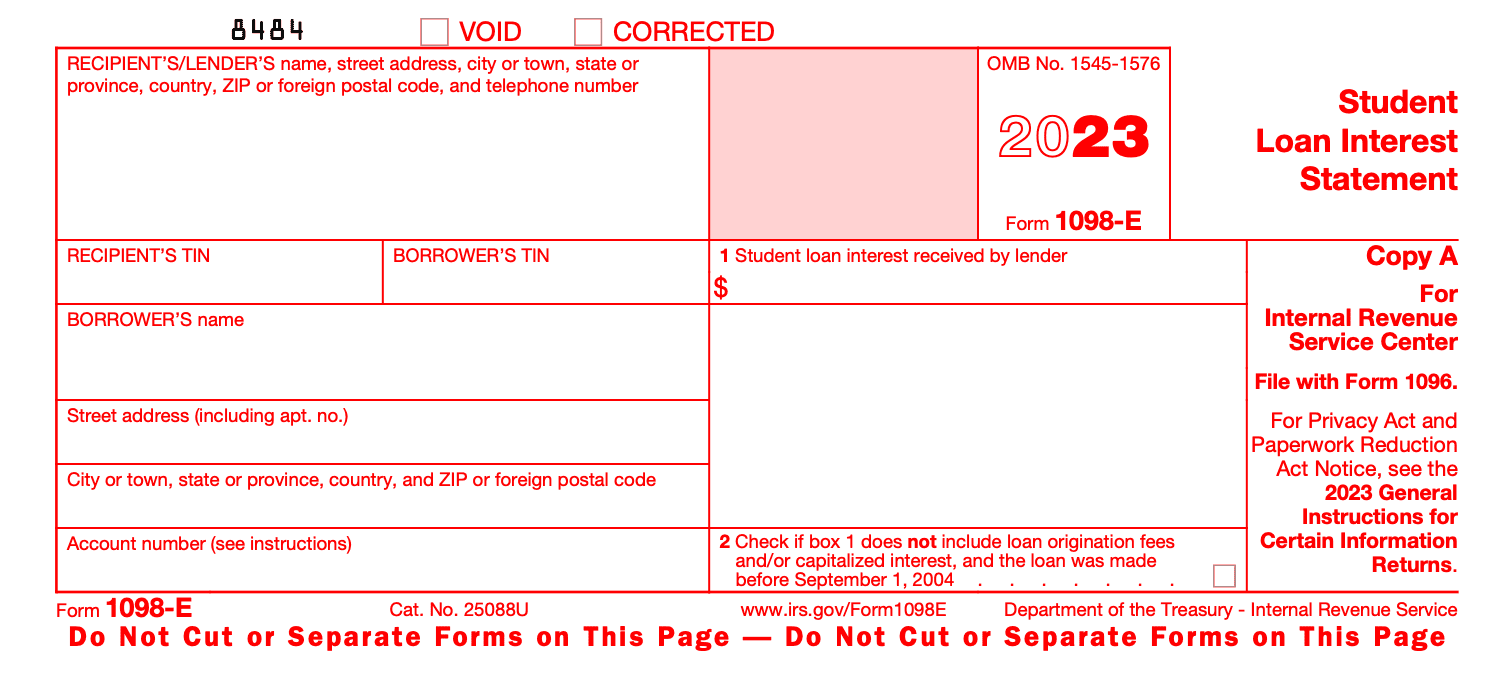

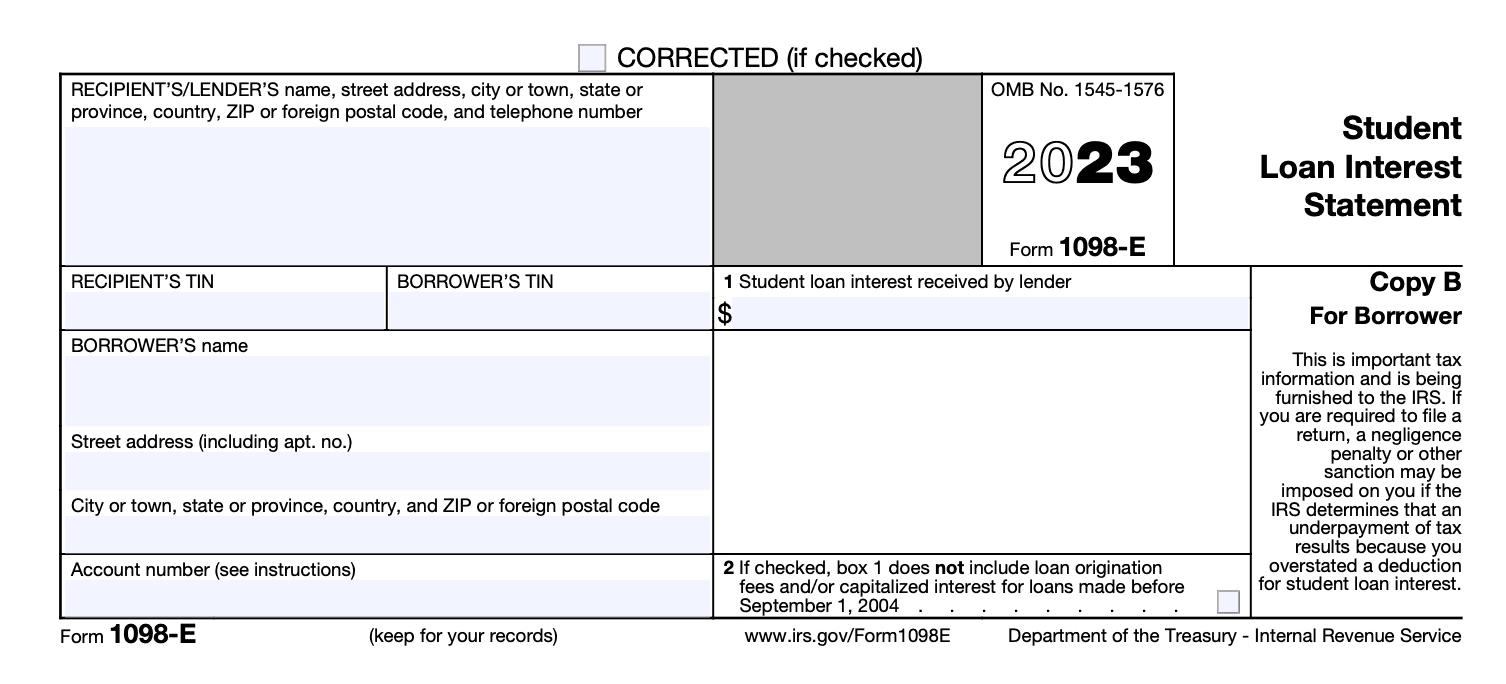

Box 1: Student Loan Interest Received

This is the most critical box on the Form 1098-E. It reports the total amount of student loan interest the borrower paid to the institution or lender during the calendar tax year. This figure is what the borrower can potentially deduct on their tax return. It’s important to understand that this amount only includes interest paid, not any origination fees, late fees, or other charges associated with the loan.

Box 2: Outstanding Principal Balance

While not directly used for calculating the interest deduction, Box 2 may report the outstanding principal balance of the student loan as of the end of the tax year. This can be helpful for the borrower to track their overall loan obligations.

Box 3: Loan Identification

This box may contain a reference number or identifier for the specific student loan to which the reported interest pertains. This is particularly useful for borrowers with multiple student loans, as it helps them match the interest reported on the 1098-E to the correct loan.

Other Information

The form may also contain additional information, such as the name and telephone number of a contact person at the institution or lender who can answer questions about the form. It will also have spaces for the payer to provide their identifying information and the recipient’s identifying information.

Eligibility for the Student Loan Interest Deduction

The student loan interest deduction allows eligible taxpayers to reduce their taxable income by the amount of student loan interest they paid during the year, up to a maximum amount. Not all student loans qualify for this deduction, and there are income limitations that can affect the amount of deduction you can claim.

Qualified Student Loans

To be eligible for the deduction, the loan must be a “qualified student loan.” This generally includes loans taken out to pay for qualified higher education expenses for an eligible student. Qualified expenses typically include tuition, fees, books, supplies, and equipment required for enrollment or attendance. The loan must also have been taken out solely for the purpose of paying these qualified expenses.

