When navigating the complex world of automotive financing, a cosigner plays a pivotal role, often serving as the bridge between a borrower with a less-than-ideal credit profile and a lender willing to extend credit. While the immediate association with a cosigner is their willingness to guarantee a loan, their responsibilities and the implications for all parties involved extend far beyond this initial understanding. This article will delve into the multifaceted role of a cosigner for a car loan, examining their functions, the prerequisites for becoming one, the inherent risks and benefits, and the crucial steps involved in the cosigning process. Understanding these dynamics is essential for anyone considering or being asked to cosign a car loan.

The Essential Functions of a Car Loan Cosigner

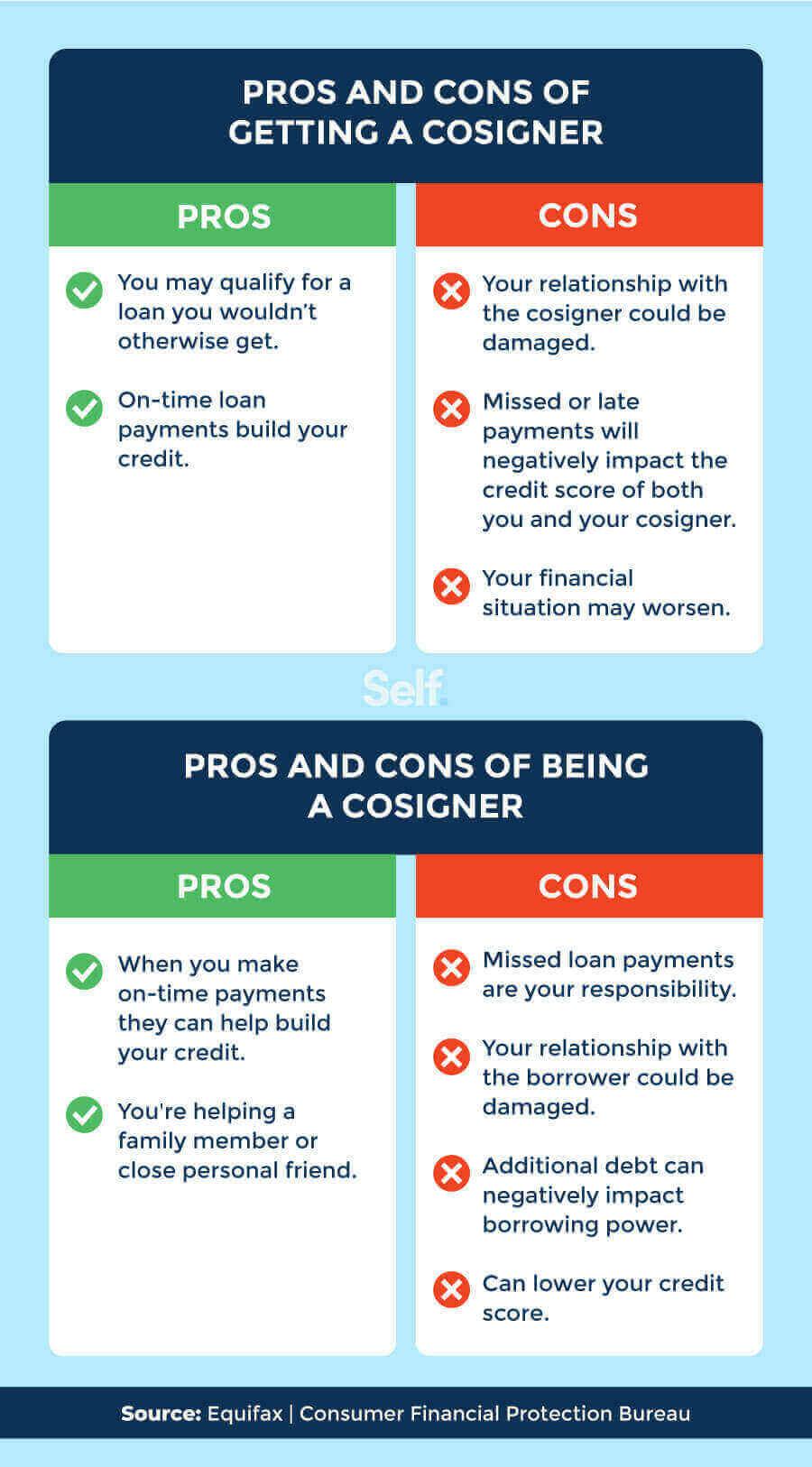

At its core, a cosigner acts as a secondary guarantor for a car loan. This means they are legally obligated to make the loan payments if the primary borrower defaults. This commitment provides lenders with an added layer of security, significantly reducing their risk. Without a cosigner, individuals with insufficient credit history, low credit scores, or a history of financial instability might find it exceedingly difficult, if not impossible, to secure financing for a vehicle.

Guaranteeing Loan Repayment

The primary function of a cosigner is to backstop the loan. Lenders assess the creditworthiness of the primary borrower. If that assessment reveals a higher risk of default, the lender may require a cosigner. By agreeing to cosign, an individual with a strong credit history effectively lends their credibility to the borrower. This significantly improves the borrower’s chances of loan approval and can often lead to more favorable loan terms, such as lower interest rates and longer repayment periods. The cosigner’s promise to pay ensures the lender doesn’t bear the full brunt of a borrower’s financial hardship.

Improving Loan Approval Chances

For individuals struggling to get approved for a car loan on their own, a cosigner is often the key to unlocking financing. This is particularly relevant for young adults starting their financial journey, individuals rebuilding their credit after a period of financial difficulty, or those with limited credit history. The cosigner’s established creditworthiness reassures the lender, making them more comfortable extending credit. This is not just about getting approved; it’s about getting approved on terms that are manageable for the borrower.

