In the world of real estate and business financing, the term “no doc loan” often surfaces, sparking curiosity and sometimes a degree of apprehension. While the allure of simplified borrowing is undeniable, understanding the nuances, benefits, and inherent risks associated with these loan products is paramount for any prospective borrower. This article aims to demystify no doc loans, exploring their fundamental nature, the types of borrowers they cater to, and the critical considerations one must undertake before embarking on such a financial path.

Understanding the “No Doc” Concept

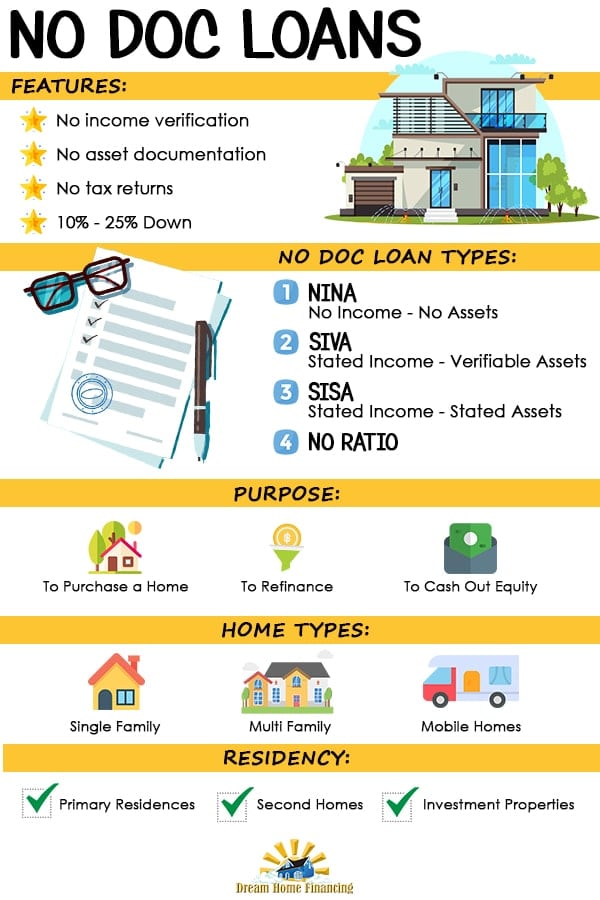

The core of a no doc loan lies in its name: it significantly reduces or entirely eliminates the stringent documentation requirements typically associated with traditional lending. In a conventional loan application, borrowers are expected to provide a comprehensive suite of financial documents, including pay stubs, tax returns, bank statements, and proof of assets. This detailed vetting process allows lenders to meticulously assess a borrower’s creditworthiness, income stability, and overall financial capacity to repay the loan.

No doc loans, on the other hand, operate under a different premise. Instead of relying heavily on verifiable income and asset statements, these loans often place a greater emphasis on the borrower’s credit score and the perceived value of the asset being financed, such as a property. The rationale behind this approach is to streamline the lending process, making it faster and more accessible for individuals or businesses who may have difficulty providing traditional documentation. This could be due to irregular income streams, self-employment, or a desire for rapid financing.

The Spectrum of Documentation Reduction

It’s important to recognize that “no doc” is not always a binary state. Loans can exist on a spectrum of documentation reduction, ranging from “low doc” to “no doc.”

Low Doc Loans

Low doc loans represent a middle ground. While they still require less documentation than traditional loans, they are not entirely devoid of paperwork. Borrowers might be asked to provide a self-declaration of income, possibly supplemented by a bank statement or two. These loans are often suitable for self-employed individuals or small business owners whose income fluctuates or is not easily captured by standard payroll records. The lender, in this scenario, is still seeking some level of assurance regarding the borrower’s ability to repay, but with less rigorous proof.

True No Doc Loans

True no doc loans, as the name implies, demand minimal to no proof of income or employment from the borrower. The approval process primarily hinges on the borrower’s credit history and the collateral’s loan-to-value ratio. For instance, in a real estate context, a lender might approve a no doc mortgage based on the borrower’s excellent credit score and the substantial equity in the property they are purchasing or refinancing. The assumption is that the borrower’s creditworthiness is sufficient to mitigate the risk associated with the lack of income verification. These are often seen in specialized lending scenarios or for borrowers with exceptionally strong credit profiles.

Why Do No Doc Loans Exist?

The existence of no doc loans can be attributed to several factors:

- Meeting Market Demand: There is a segment of the borrowing population that finds traditional loan application processes burdensome or impossible to navigate. No doc loans offer a solution for these individuals and businesses.

