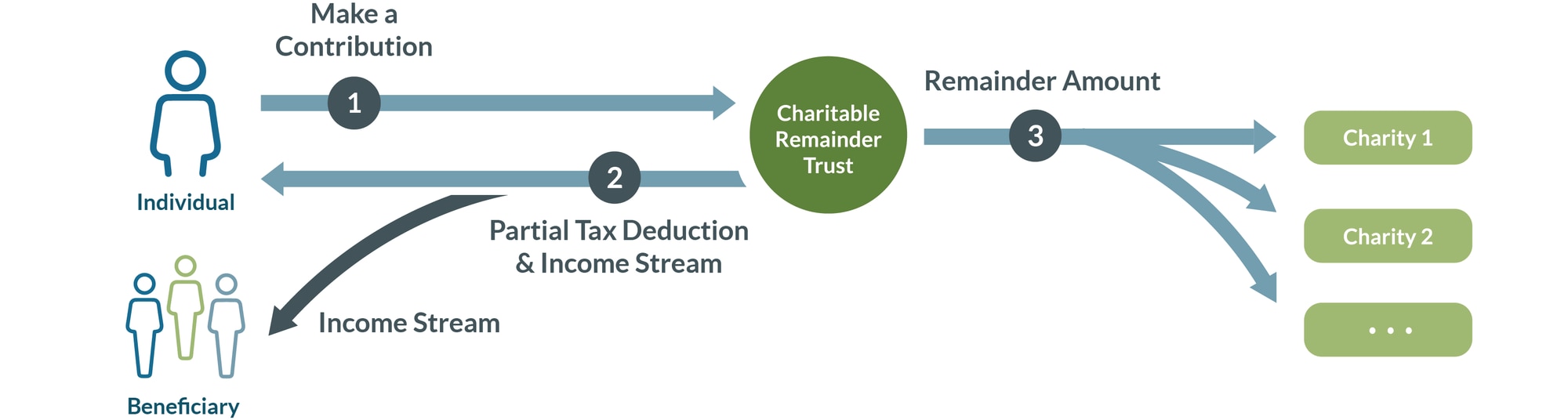

In the landscape of modern financial planning and philanthropy, where strategies for wealth management intersect with profound charitable intent, the Charitable Remainder Trust (CRT) stands out as a sophisticated and highly effective instrument. Far from a simple donation, a CRT is an irrevocable trust designed to provide a stream of income to one or more non-charitable beneficiaries (often the donor or their heirs) for a specified term, after which the remaining assets are donated to a qualified charity. This innovative structure offers significant tax advantages to the donor while ensuring a substantial future gift to a chosen cause, representing a powerful blend of financial foresight and altruism.

Understanding the Core Mechanics of a Charitable Remainder Trust

At its heart, a CRT is a contract with multiple beneficiaries and a structured timeline. When a donor establishes a CRT, they transfer assets—which can include cash, securities, real estate, or other appreciated property—into the trust. These assets are then typically invested to generate income.

The Donor’s Perspective: Income and Tax Benefits

For the donor, a CRT offers several compelling benefits that make it a cornerstone of advanced financial and estate planning:

- Income Stream: The primary allure for many donors is the creation of a reliable income stream. Depending on the trust’s structure (which we’ll explore shortly), the donor or other non-charitable beneficiaries receive regular payments for a specified period, which can be a fixed number of years (up to 20) or the lifetime of the beneficiaries. This provides financial security, especially for those looking to supplement retirement income or support family members.

- Immediate Income Tax Deduction: Upon funding the CRT, the donor is eligible for an immediate income tax deduction. The amount of this deduction is calculated based on the present value of the future charitable gift, considering factors such as the income payout rate, the term of the trust, and prevailing interest rates. This upfront tax benefit can significantly reduce a donor’s current taxable income, making philanthropy even more appealing.

- Avoidance of Capital Gains Tax: One of the most significant advantages of a CRT, particularly when funded with highly appreciated assets like stocks or real estate, is the avoidance of immediate capital gains tax. When a donor contributes appreciated assets to a CRT, they do not pay capital gains tax at the time of the transfer. Instead, the trust can sell these assets tax-free, reinvest the full proceeds, and generate a larger income stream for the beneficiaries than if the assets had been sold personally, taxed, and then reinvested. This tax deferral and avoidance on the initial sale allows for greater wealth preservation and growth within the trust.

