Reinsurance, in its essence, is insurance for insurance companies. It’s a critical, albeit often unseen, component of the global financial system that allows insurers to manage risk, maintain solvency, and underwrite more complex or extensive policies. For the average consumer, the concept of reinsurance might seem distant, but its impact is far-reaching, ultimately contributing to the stability and availability of insurance products across various sectors, including those that rely heavily on technology and innovation.

This article will delve into the fundamental concept of reinsurance, exploring its purpose, various forms, and the crucial role it plays in underpinning the insurance industry. We will then examine how this risk management tool is particularly relevant and impactful within the burgeoning fields of cutting-edge technology, especially those connected to advanced imaging and flight systems.

The Fundamentals of Reinsurance: A Risk Management Pillar

At its core, reinsurance is a contract whereby one insurance company (the “cedent” or “ceding company”) transfers a portion of its own risks to another insurance company (the “reinsurer”). This transfer is not a sale of policies to the public but rather a wholesale transaction between two financial institutions. The primary insurer, by ceding risk, is essentially buying protection for itself against the potential for large losses that could either cripple its financial stability or exceed its capacity to pay claims.

Why Do Insurers Reinsure?

The motivations for an insurance company to seek reinsurance are multifaceted and deeply rooted in sound financial practice and risk management.

Managing Capacity and Large Risks

One of the primary drivers for reinsurance is the management of underwriting capacity. An insurance company has a finite amount of capital it can risk on any given policy or a portfolio of policies. For instance, a property and casualty insurer might be able to underwrite a certain number of home insurance policies or provide coverage for a specific value of commercial property. However, a single catastrophic event, like a major earthquake or a widespread hurricane, could generate claims that far exceed the insurer’s financial reserves. Reinsurance allows the insurer to “lay off” a portion of this extreme risk, thereby increasing its capacity to underwrite larger or more numerous policies without jeopardizing its solvency.

Stabilizing Financial Results

The insurance industry is inherently exposed to volatility. Unexpectedly high claim frequencies or severities can lead to significant swings in an insurer’s profitability. Reinsurance acts as a buffer, smoothing out these fluctuations. By transferring a portion of its potential losses, the ceding company can achieve more predictable financial results, which is attractive to investors, regulators, and rating agencies. This stability is crucial for long-term business planning and for maintaining the confidence of policyholders.

Catastrophe Protection

Catastrophic events, by their nature, are rare but can be extremely costly. Insurers often purchase “catastrophe excess of loss” reinsurance. This type of coverage protects them against losses exceeding a predetermined threshold from a single event or a series of related events. For example, an insurer might buy protection against losses exceeding $50 million from a hurricane. If a hurricane causes $200 million in claims, the reinsurer would cover the amount above $50 million, significantly mitigating the primary insurer’s exposure.

Entering New Markets or Underwriting New Risks

Launching new products or expanding into unfamiliar territories often involves inherent uncertainties. Reinsurance can provide the necessary support for an insurer to gain experience and build its portfolio in these new areas. By sharing the initial risk, the insurer can test the market and refine its pricing and underwriting strategies with a safety net in place. This is particularly relevant in fast-evolving sectors where novel risks are constantly emerging.

The Mechanics of Reinsurance

Reinsurance contracts, often referred to as “treaties,” can be structured in various ways, each offering different levels of risk transfer and premium payment.

