The cessation of life brings an end to many earthly concerns, but for those left behind, financial obligations can linger. Understanding the fate of a deceased individual’s debts is crucial for executors, beneficiaries, and even creditors. This complex process involves a hierarchy of payments, legal frameworks, and the careful administration of an estate. The primary consideration is always the deceased’s assets and how they will be utilized to settle outstanding liabilities before any remaining wealth is distributed to heirs.

The Executor’s Role: Navigating the Financial Aftermath

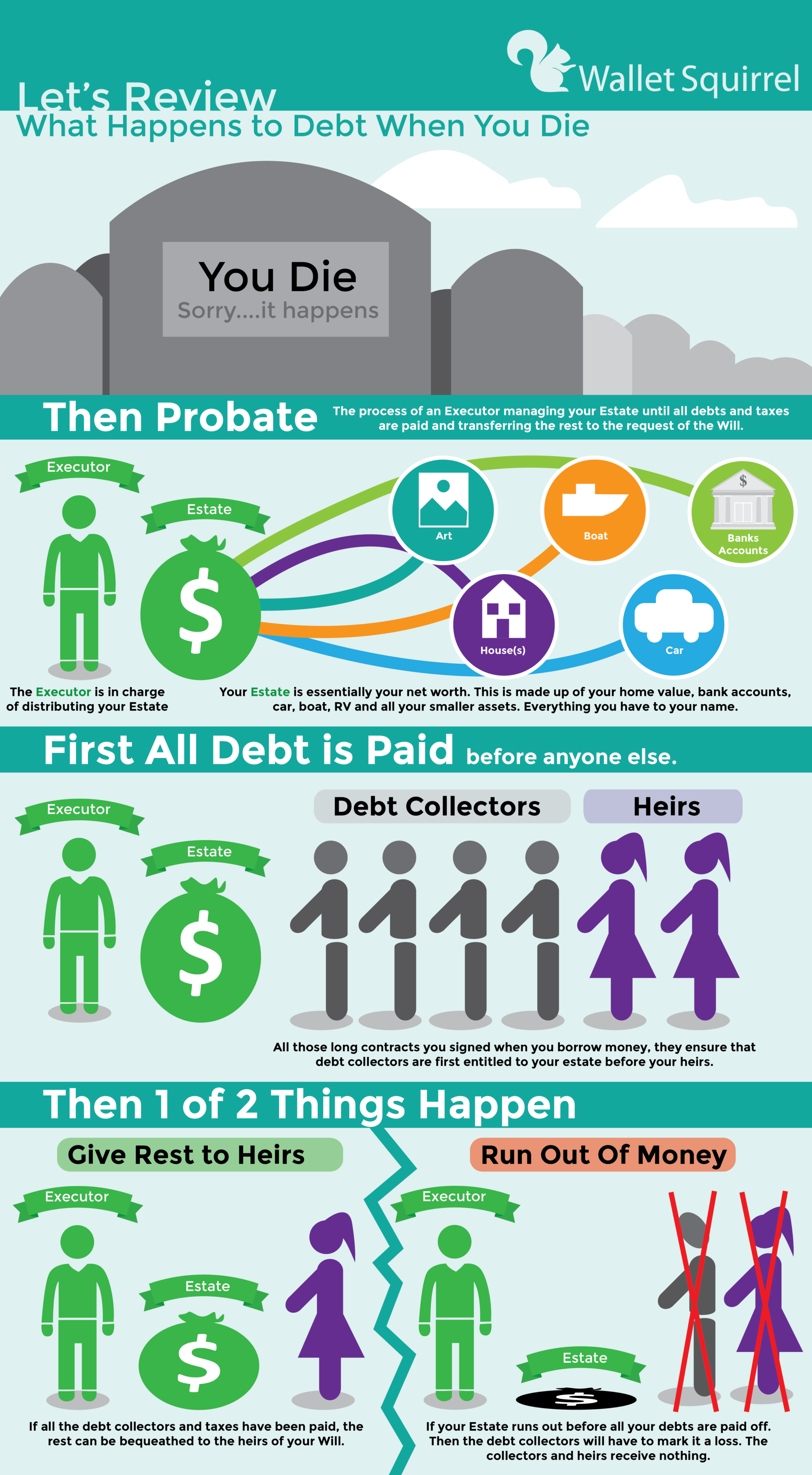

Upon an individual’s death, the responsibility for managing their financial affairs typically falls to an executor, named in the will, or a court-appointed administrator if no will exists. This individual, often a close family member or friend, steps into a position of considerable legal and financial authority. Their first and most critical task is to identify all of the deceased’s assets and liabilities. This involves a thorough search through financial records, property deeds, bank statements, and any other documents that could indicate financial holdings or obligations.