- Estate Tax Reduction: Assets transferred into a CRT are removed from the donor’s taxable estate, thereby reducing potential estate taxes. The remainder interest designated for charity is also excluded from estate tax calculations, further enhancing the trust’s appeal as an estate planning tool.

The Charitable Beneficiary’s Future

While donors enjoy immediate and ongoing financial benefits, the essence of a CRT lies in its ultimate purpose: benefiting a chosen charity. Once the non-charitable income period ends, the remaining assets in the trust are distributed to the designated charitable organization(s). This future gift ensures long-term support for causes important to the donor, reflecting a lasting legacy of generosity. Charities, in turn, appreciate CRTs as a source of planned giving that provides substantial funding for their missions in the future.

Types of Charitable Remainder Trusts

There are two primary forms of Charitable Remainder Trusts, each with distinct characteristics regarding how income payments are calculated:

Charitable Remainder Annuity Trust (CRAT)

A CRAT pays a fixed annuity amount each year to the non-charitable beneficiaries. This payment is determined when the trust is established and remains constant throughout the trust’s term, regardless of the trust’s investment performance. The annuity amount must be at least 5% but no more than 50% of the initial fair market value of the assets placed into the trust.

- Predictable Income: Donors who prioritize a stable, predictable income stream often favor CRATs. This certainty can be invaluable for budgeting and financial planning, especially during retirement.

- Risk Aversion: Because the payments are fixed, CRATs offer a degree of protection against market downturns affecting the trust’s principal. However, if the trust’s investments perform exceptionally well, the donor does not benefit from increased payments, and the charitable remainder grows more rapidly.

- No Further Contributions: A key characteristic of CRATs is that no additional contributions can be made to the trust after its initial funding.

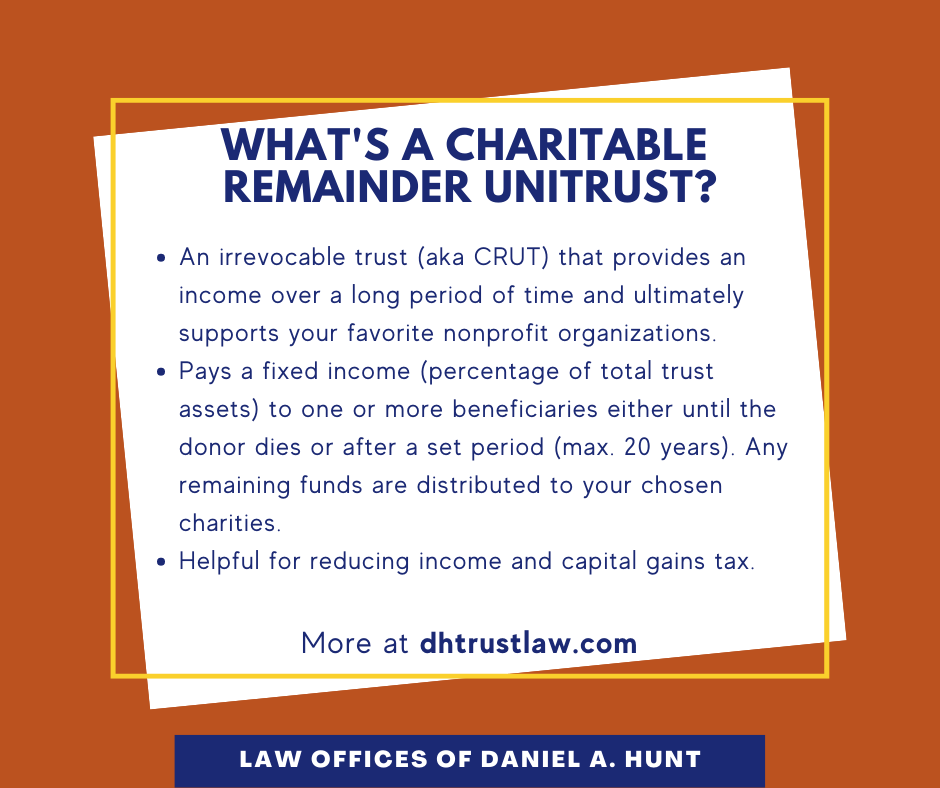

Charitable Remainder Unitrust (CRUT)

A CRUT pays a variable income amount to the non-charitable beneficiaries each year. This payment is calculated as a fixed percentage (at least 5% but no more than 50%) of the trust’s fair market value, revalued annually.