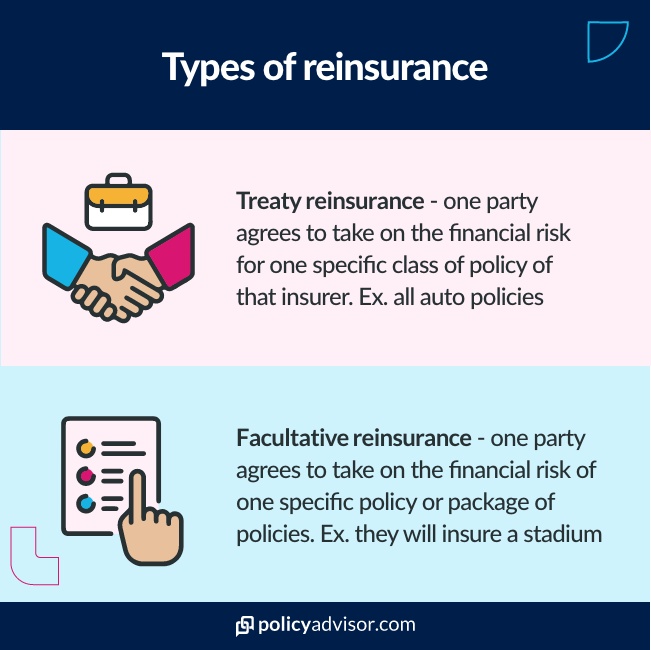

Treaty Reinsurance

In treaty reinsurance, the reinsurer agrees to accept a defined portion of a specific class or classes of business written by the ceding company over a set period. This provides automatic coverage for all policies that fall within the scope of the treaty. Treaties can be further categorized:

-

Proportional Reinsurance: In this type, the reinsurer shares a proportional part of both the premiums and the losses of the ceding company. This can be structured as:

- Quota Share: The reinsurer assumes a fixed percentage of every risk written by the ceding company. For example, a 20% quota share treaty means the reinsurer receives 20% of the premiums and pays 20% of the claims for the covered business.

- Surplus Share: This is used when the ceding company wants to retain more of the smaller risks and only reinsure the larger ones. The reinsurer agrees to accept a portion of the risk that exceeds the ceding company’s retention limit, up to a specified amount.

-

Non-Proportional Reinsurance (Excess of Loss): Here, the reinsurer only pays if the losses exceed a certain predetermined amount (the “retention” or “deductible”) for the ceding company. The reinsurer is not involved in sharing the premiums proportionally but collects a premium for the coverage provided. Common forms include:

- Per Risk XL: The reinsurer pays losses on individual risks that exceed a specified limit.

- Per Occurrence XL: The reinsurer pays losses from a single event or occurrence that exceed a specified aggregate limit for that event.

- Aggregate XL: The reinsurer pays losses once the ceding company’s total losses for a defined period (usually a year) exceed a specific aggregate amount.

Facultative Reinsurance

Unlike treaty reinsurance, facultative reinsurance is negotiated on a case-by-case basis for individual risks. The ceding company offers a specific risk to a reinsurer, who then decides whether to accept it and on what terms. This is typically used for large or unusual risks that do not fit within the parameters of existing treaties.

The Role of Reinsurance in Technological Advancement

The rapid pace of technological innovation, particularly in areas like advanced imaging, autonomous systems, and drone technology, presents both opportunities and significant new risks for insurers. Reinsurance plays a pivotal role in enabling the insurance industry to confidently underwrite these emerging technologies.

Underwriting Emerging Technologies: A New Frontier for Risk

The development of sophisticated technologies such as high-resolution gimbal cameras, advanced stabilization systems, AI-driven flight modes, and complex sensor arrays introduces novel and evolving risks. Insurers need to understand and price these risks accurately.

Flight Technology and Autonomous Systems

The proliferation of drones, from small consumer quadcopters to sophisticated industrial UAVs, necessitates specialized insurance coverage. These policies must account for risks such as:

- Operational Failures: Malfunctions in navigation, stabilization systems, GPS, or obstacle avoidance sensors can lead to crashes and property damage.

- Cybersecurity Threats: Drones are increasingly connected, making them vulnerable to hacking, which could result in loss of control or data breaches.

- Product Liability: Manufacturers of flight technology, sensors, and control systems face potential liability if their products are found to be defective and cause harm.

- Third-Party Liability: Damage to property or injury to individuals caused by drone operations is a significant concern.

Reinsurers provide capacity and expertise that allow primary insurers to underwrite these complex risks. They can help analyze the probability of system failures, the impact of environmental factors on flight, and the evolving legal and regulatory landscape surrounding drone operations.

