The phrase “what a trust fund” can evoke images of inherited wealth, lavish lifestyles, and perhaps a touch of envy. While the popular perception often focuses on the glamorous side, the reality of trust funds is far more nuanced, extending into sophisticated financial planning, asset management, and the strategic preservation of wealth for future generations. Understanding what a trust fund truly entails requires delving beyond the superficial and appreciating its intricate mechanisms and profound implications for both settlors and beneficiaries.

The Foundation of a Trust Fund

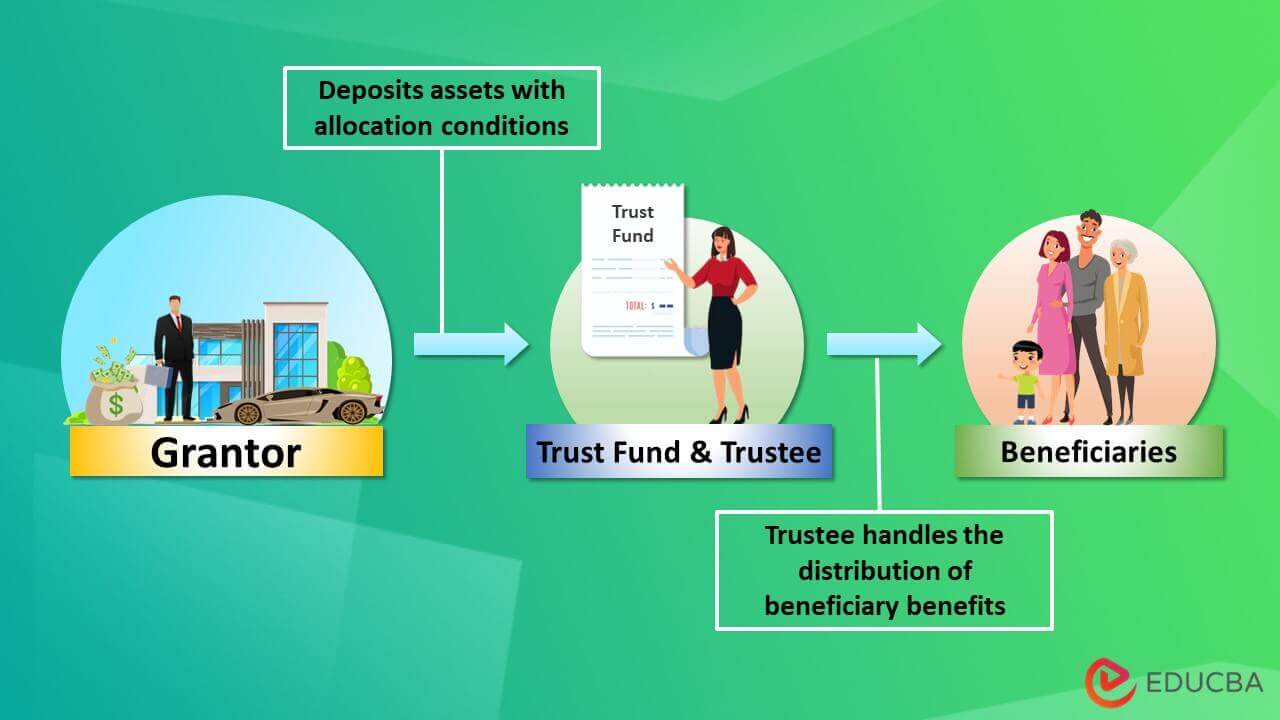

