Business interruption insurance, often bundled with commercial property insurance, is a crucial safety net for businesses facing unexpected downtime. While property insurance may cover the physical damage to a business’s assets, it doesn’t typically address the resulting loss of income and increased operating expenses. This is where business interruption insurance steps in, aiming to restore a business to its financial position prior to the covered loss. Understanding precisely what this vital coverage entails is essential for any business owner seeking robust protection against unforeseen events.

Core Coverage Principles and Triggering Events

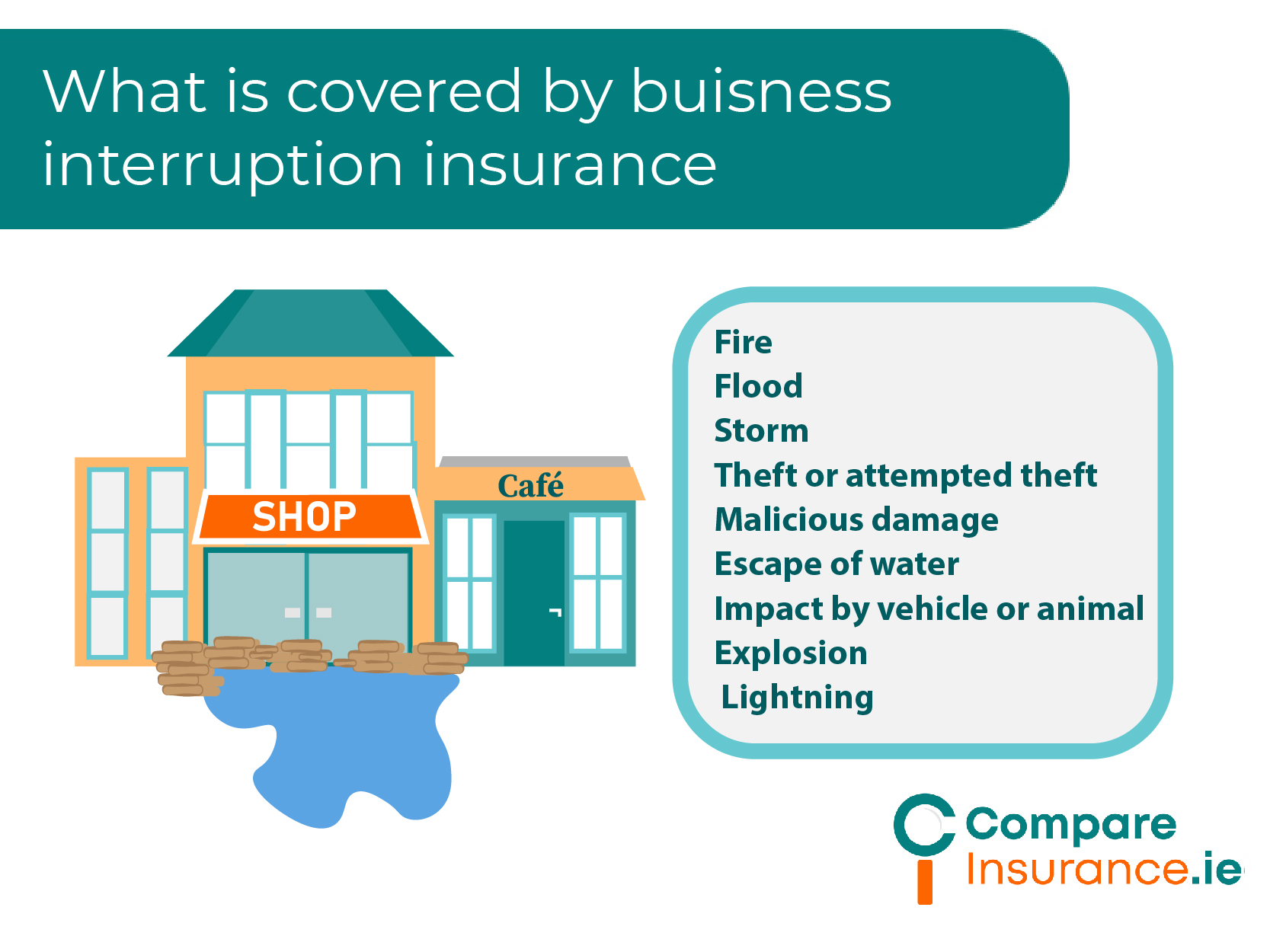

At its heart, business interruption insurance is designed to indemnify a business for the net income it loses and the necessary ongoing operating expenses it incurs due to a covered peril that forces a temporary cessation or significant slowdown of operations. The “covered peril” is a critical component, as the insurance policy will specifically list the types of events that trigger coverage. Typically, these are sudden and accidental physical losses, such as fire, windstorms, vandalism, or lightning.