Cameras and Imaging Systems

Similarly, the advancement in cameras and imaging technology, including 4K and higher resolution, thermal imaging, and sophisticated optical zoom capabilities, brings its own set of insurance considerations.

- Equipment Damage: High-value imaging equipment is susceptible to damage during operation, transport, or storage.

- Data Loss or Corruption: The valuable data captured by these advanced cameras can be lost due to equipment failure, human error, or cyberattacks.

- Intellectual Property Risks: Issues related to the use of captured imagery and potential copyright infringements can arise.

- Specialized Liability: In certain applications, such as aerial inspections or surveillance, the accuracy and reliability of imaging data can have significant legal implications.

Reinsurance helps insurers cover the potential costs associated with insuring this high-value and often critical equipment, as well as the liabilities that may arise from its use.

Facilitating Innovation Through Risk Mitigation

Without the risk-sharing mechanisms provided by reinsurance, primary insurers might be hesitant to offer comprehensive coverage for cutting-edge technologies. This could stifle innovation by making it prohibitively expensive or impossible for companies developing these products to obtain the necessary insurance to operate and scale.

- Enabling Larger Projects: For large-scale drone deployment in sectors like agriculture, infrastructure inspection, or delivery services, significant underwriting capacity is required. Reinsurance allows insurers to participate in these large projects by transferring a portion of the risk.

- Supporting Start-ups: New ventures in the drone and imaging technology space often have limited capital. Reinsurance can indirectly support them by enabling insurers to offer them the coverage they need at more competitive rates.

- Promoting Research and Development: The availability of insurance backed by reinsurers provides a safety net for companies investing heavily in R&D for new flight technologies, stabilization systems, and advanced imaging.

In essence, reinsurance acts as a crucial enabler, allowing the insurance market to keep pace with the rapid evolution of technology. It provides the financial backbone that allows for the underwriting of novel risks, thereby fostering an environment where innovation can flourish.

Types of Reinsurance and Their Application to Tech Sectors

The specific needs of tech-related industries, with their unique risk profiles, often necessitate tailored reinsurance solutions. Understanding the different types of reinsurance is key to appreciating how these solutions are applied.

Treaty Reinsurance in the Tech Industry

Treaty reinsurance is particularly beneficial for insurers who underwrite large volumes of similar risks within the tech sector.

- Proportional Treaties for Drone Manufacturers: An insurer providing product liability coverage to a high-volume drone manufacturer might enter into a quota share treaty. This means the reinsurer shares a percentage of the premiums and claims for every drone sold. This helps the primary insurer manage its exposure to widespread product defects and product recalls.

- Surplus Share for High-Value Imaging Equipment: For insurers covering expensive gimbal cameras and other specialized imaging gear, a surplus share treaty can be effective. If a policyholder insures a $50,000 camera, and the primary insurer’s retention limit is $10,000, the reinsurer would automatically cover a portion of the risk exceeding $10,000, up to an agreed-upon limit. This allows insurers to offer high-value coverage without taking on an undue burden for each individual policy.

Non-Proportional Reinsurance for Catastrophic Tech-Related Events

Non-proportional reinsurance, especially excess of loss, is vital for protecting against large, infrequent events that could impact the tech industry.

- Per Occurrence XL for Drone Fleets: A company operating a large fleet of commercial drones might face a scenario where a single software glitch or a coordinated cyberattack causes multiple drones to crash simultaneously. A per occurrence excess of loss treaty would protect the insurer against the aggregate losses from such an event exceeding a specific threshold.

- Aggregate XL for Sensor Malfunctions: If a broad series of sensor malfunctions across various drone models, manufactured by the same company, leads to a significant number of individual claims over a policy year, an aggregate excess of loss treaty would come into play once the total claims reach a certain level. This safeguards the insurer from cumulative losses over time.