Identifying and Valuing Assets

The executor must meticulously catalog every asset belonging to the deceased. This can range from tangible possessions like real estate, vehicles, and personal belongings, to intangible assets such as bank accounts, investment portfolios, retirement funds, and life insurance policies. The value of these assets must be accurately determined, often through professional appraisals for real estate and valuable personal property, or by consulting financial statements for liquid assets. This valuation is essential for establishing the total worth of the estate, which will dictate the capacity to repay debts.

Notifying Creditors

Once the assets are identified and valued, the executor must formally notify known creditors of the death. This is typically done through official letters, often accompanied by a copy of the death certificate. State laws dictate the specific procedures for notification, including the timeframe within which creditors must file their claims against the estate. This proactive communication ensures that all parties are aware of the situation and have the opportunity to present their claims. Unidentified creditors may also become aware through public notices, such as obituaries or legal advertisements, that the executor is required to publish in local newspapers.

The Probate Process

In many cases, the administration of a deceased person’s estate will go through a legal process called probate. Probate is overseen by a court and serves to validate the will, appoint an executor or administrator, identify and appraise assets, pay debts and taxes, and finally, distribute the remaining assets to the rightful heirs. The duration and complexity of probate can vary significantly depending on the size and nature of the estate, as well as the laws of the specific jurisdiction. During probate, the executor operates under the court’s supervision, ensuring that all legal requirements are met.

Debt Settlement: A Hierarchical Approach

The order in which debts are paid is not arbitrary. State laws establish a specific hierarchy that dictates which creditors have priority. This ensures that certain obligations are met before others, providing a structured framework for debt resolution.

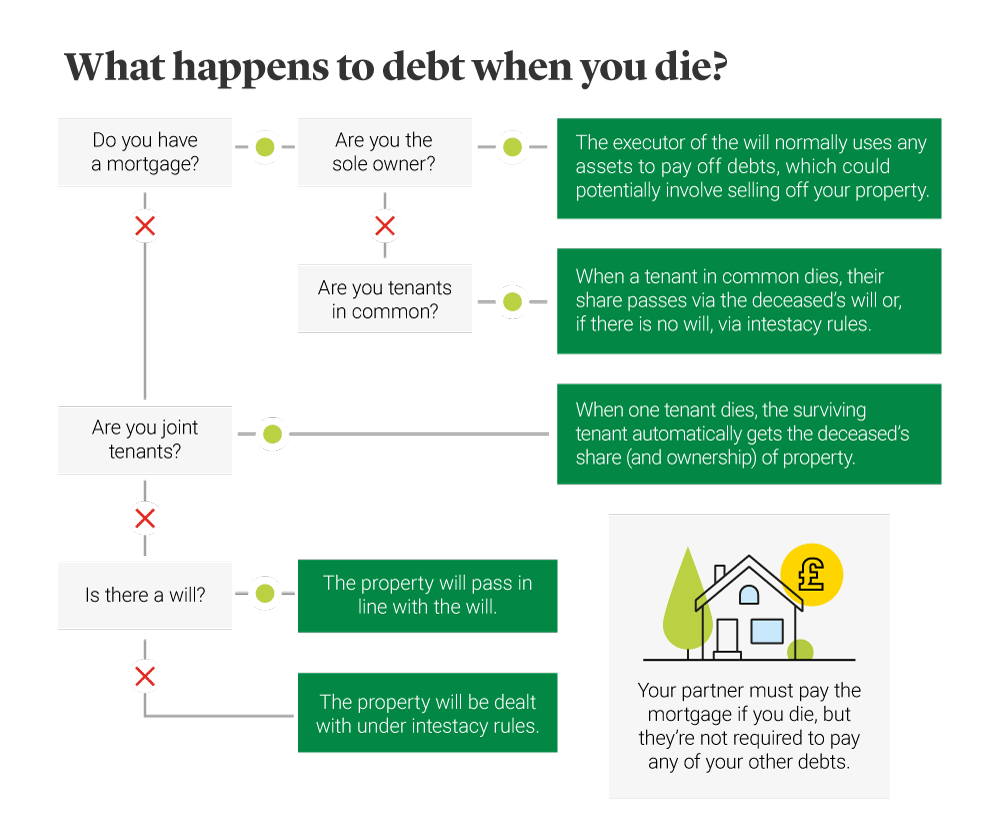

Secured Debts: The First in Line

Secured debts are those backed by collateral, meaning the creditor has a legal claim on a specific asset if the debt is not repaid. Mortgages on a home, car loans, and loans secured by other valuable property fall into this category. If the deceased owned a home with an outstanding mortgage, the executor has a few options. They can continue to make payments from the estate’s assets to keep the home, sell the home to pay off the mortgage and distribute any remaining equity, or allow the lender to foreclose if the estate lacks sufficient funds or if it’s deemed the best course of action. The same principles apply to other secured debts like car loans.