- Federal Student Loans: Loans made by the federal government, such as Direct Loans, PLUS Loans, and Perkins Loans, are generally qualified student loans.

- Private Student Loans: Loans made by private lenders, such as banks and credit unions, can also be qualified student loans, provided they meet the criteria for being used for qualified higher education expenses.

Loans that do not typically qualify include:

- Loans from relatives or friends.

- Loans from retirement plans.

- Loans from a life insurance policy.

- Loans obtained through a grant or scholarship.

- Loans for which the repayment is contingent on the student’s future service.

Income Limitations

The ability to deduct student loan interest is subject to income limitations. The IRS sets annual limits for Modified Adjusted Gross Income (MAGI). If your MAGI is above these limits, your deduction may be reduced or eliminated entirely. For example, for the 2023 tax year, the deduction begins to phase out for taxpayers with a MAGI above $75,000 (or $150,000 for those married filing jointly) and is eliminated for those with a MAGI of $90,000 or more ($180,000 or more for those married filing jointly).

Claiming the Student Loan Interest Deduction on Your Tax Return

When you receive a Form 1098-E, it simplifies the process of claiming the student loan interest deduction on your federal income tax return.

Where to Report

The student loan interest deduction is an “above-the-line” deduction, meaning you can claim it even if you do not itemize your deductions. It is reported on Schedule 1 (Form 1040), Additional Income and Adjustments to Income, line 20.

Calculating the Deduction

The maximum amount of student loan interest you can deduct in a tax year is $2,500. If the amount of interest reported on your 1098-E is less than $2,500, you can deduct the actual amount you paid. If you paid more than $2,500, you can only deduct up to the $2,500 limit. Remember to consider the MAGI limitations, which may reduce your deductible amount.

Keeping Records

It is always a good practice to keep your Form 1098-E along with your tax return and other supporting documentation. This can be helpful in case of an audit or if you need to refer back to the information in future tax years.

Common Questions and Considerations Regarding Form 1098-E

While the Form 1098-E is designed for clarity, some questions and scenarios may arise for taxpayers.

What if I don’t receive a 1098-E?

If you paid student loan interest during the tax year and did not receive a Form 1098-E by the January 31st deadline (for paper statements), you should contact the lender or educational institution that received your interest payments. They are required to send you a 1098-E if you paid more than $600 in interest. You can still claim the deduction if you have records of your interest payments, such as monthly statements or canceled checks, even if you don’t have the official form.

Can I deduct interest paid by my parents?

If your parents paid the interest on your student loan, and they are claiming you as a dependent, they may be able to deduct the interest on their tax return. However, if you are not claimed as a dependent by your parents, and they paid the interest on a loan for which you are responsible, the deduction generally belongs to the borrower (you) if you are otherwise eligible. It is crucial to understand who legally made the interest payments and whose tax return is being filed.

What about refinancing my student loans?

If you refinance your student loans, the new lender will be responsible for issuing a Form 1098-E for the interest paid on the refinanced loan in that tax year. Any interest paid on the old loan before the refinancing should be reported on a 1098-E from the original lender, if applicable.

Does the 1098-E report interest on private loans only?

No, the Form 1098-E can be issued for both federal and private student loans. The key factor is that qualified student loan interest has been paid, and the payer has met the reporting threshold.

What is the difference between a 1098-T and a 1098-E?

It’s important not to confuse Form 1098-E with Form 1098-T, Tuition Statement. Form 1098-T reports the amounts billed and paid for qualified tuition and related expenses, which are used to determine eligibility for education credits (like the American Opportunity Tax Credit and the Lifetime Learning Credit). Form 1098-E, on the other hand, specifically reports student loan interest paid. Both forms are important for tax purposes related to higher education but serve different functions.

In conclusion, Form 1098-E is an indispensable document for taxpayers seeking to reduce their tax burden by deducting student loan interest. By understanding its purpose, contents, and the eligibility requirements for the deduction, students and their families can effectively leverage this tax benefit, making the pursuit of higher education more financially manageable. Always consult with a qualified tax professional if you have complex tax situations or specific questions about student loan interest deductions.