Lost Income and Profits

The primary benefit of business interruption insurance is the compensation for lost net income. This includes not only profits that would have been earned but also normal operating expenses that continue even when the business is not operating at full capacity or is temporarily closed. These ongoing expenses can include payroll for essential staff, rent or mortgage payments, loan payments, taxes, and other fixed costs. The policy aims to ensure that the business can weather the storm without falling into financial distress due to the interruption.

Necessary Continuing Expenses

Beyond lost profits, the policy also covers “necessary continuing expenses.” This is a broad category that encompasses all the costs a business must continue to incur to keep its operations viable. Examples include:

- Rent or Mortgage Payments: Ensuring the business doesn’t lose its physical location due to inability to pay.

- Payroll: Maintaining key employees who are essential for resuming operations once the premises are available or repairs are complete. This is particularly important for specialized skills or long-term staff.

- Utilities: Costs for electricity, water, and gas, even if the business is not fully operational, may be necessary to maintain equipment or security.

- Loan Payments and Other Debt Obligations: Preventing default on financial commitments.

- Taxes: Ensuring tax obligations are met to avoid penalties.

- Insurance Premiums: Continuing to pay for other essential insurance policies.

The definition of “necessary” is important. It refers to expenses that are unavoidable and continue regardless of whether the business is generating revenue.

Extended Period of Indemnity

Many policies include an “extended period of indemnity” clause. This is a crucial feature that recognizes that even after the physical damage has been repaired and the business has reopened, it may take time to return to pre-loss revenue levels. The extended period of indemnity allows the business to continue receiving benefits for a specified period after reopening to help it regain its lost profitability and market share. This period can range from a few weeks to several months, depending on the policy and the severity of the interruption.

Common Triggering Perils and Exclusions

The scope of business interruption coverage is directly tied to the perils that are covered by the underlying property insurance policy. If a peril is excluded from the property damage coverage, it will almost certainly be excluded from business interruption coverage as well.

Covered Perils

Commonly covered perils include:

- Fire and Smoke: A widespread cause of business interruption, covering damage from flames, heat, and smoke.

- Windstorms and Hail: Particularly relevant in regions prone to severe weather, covering damage from high winds and hailstones.

- Vandalism and Malicious Mischief: Intentional damage to property by third parties.

- Lightning: Damage caused by lightning strikes.

- Explosion: Damage resulting from an explosion.

- Civil Authority: This can cover lost income if a civil authority (like the government) prohibits access to the insured premises due to damage to adjacent property caused by a covered peril. For example, if a fire in an adjacent building causes authorities to cordon off your block, you might be covered.

Common Exclusions

It is equally important to understand what business interruption insurance does not cover. Common exclusions include:

- Flood and Water Damage (unless caused by a covered peril): Standard flood damage is typically excluded unless a separate flood insurance policy is purchased. However, if a covered peril (like a windstorm) causes a leak that results in water damage, that might be covered.

- Earthquake and Earth Movement: Similar to flood, earthquake damage usually requires a separate policy.

- Power Outages (unless caused by a covered peril): A general power outage affecting a wider area is usually not covered. However, if the outage is caused by a covered peril (e.g., a lightning strike damaging a local utility pole), then resulting business interruption might be covered.

- Mechanical Breakdown or Utility Failure: If a machine in your business breaks down, or your internal power system fails, this is generally not covered.

- Wear and Tear: Damage resulting from gradual deterioration rather than a sudden, accidental event.

- Acts of War or Terrorism: These catastrophic events are typically excluded.

- Pandemics and Epidemics: While the COVID-19 pandemic highlighted the need for coverage related to widespread health crises, most standard business interruption policies exclude losses arising from infectious diseases. Some policies may offer endorsements or separate coverage for communicable diseases, but these are often specific and costly.

- Cyber-Attacks and Data Breaches: Unless specifically endorsed, business interruption arising from cyber incidents is usually excluded. Specialized cyber insurance is needed for these risks.

Additional Coverage Endorsements

Beyond the core coverage, several endorsements can expand the protection offered by business interruption insurance, addressing specific scenarios and common limitations. These endorsements are critical for tailoring the policy to the unique risks faced by a particular business.