Priority Debts: Essential Obligations

Following secured debts, there are certain priority debts that must be settled before unsecured debts. These typically include:

- Taxes: Federal, state, and local taxes owed by the deceased, including income tax and estate tax (if applicable), have a high priority.

- Funeral Expenses: Reasonable costs associated with the funeral and burial are generally paid from the estate.

- Probate Costs: Legal fees, court costs, and executor fees associated with the probate process itself are also prioritized.

- Spousal and Child Support: Arrears in spousal or child support payments often take precedence.

The specific order of these priority debts can vary by state, but they are consistently ranked above general unsecured debts.

Unsecured Debts: The Remainder

Unsecured debts are those not backed by any collateral. This category includes:

- Credit Card Debt: Balances on credit cards are a common form of unsecured debt.

- Medical Bills: Outstanding medical expenses for the deceased’s care.

- Personal Loans: Unsecured loans taken out from banks or other lenders.

- Student Loans: While some student loans may have provisions for discharge upon death, many do not, and remain an obligation of the estate.

If the estate’s assets are insufficient to cover all debts, unsecured creditors will receive payment on a pro-rata basis. This means they will receive a percentage of what they are owed, based on the remaining funds after secured and priority debts have been settled.

When Assets Aren’t Enough: Insolvency and Beyond

A significant concern for both executors and heirs is the possibility that the deceased’s debts exceed their assets. This situation is known as estate insolvency.