- Catastrophe Excess of Loss for Natural Disasters Impacting Tech Infrastructure: While not directly related to the technology itself, natural disasters can severely impact data centers, manufacturing facilities, or distribution hubs for tech companies. Insurers providing property coverage to these entities rely on catastrophe excess of loss reinsurance to protect themselves from the massive claims that could arise from events like earthquakes or hurricanes.

Facultative Reinsurance for Novel or Unique Tech Risks

The truly groundbreaking nature of some technological advancements means that standard treaty structures may not adequately cover the risks involved. This is where facultative reinsurance becomes essential.

- Unique AI Flight System: A company developing a highly experimental AI system for autonomous flight that operates outside current regulatory frameworks might require facultative reinsurance. Each specific risk associated with the system’s deployment would be underwritten individually by a reinsurer.

- Cutting-Edge Imaging Sensor Development: The development of a completely new type of imaging sensor with untested capabilities and unknown failure modes would likely be reinsured facultatively. The reinsurer would assess the specific technical risks, potential liabilities, and projected market performance before offering coverage.

- Large-Scale Drone Delivery Networks: The launch of a novel, large-scale drone delivery network in a complex urban environment presents unique operational and liability challenges. Insurers might seek facultative reinsurance for specific aspects of this operation, such as unique flight path risks or potential interactions with air traffic control systems.

The ability for reinsurers to underwrite these bespoke risks on a facultative basis is crucial for pushing the boundaries of what is technologically possible, as it allows for the creation of insurance products that can adapt to the rapidly changing landscape of innovation.

The Future of Reinsurance in a Tech-Driven World

As technology continues to evolve at an exponential rate, the relationship between reinsurance and innovation will only deepen. The challenges and opportunities presented by emerging fields will demand even more sophisticated risk management solutions.

The Impact of Artificial Intelligence and Machine Learning

AI and machine learning are not only driving innovation in the sectors being insured but are also transforming the reinsurance industry itself.

- Enhanced Risk Assessment: Reinsurers are increasingly using AI and machine learning to analyze vast datasets, identify patterns, and more accurately assess the risks associated with new technologies. This allows for more precise pricing and better underwriting decisions.

- Predictive Modeling: Advanced algorithms can predict the likelihood of certain technological failures or the impact of evolving cyber threats, enabling reinsurers to proactively manage their portfolios.

- Automated Underwriting: In some cases, AI can automate aspects of facultative and treaty underwriting, increasing efficiency and speed.

The Rise of Parametric Reinsurance

Parametric insurance, which pays out based on predefined triggers (e.g., wind speed exceeding a certain threshold, seismic activity reaching a specific magnitude) rather than on the actual assessment of losses, is becoming increasingly relevant for technological risks.

- Drone Operation Triggers: A parametric policy for drone operations could be triggered by adverse weather conditions that exceed safe operating limits, automatically compensating the insured for grounded operations or equipment damage due to conditions outside their control.

- Imaging System Performance Triggers: For critical imaging applications, a parametric policy could be triggered if sensor performance degrades below a certain calibrated level, ensuring immediate financial recourse for operational disruptions.

Reinsurance is instrumental in supporting the growth of parametric solutions, as reinsurers have the capacity to underwrite these large-scale trigger-based exposures.

The Symbiotic Relationship: Reinsurance as an Innovation Catalyst

The connection between reinsurance and technological advancement is not merely one of protection; it is a symbiotic relationship where reinsurance actively catalyzes innovation. By absorbing and managing the inherent risks associated with cutting-edge developments, reinsurance allows companies to invest, develop, and deploy new technologies with greater confidence. This, in turn, fuels further innovation, creating a virtuous cycle.

The complex world of drones, advanced flight systems, and sophisticated imaging technology, while exciting, would face significant hurdles in their widespread adoption and development without the robust risk management framework that reinsurance provides. It is the unseen hand that ensures the financial stability of the insurance market, enabling it to confidently underwrite the uncertainties of tomorrow’s technological landscape. As we continue to push the boundaries of what is possible, the role of reinsurance will remain paramount, a silent but indispensable partner in the journey of technological progress.