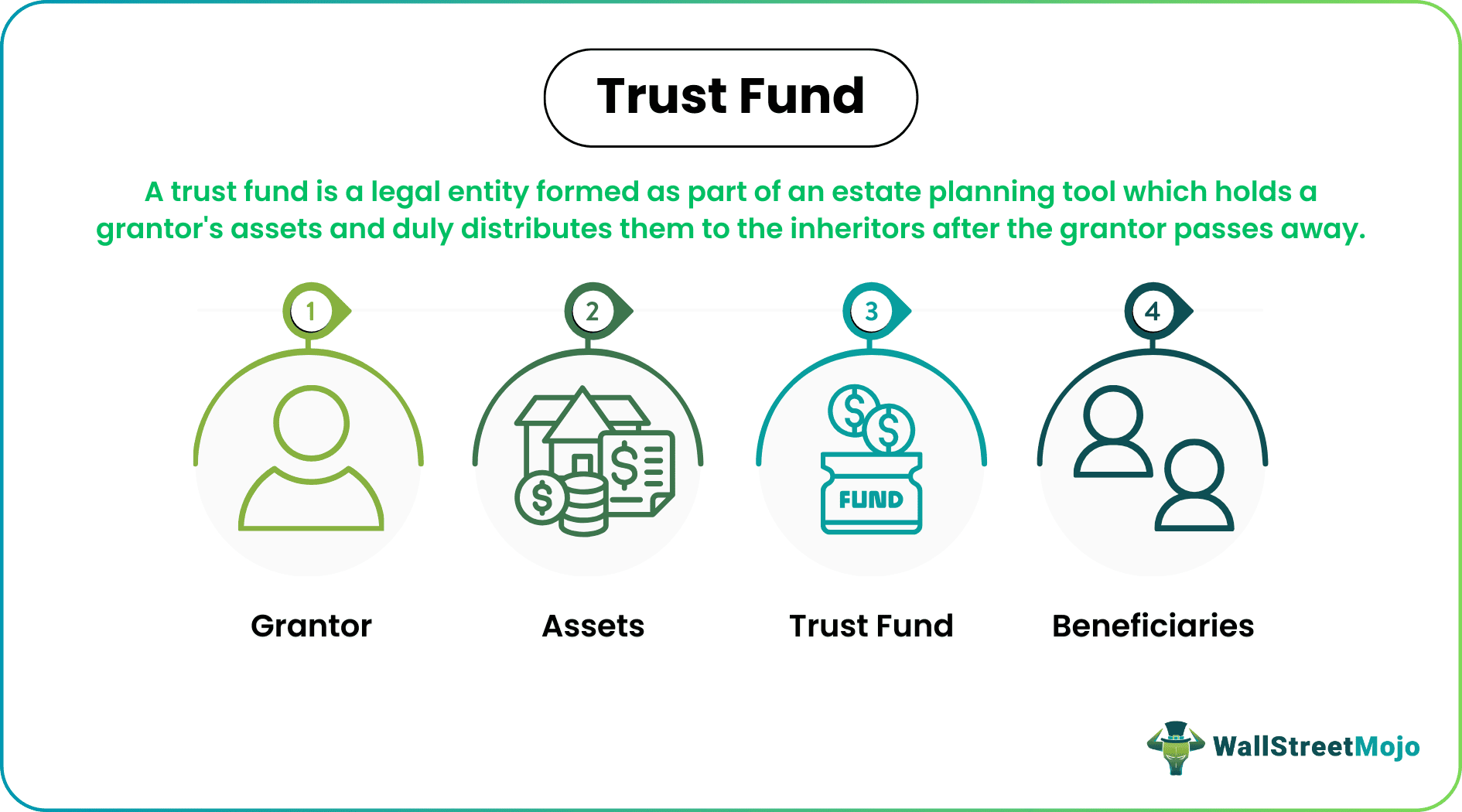

At its core, a trust fund is a legal arrangement where a designated individual or entity, known as the trustee, holds and manages assets on behalf of one or more beneficiaries. This arrangement is established through a trust document, which meticulously outlines the terms, conditions, and distribution protocols for the assets. The person who creates the trust and transfers assets into it is called the settlor, grantor, or trustor. The settlor’s primary intent is typically to provide financial security, support, or a legacy for the beneficiaries, often over an extended period.