Securing Better Loan Terms

Beyond mere approval, a cosigner can significantly influence the terms of the loan. Lenders offer lower interest rates and more favorable repayment structures to borrowers who present less risk. By having a cosigner with a strong credit profile, the perceived risk to the lender is reduced. This can translate into substantial savings for the borrower over the life of the loan, as a lower interest rate means less money paid in finance charges. In some cases, the difference in interest rates can be significant enough to make a substantial impact on the overall cost of the vehicle.

Who Can Be a Car Loan Cosigner?

Not everyone is suited to be a cosigner. The role demands a robust financial standing and a deep understanding of the commitment involved. Lenders have specific criteria that a prospective cosigner must meet to ensure they can genuinely back the loan.

Strong Credit History and Score

The most critical requirement for a cosigner is a strong credit history and a good to excellent credit score. Lenders will scrutinize the cosigner’s credit report to assess their past borrowing behavior, payment timeliness, and overall credit utilization. A history of responsible credit management, with a consistent record of making payments on time and maintaining low credit utilization, is paramount. Lenders typically look for credit scores in the high 600s or above, with many preferring scores in the 700s or 800s for optimal loan terms.

Stable Income and Employment

Beyond creditworthiness, lenders need assurance that the cosigner has the financial capacity to take on the added debt obligation. This typically means demonstrating a stable income and consistent employment history. The lender will likely require proof of income, such as pay stubs, tax returns, or bank statements, to verify the cosigner’s ability to afford the monthly car payments, in addition to their existing financial obligations. A stable job and a reliable income stream are crucial indicators of financial stability.

Understanding of Financial Responsibility

A cosigner must possess a clear understanding of the legal and financial implications of their commitment. It is not a favor to be undertaken lightly. They need to comprehend that their credit score will be affected by the loan’s performance, that they are legally liable for the debt, and that failure to repay could lead to severe financial consequences, including damage to their own credit rating and potential legal action. Open and honest communication between the borrower and the cosigner is vital before any agreement is made.

Risks and Benefits for the Cosigner

Becoming a cosigner carries significant weight, presenting both potential benefits and substantial risks that must be carefully weighed.

Potential Benefits

The primary benefit for a cosigner, especially a close family member or friend, is the ability to help someone they care about achieve a significant goal, such as obtaining reliable transportation. For the cosigner themselves, if the loan is managed impeccably by the primary borrower, the loan can, in some instances, positively impact the cosigner’s credit score. This occurs if the loan payments are consistently made on time, as this demonstrates responsible credit behavior. However, this benefit is secondary and contingent on the borrower’s adherence to the loan terms.

Significant Risks

The risks associated with cosigning are considerable and cannot be overstated. The most significant risk is that the borrower defaults on the loan. If this happens, the lender will pursue the cosigner for the outstanding debt. This can result in the cosigner having to make the full loan payments, even if they never drove the car or benefited from its use. Furthermore, the default will be reported on the cosigner’s credit report, severely damaging their credit score. This can make it harder for the cosigner to secure their own loans, mortgages, or credit cards in the future. The lender may also repossess the vehicle, and the cosigner could still be liable for any deficiency balance remaining after the vehicle is sold.

Impact on Credit Score

Even if the borrower makes all payments on time, the presence of a cosigned loan can affect the cosigner’s credit utilization ratio and their debt-to-income ratio, which are factors lenders consider when evaluating new credit applications. A cosigned loan is considered a debt obligation of the cosigner, and it will appear on their credit report. If the loan is a substantial amount, it could make it appear to other lenders that the cosigner has taken on a significant financial burden, potentially impacting their ability to qualify for other credit or limiting the amount they can borrow.

The Cosigning Process and Best Practices

Successfully navigating the cosigning process requires careful planning, clear communication, and a thorough understanding of the steps involved.

Loan Application and Agreement

The process typically begins with the primary borrower applying for a car loan. During the application, the borrower will indicate they intend to have a cosigner. The lender will then require the cosigner to complete a separate loan application, which will include their personal information, employment details, and financial history. The cosigner will also need to provide consent for the lender to pull their credit report. Both parties will need to review and sign the loan agreement, acknowledging the terms and the cosigner’s responsibilities.

Due Diligence and Communication

Before agreeing to cosign, it is imperative for the prospective cosigner to conduct due diligence. This involves having an open and honest conversation with the primary borrower about their financial situation, their ability to afford the monthly payments, and their plan for repayment. The cosigner should review the proposed loan terms, including the interest rate, loan amount, and repayment period, to ensure they are comfortable with the financial commitment. It’s also wise for the cosigner to understand the borrower’s budget and their overall financial health.

Ongoing Monitoring and Exit Strategy

While the primary responsibility for loan payments lies with the borrower, a vigilant cosigner may choose to monitor the loan’s progress. This can involve regularly checking their own credit report for any discrepancies or late payments, or asking the borrower for proof of timely payments. Establishing an “exit strategy” is also a wise consideration. This could involve the borrower refinancing the loan into their name alone once their credit has improved or when they have demonstrated a consistent payment history. This frees the cosigner from their obligation and is a desirable outcome for all parties. The cosigner should ensure they understand the conditions under which they can be released from the loan obligation, if such provisions are even available.

In conclusion, a cosigner for a car loan acts as a vital financial guarantor, enabling borrowers with credit challenges to secure financing and potentially achieve better loan terms. However, this role is fraught with significant risks, primarily the legal obligation to repay the loan if the primary borrower defaults, which can severely damage the cosigner’s credit and financial well-being. Therefore, a thorough understanding of the responsibilities, risks, and the entire cosigning process, coupled with open communication and careful consideration, is essential before undertaking this important financial commitment.