- Variable Income: Unlike CRATs, CRUT payments fluctuate with the annual valuation of the trust assets. If the trust’s investments grow, the payout amount increases; if they decline, the payout decreases. This offers beneficiaries the potential for rising income in a strong market.

- Inflation Hedge: For donors concerned about inflation eroding the purchasing power of their income over time, a CRUT can act as a partial hedge, as payments may grow with the trust’s asset value.

- Additional Contributions: A significant advantage of CRUTs is their flexibility to accept additional contributions over time, allowing donors to add more assets to the trust as their financial circumstances evolve.

- Variations of CRUTs: There are specialized forms of CRUTs, such as:

- Net Income CRUT (NICRUT): Pays the lesser of the fixed percentage or the actual net income of the trust. If the trust’s income is less than the payout percentage, only the net income is distributed.

- Net Income with Makeup CRUT (NIMCRUT): Similar to a NICRUT, but includes a “makeup” provision. If the trust’s income in a given year is less than the stated percentage, the shortfall is tracked and can be paid out in future years when the trust’s income exceeds the stated percentage. These are often used when the trust holds non-income-producing assets that are expected to grow significantly, like undeveloped real estate or early-stage company stock, which will eventually be sold.

Strategic Applications and Financial Innovation

Charitable Remainder Trusts are more than just a donation vehicle; they are a testament to financial innovation, offering versatile solutions for complex planning scenarios. Their structure allows for creative strategies in estate planning, wealth transfer, and even the funding of future innovation and research.

Estate Planning and Wealth Transfer

CRTs play a pivotal role in comprehensive estate planning. By removing assets from the taxable estate, they help preserve wealth for future generations while fulfilling philanthropic goals. They provide a strategic method for transferring highly appreciated assets without immediate tax burdens, allowing for optimized asset utilization. This is particularly valuable for individuals with substantial estates looking to minimize tax liabilities while maximizing their impact on charitable causes. The ability to provide an income stream to non-charitable beneficiaries also means donors can support loved ones while still ensuring a significant legacy gift.

Funding Future Innovation and Research

Beyond individual wealth management, CRTs represent an innovative mechanism for sustained philanthropic support that can fuel long-term societal progress, including technological advancement and scientific research. By directing the remainder interest to educational institutions, research foundations, or non-profit organizations focused on cutting-edge technologies, CRTs become powerful engines for future innovation.

Imagine a donor passionate about artificial intelligence, renewable energy, or space exploration. By establishing a CRT and designating a university’s AI research lab or a specific technology-focused non-profit as the ultimate beneficiary, they are providing a future endowment that can fund groundbreaking projects, support emerging scientists, and accelerate the pace of discovery. The deferred nature of the charitable gift ensures that capital is available for a charity’s mission far into the future, providing a stable, predictable stream of funding that can be crucial for long-term research initiatives that require sustained investment. This innovative use of financial instruments allows individuals to leave a lasting mark on the technological landscape, shaping the future through their generosity.

Navigating Complexity and Professional Guidance

While the benefits of Charitable Remainder Trusts are substantial, their establishment and management involve considerable legal, financial, and tax complexities. Crafting a CRT requires careful consideration of the donor’s financial goals, philanthropic aspirations, tax situation, and the specific type of assets being contributed.

Key considerations include:

- Asset Selection: Deciding which assets to contribute (e.g., highly appreciated stock, real estate, cash) is crucial for maximizing tax advantages and income generation.

- Payout Rate and Term: Setting the appropriate payout rate and the duration of the income stream directly impacts the income received, the charitable deduction, and the size of the eventual charitable gift.

- Investment Strategy: The trustee of the CRT is responsible for investing the trust assets prudently to generate income and preserve the principal for the charitable remainder.

- Legal and Tax Compliance: CRTs must adhere to strict IRS regulations to qualify for their unique tax benefits. Errors in drafting or administration can lead to severe penalties.

Given these complexities, engaging experienced professionals—including estate planning attorneys, financial advisors specializing in charitable giving, and tax accountants—is essential. These experts can help design a CRT that aligns perfectly with a donor’s financial and charitable objectives, ensuring compliance with all legal requirements and maximizing the benefits for both the donor and the chosen charity. Through meticulous planning and expert guidance, a Charitable Remainder Trust can become a powerful tool for strategic philanthropy and a lasting legacy of support for the causes that matter most.