The Role of the Estate as a Separate Entity

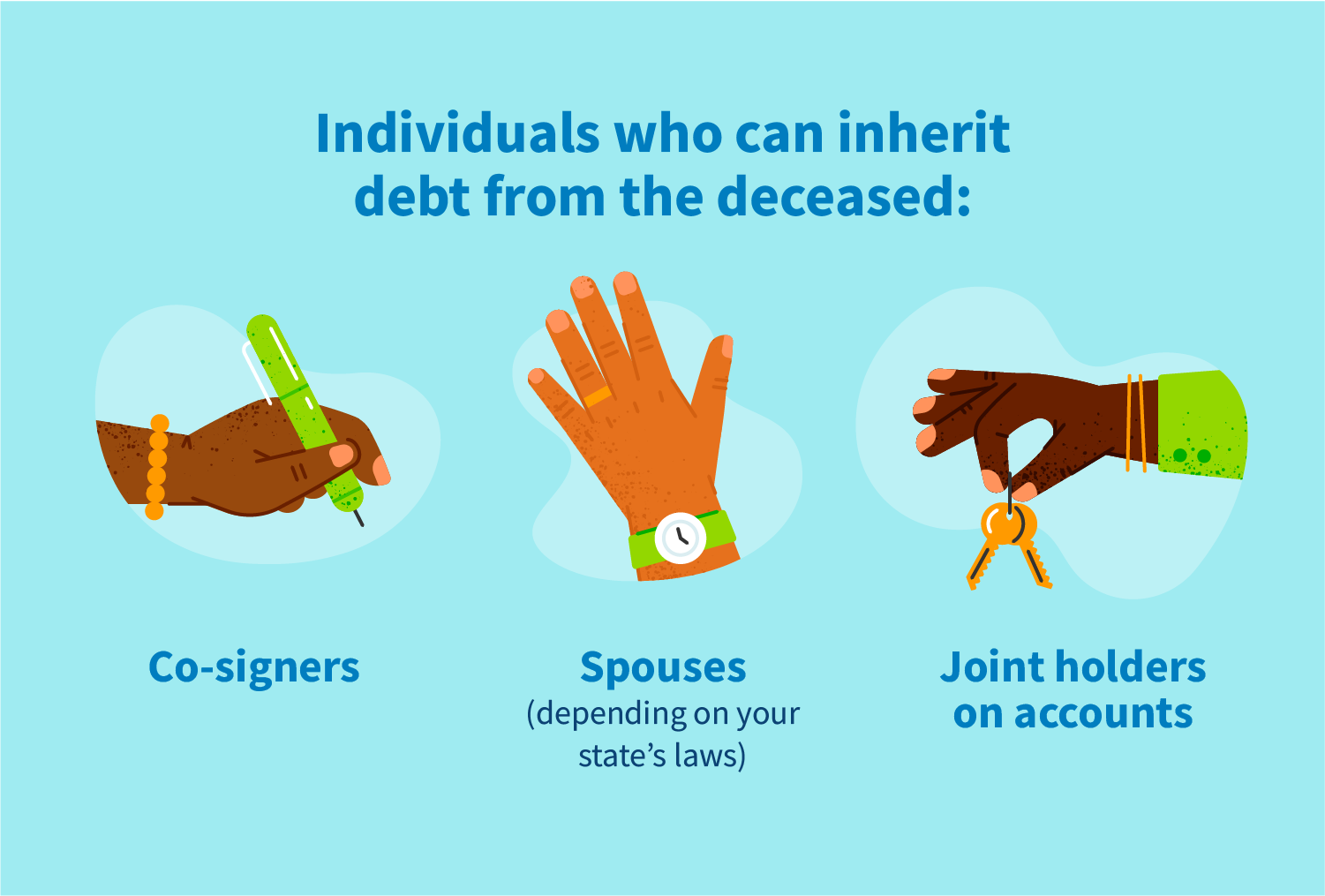

It’s a common misconception that debts transfer directly to the surviving family members. In most cases, this is not true. The estate is treated as a separate legal entity, and its debts are paid from its assets. Surviving spouses, children, or other relatives are generally not personally liable for the deceased’s debts, unless they were a co-signer on a loan or have jointly owned accounts where they assume responsibility.

What Happens to Unpaid Debts?

If an estate is insolvent, meaning there are not enough assets to pay all creditors in full, the hierarchy of debt settlement still applies. Secured creditors will still have a claim on their collateral. Priority debts will be paid as much as possible. Unsecured creditors will receive whatever remains, which may be very little or nothing at all. Once the estate’s assets are exhausted and all possible payments have been made according to the legal hierarchy, any remaining unpaid debts are typically discharged. The creditors are then unable to pursue these debts further.

Joint Debts and Co-Signers

There are exceptions where family members might be responsible for a deceased person’s debt. The most common scenario is when a surviving individual was a co-signer on a loan or credit card. In such cases, the co-signer remains fully responsible for the entire debt, even after the primary borrower’s death. Similarly, if a spouse had joint credit card accounts, the surviving spouse is typically responsible for the entire balance. Community property laws in some states can also create complexities, potentially making spouses jointly liable for debts incurred during the marriage, regardless of whose name is on the account.

Specific Debt Types and Their Fate

Different types of debt have distinct rules regarding their treatment after death.

Mortgages and Home Equity

As mentioned, mortgages are secured debts. If the deceased owned a home, the mortgage lender has a claim on the property. The executor must decide whether to sell the property to pay off the mortgage, continue making payments from the estate, or let the lender foreclose. Home equity lines of credit (HELOCs) are also typically secured by the property and are treated similarly.

Car Loans

Similar to mortgages, car loans are secured by the vehicle. The executor can choose to pay off the loan from the estate, continue payments if a beneficiary wishes to keep the car, or allow the lender to repossess the vehicle.

Credit Card Debt

Credit card debt is unsecured. It will be paid from the estate’s assets after secured and priority debts. If funds are insufficient, the remaining balance is usually discharged. However, it’s crucial for the executor to ensure all claims are properly handled and that no fraudulent claims are honored.

Student Loans

The treatment of student loans upon death can vary. Federal student loans often have provisions for discharge if the borrower dies. The executor would need to provide a death certificate to the loan servicer to initiate this process. Private student loans, however, may have different terms. Some may be dischargeable, while others might become an obligation of the estate or even a co-signer if one exists.

Medical Debt

Medical debt is generally considered unsecured. It will be paid from the estate according to the established hierarchy. If the deceased was covered by insurance, the executor should ensure all claims were submitted and paid by the insurer before treating the remaining balance as a debt of the estate.

Protecting Heirs and the Estate

Navigating the financial aftermath of a death requires careful planning and adherence to legal procedures to protect both the estate and the rightful heirs.

The Importance of a Will

A well-drafted will is invaluable. It clearly outlines the deceased’s wishes regarding asset distribution and can name an executor trusted to manage the process. This foresight can significantly reduce confusion and potential disputes among beneficiaries.

Life Insurance and Payable-on-Death Accounts

Assets like life insurance policies with designated beneficiaries and accounts with “Payable-on-Death” (POD) or “Transfer-on-Death” (TOD) designations generally bypass the probate process. These assets are transferred directly to the named beneficiary, regardless of the will’s contents or the estate’s debts. This can be a valuable way to provide immediate liquidity to heirs or to cover specific expenses like funeral costs. However, in some limited circumstances and jurisdictions, life insurance proceeds might be subject to estate taxes or even claims by creditors if the estate is insolvent, although this is less common.

Seeking Professional Guidance

The complexities of estate administration and debt settlement often necessitate professional help. Executors are strongly advised to consult with an estate attorney and a tax advisor. An attorney can guide the executor through the probate process, ensure legal compliance, and help manage creditor claims. A tax advisor can assist with filing final tax returns and navigating any estate tax obligations. This professional support is crucial for making informed decisions and preventing costly mistakes that could impact the estate or its beneficiaries.