Types of Trusts

The world of trusts is diverse, with various structures designed to meet specific needs and objectives. Understanding these distinctions is crucial for appreciating the full scope of “what a trust fund” can represent.

Revocable vs. Irrevocable Trusts

A fundamental distinction lies between revocable and irrevocable trusts. A revocable trust can be altered or terminated by the settlor during their lifetime. This offers flexibility, allowing the settlor to make changes as circumstances evolve. However, assets in a revocable trust are generally still considered part of the settlor’s estate for tax purposes and can be subject to creditors’ claims.

Conversely, an irrevocable trust generally cannot be amended or revoked by the settlor once established. This permanence provides significant benefits, particularly in terms of estate tax reduction and asset protection. Assets transferred to an irrevocable trust are typically removed from the settlor’s taxable estate, and they are also shielded from the settlor’s personal creditors.

Living Trusts vs. Testamentary Trusts

The timing of a trust’s establishment also defines its category. A living trust (also known as an inter vivos trust) is created and funded during the settlor’s lifetime. This allows for the seamless transfer of assets to beneficiaries upon the settlor’s death, often avoiding the complexities and delays associated with probate.

A testamentary trust, on the other hand, is created through a will and only comes into effect after the settlor’s death. While it serves a similar purpose of asset distribution and management, it must go through the probate process before it can be established.

Charitable Trusts

For individuals with philanthropic goals, charitable trusts offer a powerful way to support charitable causes while potentially realizing tax benefits. These trusts can be structured to provide income to beneficiaries for a period, with the remaining assets eventually passing to a designated charity, or they can directly benefit a charity from the outset.

Special Needs Trusts

A crucial type of trust for families with individuals with disabilities is the special needs trust. This type of trust allows for assets to be held for the benefit of a disabled individual without jeopardizing their eligibility for essential government benefits, such as Supplemental Security Income (SSI) and Medicaid. The funds are used to supplement, not replace, these benefits, covering items and services not provided by government assistance.

The Mechanics of Trust Fund Management

Beyond the initial establishment, the ongoing management of a trust fund is a critical aspect of its functionality. This involves a range of responsibilities and strategic decisions designed to preserve and grow the assets while adhering to the settlor’s intentions.

The Role of the Trustee

The trustee is the linchpin of any trust fund. This individual or entity bears a fiduciary duty to act in the best interests of the beneficiaries. Their responsibilities are multifaceted and demanding.

Fiduciary Duties

The concept of a fiduciary duty is paramount. It encompasses several key obligations:

- Duty of Loyalty: The trustee must act solely in the interest of the beneficiaries, avoiding any self-dealing or conflicts of interest.

- Duty of Prudence: The trustee must manage the trust assets with the care, skill, and caution that a prudent person would exercise in managing their own affairs. This includes making sound investment decisions, diversifying assets, and regularly reviewing the portfolio.

- Duty to Account: Trustees are required to maintain accurate records of all trust transactions and provide regular accountings to the beneficiaries, detailing income, expenses, and asset values.

- Duty to Inform and Communicate: Trustees must keep beneficiaries reasonably informed about the trust’s administration and their rights under the trust.

Investment Management

A significant responsibility of the trustee is the prudent investment of trust assets. This involves developing an investment strategy that aligns with the trust’s objectives, the beneficiaries’ needs, and the prevailing market conditions. Diversification across various asset classes, such as stocks, bonds, real estate, and alternative investments, is typically employed to mitigate risk and enhance returns.

Distribution of Assets

The trustee is responsible for distributing trust assets according to the terms outlined in the trust document. This can involve making regular income payments, periodic distributions of principal, or lump-sum distributions upon the occurrence of specific events, such as a beneficiary reaching a certain age or graduating from college. The trustee must exercise discretion judiciously if the trust document grants them such authority.

The Purpose and Advantages of Trust Funds

The decision to establish a trust fund is rarely arbitrary. It is typically driven by a desire to achieve specific financial and personal goals that might be difficult or impossible to accomplish through other means.

