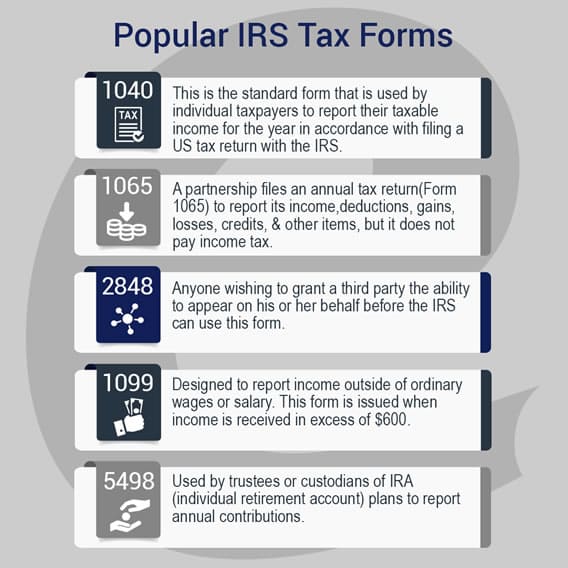

The “1040” is a fundamental document in the United States tax system, and understanding its purpose is crucial for millions of individuals and families each year. It serves as the primary form for filing federal income tax returns. This comprehensive document is where taxpayers report their income, calculate their tax liability, and determine whether they owe additional tax or are due a refund. Its usage extends beyond simply reporting income; it’s a tool for claiming deductions, credits, and other adjustments that can significantly impact the final tax obligation.

Understanding the Basics of the 1040 Form

The 1040 form, officially known as the U.S. Individual Income Tax Return, is the cornerstone of the annual tax filing process for most American taxpayers. It’s designed to capture a wide array of financial information necessary for the Internal Revenue Service (IRS) to assess an individual’s tax situation. Its origins date back to the early days of the income tax system, evolving over time to accommodate changes in tax law and the complexities of modern financial lives.

Who Needs to File a 1040?

The primary requirement for filing a Form 1040 is based on your gross income for the tax year. Generally, if your gross income exceeds certain thresholds, you are required to file. These thresholds are adjusted annually for inflation and depend on your filing status (e.g., single, married filing jointly, head of household). Even if your income falls below these thresholds, you might still choose to file if you had federal income tax withheld from your paychecks, as filing would allow you to claim a refund. Additionally, certain other situations, such as owing special taxes like self-employment tax, may necessitate filing a 1040 regardless of your gross income.

Key Information Collected on the 1040

The 1040 form is structured to systematically gather all the essential information needed for tax computation. This includes:

- Personal Information: Your name, address, Social Security number, and filing status are the foundational elements. This identifies who is filing the return.

- Dependents: Information about any dependents you claim, such as children or other qualifying relatives, is crucial for claiming certain tax credits and deductions.

- Income: This is a major section where you report all sources of income, including wages, salaries, tips, interest, dividends, capital gains, retirement distributions, unemployment compensation, and any other taxable income.

- Adjustments to Income: Also known as “above-the-line” deductions, these reduce your adjusted gross income (AGI). Examples include contributions to traditional IRAs, student loan interest, alimony paid, and self-employment tax deductions.

- Adjusted Gross Income (AGI): This is a critical subtotal calculated by subtracting your adjustments to income from your gross income. AGI is used as a starting point for many other tax calculations.

- Deductions: You have two options for deductions: the standard deduction or itemized deductions. The standard deduction is a fixed amount that varies by filing status. Itemizing involves listing specific deductible expenses, such as mortgage interest, state and local taxes (SALT), charitable contributions, and medical expenses exceeding a certain percentage of your AGI. You choose whichever option results in a larger deduction, thereby reducing your taxable income.

- Taxable Income: This is calculated by subtracting your total deductions from your AGI. This is the amount of income on which your tax liability is calculated.

- Tax Credits: These are dollar-for-dollar reductions of your tax liability, making them generally more valuable than deductions. Common credits include the Child Tax Credit, Earned Income Tax Credit, education credits, and energy credits.

- Tax Liability: Based on your taxable income and the applicable tax brackets for your filing status, your total tax liability is calculated.