- Speed and Efficiency: For borrowers who require rapid access to funds, the reduced documentation process of no doc loans can significantly expedite the approval and funding timeline. This is particularly attractive for time-sensitive investments or opportunities.

- Flexibility for Alternative Income Sources: Individuals with income from multiple sources, freelance work, or businesses with fluctuating revenue may struggle to meet the strict income verification requirements of conventional loans. No doc loans provide a pathway to financing for these borrowers.

- Investor Focus: In some investment scenarios, particularly in real estate, lenders may be more inclined to focus on the asset’s value and the borrower’s exit strategy rather than detailed income verification, especially if the borrower demonstrates strong financial discipline through their credit history.

Who Benefits from No Doc Loans?

While no doc loans offer a seemingly attractive alternative, they are not universally suitable. Certain borrower profiles and situations align more favorably with the advantages these loans provide.

Self-Employed Individuals and Freelancers

Perhaps the most prominent beneficiaries of no doc loans are individuals who are self-employed or work as freelancers. Their income is often irregular, project-based, or derived from various sources that are difficult to consolidate into traditional pay stubs and tax returns. For example, a graphic designer who earns income from multiple clients throughout the year, or a contractor whose earnings vary seasonally, might find it challenging to demonstrate a consistent income stream acceptable to conventional lenders. A no doc loan allows them to leverage their assets or creditworthiness without the hurdles of proving fluctuating income.

Business Owners with Complex Financial Structures

Small and medium-sized business owners often have intricate financial structures that can make traditional income verification a complex undertaking. If a business owner’s personal income is tied directly to business profits, and those profits fluctuate, they may encounter difficulties securing conventional loans. No doc loans can provide a streamlined path for these entrepreneurs to access capital for business expansion, working capital, or other ventures, relying more on the business’s asset value or the owner’s credit history.

Real Estate Investors

Real estate investors, particularly those with substantial portfolios or significant equity in their properties, can also find no doc loans beneficial. These loans are often used for investment properties where the projected rental income or the resale value of the property is a primary consideration for the lender. An investor with a strong track record and a solid credit score might be approved for a no doc investment property loan based on the property’s potential and their ability to manage multiple assets, rather than a detailed personal income assessment.

Borrowers with Excellent Credit Scores

A consistently strong credit score is often the cornerstone of no doc loan approval. Lenders extend these loans with reduced documentation precisely because they trust the borrower’s history of responsible credit management. A high credit score signals to the lender that the borrower is likely to repay their debts, even in the absence of extensive income verification. Therefore, individuals with a proven history of financial reliability are prime candidates for no doc financing.

Borrowers Seeking Expedited Financing

In situations where time is of the essence, such as seizing a time-limited investment opportunity or needing to close a deal quickly, the speed of no doc loans can be a significant advantage. The simplified application and approval process can drastically shorten the time from application to funding compared to traditional loans, which can involve lengthy underwriting and documentation review periods.

Risks and Considerations of No Doc Loans

While the appeal of reduced documentation and speed is undeniable, it is crucial to approach no doc loans with a clear understanding of the inherent risks and considerations involved. These loans often come with trade-offs that can significantly impact the borrower in the long run.