Estate Planning and Wealth Preservation

One of the most common reasons for creating a trust fund is its integral role in comprehensive estate planning. Trusts can facilitate the orderly transfer of assets to heirs, bypassing the often lengthy and public probate process. This can lead to significant savings in time and administrative costs.

Furthermore, trusts are instrumental in preserving wealth across generations. By structuring distributions and setting conditions, settlors can encourage responsible financial behavior among beneficiaries, ensuring that the inherited wealth serves its intended purpose rather than being quickly depleted.

Asset Protection

Irrevocable trusts offer a robust shield against potential creditors and legal claims. Once assets are transferred into an irrevocable trust, they are generally no longer considered the personal property of the settlor, thereby protecting them from lawsuits, bankruptcies, and other financial liabilities. This protection can be particularly valuable for individuals in professions with high liability risks or those concerned about future financial uncertainties.

Tax Efficiency

Trusts can be powerful tools for minimizing estate and gift taxes. By strategically placing assets into trusts, particularly irrevocable ones, settlors can reduce the taxable value of their estates, thereby lessening the burden of estate taxes for their heirs. Certain types of trusts, like grantor retained annuity trusts (GRATs) and qualified personal residence trusts (QPRTs), are specifically designed to leverage tax advantages in wealth transfer.

Control and Flexibility

While irrevocable trusts relinquish control to the trustee, they still allow the settlor to exert influence over how assets are managed and distributed. The trust document can stipulate specific investment guidelines, distribution criteria, and even conditions that beneficiaries must meet. For revocable trusts, the settlor retains complete control, able to modify or revoke the trust as needed. This ability to dictate future financial outcomes provides a sense of security and control over one’s legacy.

Providing for Minors or Incapacitated Individuals

Trusts are an invaluable mechanism for providing for the financial well-being of minor children or individuals who may be unable to manage their own finances due to age, disability, or other reasons. A trustee can manage the assets and make distributions for the beneficiary’s support, education, and general welfare until they are deemed capable of handling their own affairs or until specific trust provisions are met.

The Nuances and Considerations

While the advantages of trust funds are substantial, establishing and managing them involves a degree of complexity and requires careful consideration.

Cost of Establishment and Administration

Setting up a trust fund typically involves legal fees for drafting the trust document, as well as ongoing costs for trustee fees, accounting, and investment management. For smaller estates, the administrative costs might outweigh the benefits, making simpler estate planning tools more appropriate.

Choice of Trustee

Selecting the right trustee is perhaps one of the most critical decisions a settlor will make. The trustee must possess the financial acumen, integrity, and understanding of the settlor’s wishes to effectively manage the trust. Options include individual trustees (family members, friends), corporate trustees (banks, trust companies), or a combination of both. Each option has its own set of advantages and disadvantages regarding cost, expertise, and impartiality.

Beneficiary Considerations

The terms of the trust must be carefully crafted to consider the beneficiaries’ financial literacy, maturity, and individual circumstances. Poorly designed trusts can inadvertently create dependency, encourage irresponsible spending, or fail to adequately meet the beneficiaries’ needs. Open communication between the settlor, trustee, and beneficiaries, where appropriate, can help ensure the trust serves its intended purpose effectively.

Legal and Tax Implications

Trust law and tax regulations are complex and subject to change. It is imperative to work with experienced legal and financial professionals to ensure the trust is structured correctly, complies with all applicable laws, and achieves the desired tax outcomes. Missteps in drafting or administration can lead to unintended tax liabilities or legal challenges.

In conclusion, “what a trust fund” is far more than just a vehicle for inherited wealth. It represents a sophisticated legal and financial instrument designed for meticulous planning, robust asset protection, and the enduring preservation of wealth and legacy. From the foundational legal structures to the intricate management and distribution protocols, trusts offer a powerful and adaptable solution for individuals seeking to secure their financial future and that of their loved ones for generations to come.