Extra Expense Coverage

While business interruption insurance focuses on lost income and continuing expenses, “extra expense” coverage addresses the additional costs a business incurs to resume operations as quickly as possible, even if it means operating at a higher cost temporarily. This could include renting temporary office space, purchasing new equipment immediately, paying overtime to employees to expedite repairs, or advertising to inform customers of a new temporary location. The goal is to minimize the duration of the interruption, and extra expense coverage facilitates this by allowing the business to spend money to save money in the long run by getting back to generating revenue sooner.

Contingent Business Interruption (CBI)

This endorsement covers losses incurred when a business’s operations are interrupted due to damage or disruption at a supplier or key customer’s premises. For example, if a critical supplier experiences a fire that halts production of a component your business relies on, CBI could provide coverage for your lost income. Similarly, if a major client’s facility is destroyed, and they can no longer purchase your products, CBI might apply. This coverage recognizes the interconnectedness of modern supply chains.

Civil Authority or Order of Civil Authority Coverage

As mentioned earlier, this coverage can be triggered when a government or civil authority prohibits access to your business premises due to damage to property other than your own, caused by a covered peril. This is distinct from being directly damaged. For instance, if a fire next door forces the city to evacuate your block for safety reasons, and you cannot operate your business, this coverage can help compensate for your lost income.

Ingress/Egress Interruption

This endorsement covers lost business income resulting from the inability to access the insured premises due to damage to a road or bridge leading to the business, caused by a covered peril. This is particularly relevant for businesses located in remote areas or those heavily reliant on specific access routes.

Loss Mitigation Expenses

Some policies may cover reasonable expenses incurred by the business to mitigate the loss, meaning to reduce the extent or duration of the business interruption. This could include temporary repairs, securing the premises, or other actions taken to prevent further damage or delay.

Computer Systems Interruption

Standard policies often exclude business interruption caused by the failure of computer systems or data loss. A specific endorsement can be added to cover lost income and extra expenses resulting from such events, provided they are caused by a covered peril.

Determining the Period of Restoration

A critical aspect of business interruption insurance is the “period of restoration” or “period of interruption.” This is the timeframe during which the insurance company will pay benefits. It begins when the damaged property is physically repaired or replaced and the business can resume operations, and it ends when the business has returned to its “normal” operating capacity or the policy limit is reached, whichever comes first.

Defining “Normal” Operations

The definition of “normal” operations is crucial. It generally refers to the level of gross earnings the business would have achieved had the loss not occurred. This is why maintaining detailed financial records is paramount for accurately calculating and substantiating claims. Insurance adjusters will compare post-loss financial performance against pre-loss projections and historical data to determine the extent of lost income.

Limits and Waiting Periods

Business interruption policies will have specific limits on the total payout and often a waiting period (also known as a deductible period or elimination period) before coverage begins. This waiting period, typically ranging from 24 hours to 72 hours, means the business must absorb the losses for that initial period. The waiting period is usually measured in days of suspension of operations rather than dollar amounts.

For example, a 72-hour waiting period means that the insurer will not pay for the first 72 hours of lost business income following the commencement of the interruption.

Policy Limits and Valuation

It’s essential to understand the policy limits. These are the maximum amounts the insurer will pay for business interruption losses. These limits can be a specific dollar amount, a time limit (e.g., 12 months of coverage), or a percentage of the property damage coverage. Businesses must ensure their coverage limits are sufficient to cover potential losses, considering their revenue, expenses, and the potential duration of an interruption.

Valuation methods for business interruption claims can be complex. Insurers typically use the “gross earnings” form or the “actual loss sustained” form. The gross earnings form covers lost net profit and continuing operating expenses, but it often has a provision to prevent recovery for expenses that would have ceased had the business not been interrupted. The actual loss sustained form is broader, covering the actual reduction in net profit and continuing expenses. Understanding which valuation method your policy uses is key.

Conclusion: Proactive Risk Management and Policy Review

Business interruption insurance is not a “set it and forget it” policy. It requires proactive risk management and regular review. Businesses should:

- Understand Their Risks: Identify potential threats and their impact on operations.

- Maintain Accurate Records: Keep meticulous financial records, including projections, to support claims.

- Review Policies Annually: Ensure coverage limits, endorsements, and definitions align with current business needs and risks.

- Consult with Professionals: Work with experienced insurance brokers and agents to tailor coverage and understand policy nuances.

- Consider Endorsements: Evaluate endorsements like Extra Expense, Contingent Business Interruption, and Civil Authority to fill potential coverage gaps.

By thoroughly understanding what business interruption insurance covers and diligently managing their policies, businesses can significantly enhance their resilience and ability to recover from unforeseen disruptions, safeguarding their financial future.