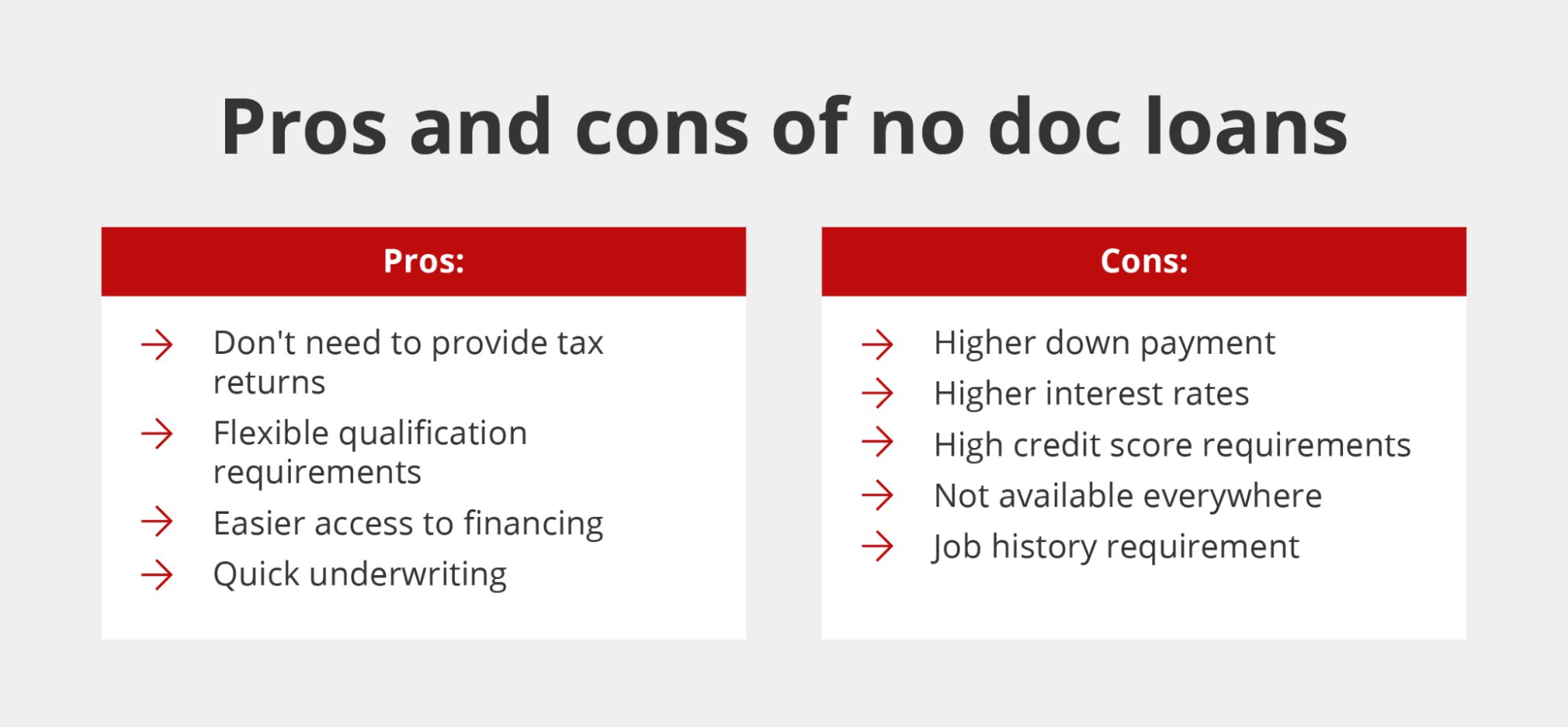

Higher Interest Rates and Fees

The reduced documentation and the perceived higher risk for the lender are typically reflected in the loan terms. No doc loans often carry higher interest rates and may include more substantial origination fees, closing costs, or other associated charges. These increased costs can lead to a higher overall cost of borrowing over the life of the loan, making it more expensive than a traditional loan with comparable terms. Borrowers must meticulously compare the total cost of a no doc loan against traditional options to ensure it remains financially viable.

Increased Risk of Default

The very nature of reduced income verification inherently increases the risk of default. Without a thorough understanding of the borrower’s current income stability and capacity to repay, lenders are taking on a greater gamble. For the borrower, this translates to a higher likelihood of falling behind on payments if their financial circumstances change unexpectedly. Defaulting on a no doc loan can have severe consequences, including foreclosure on the property, significant damage to credit scores, and legal repercussions.

Importance of Collateral and Creditworthiness

Given the limited reliance on income verification, the borrower’s creditworthiness and the value of the collateral become paramount. A strong credit score and a substantial down payment or equity in the asset are often non-negotiable requirements. If these factors are not exceptionally strong, obtaining a no doc loan may be difficult, or the terms offered might be exceptionally unfavorable. Borrowers must ensure they meet these stringent collateral and credit requirements before pursuing this type of financing.

Potential for Predatory Lending

Unfortunately, the market for no doc loans can sometimes attract predatory lenders who may exploit borrowers’ desperation or lack of financial literacy. These lenders might offer seemingly attractive terms initially, only to reveal hidden fees or excessively high interest rates later in the process. It is imperative for borrowers to conduct thorough due diligence on any lender offering no doc loans, checking their reputation, licensing, and reading reviews from other customers.

Understanding Loan Covenants and Repayment Terms

Even with reduced documentation, borrowers must fully understand all loan covenants, repayment schedules, and any specific conditions attached to the no doc loan. This includes understanding what constitutes a default, the penalties for late payments, and any options for loan modification or refinancing. Misunderstanding these terms can lead to unforeseen financial distress.

In conclusion, no doc loans can serve as a valuable financial tool for specific borrowers and situations, offering speed and accessibility where traditional lending falls short. However, their advantages are invariably balanced by increased costs and potential risks. A thorough understanding of what constitutes a no doc loan, who it benefits, and the crucial considerations involved is essential for any borrower to make an informed decision and navigate this less conventional lending landscape successfully. Diligence, careful comparison of offers, and a realistic assessment of one’s own financial capacity are the keys to leveraging the potential of no doc loans without falling victim to their inherent drawbacks.