- Payments and Refunds: This section accounts for taxes already paid throughout the year, typically through withholding from paychecks or estimated tax payments. If your payments exceed your tax liability, you are due a refund. If your liability is greater than your payments, you owe additional tax.

The Role of the 1040 in Tax Planning and Compliance

Beyond its function as a reporting document, the 1040 form plays a significant role in tax planning and ensuring compliance with the U.S. tax laws. It’s not merely a record of past financial activity but a tool that can be leveraged to optimize tax outcomes.

Calculating Tax Liability and Determining Refund or Amount Due

The core purpose of the 1040 is to accurately calculate your tax liability for the year. This involves a series of steps: first, determining your gross income; second, subtracting any eligible adjustments to arrive at your Adjusted Gross Income (AGI); third, subtracting either the standard deduction or itemized deductions to arrive at your taxable income; and finally, applying the appropriate tax rates to your taxable income to determine your tax liability. Once your total tax liability is established, it’s compared against the total tax payments you’ve already made. If payments exceed liability, a refund is issued. If liability exceeds payments, you must remit the difference to the IRS by the tax deadline.

Claiming Deductions and Credits

A critical aspect of using the 1040 form effectively is the ability to claim deductions and tax credits. Deductions reduce your taxable income, thereby lowering the amount of income subject to taxation. Credits, on the other hand, directly reduce the amount of tax you owe. Understanding which deductions and credits you are eligible for is a key component of tax planning. For instance, individuals with significant medical expenses, who are homeowners with mortgage interest, or who make substantial charitable donations might benefit from itemizing their deductions. Similarly, families with children may be eligible for the Child Tax Credit, while lower-income workers might qualify for the Earned Income Tax Credit. The 1040 form provides the framework for claiming these benefits.

Record Keeping and Future Tax Strategies

The information reported on your 1040 form is essential for maintaining accurate financial records. These records serve multiple purposes, including supporting the figures reported on your return in case of an audit, and providing a historical overview of your financial activity. This historical data can be invaluable for future tax planning. By reviewing past returns, you can identify trends in your income and expenses, assess the effectiveness of your tax strategies, and anticipate future tax obligations. This proactive approach can help you make informed financial decisions throughout the year, such as adjusting your investment strategies, retirement contributions, or business expenses to optimize your tax situation.

Variations and Related Tax Forms

While the core Form 1040 is the most common, the IRS has developed various versions and accompanying schedules to accommodate different taxpayer situations. These variations ensure that the tax system can handle the diversity of financial lives and transactions.

The Different Versions of Form 1040

Over the years, the IRS has simplified and restructured the main 1040 form. While the core principles remain the same, taxpayers may encounter slightly different layouts depending on the tax year. The goal has been to make the form more user-friendly and to consolidate information that was previously spread across multiple, separate forms. The current iteration of Form 1040 is designed to be the main form, with additional schedules and forms attached as needed to report specific types of income, deductions, or credits. This approach aims to streamline the filing process for the majority of taxpayers while providing the necessary depth for more complex situations.

Common Schedules and Forms Attached to the 1040

The main Form 1040 is often accompanied by numerous schedules and other forms, each designed to report specific types of financial activity. Some of the most common include:

- Schedule 1 (Form 1040): Additional Income and Adjustments to Income. This schedule is used to report various income sources not directly listed on the main form, such as unemployment compensation, gambling winnings, and alimony received. It also details adjustments to income, like IRA deductions and student loan interest.

- Schedule 2 (Form 1040): Additional Taxes. This is where taxpayers report certain taxes that aren’t part of the regular income tax calculation, such as self-employment tax, household employment taxes, and additional taxes on retirement accounts.

- Schedule 3 (Form 1040): Additional Credits and Payments. This schedule is used to report and calculate various tax credits beyond those directly listed on the main form, such as education credits, health insurance marketplace premium tax credits, and foreign tax credits. It also accounts for certain tax payments.

- Schedule A (Form 1040): Itemized Deductions. This is the form used if you choose to itemize your deductions rather than taking the standard deduction. You report deductible medical and dental expenses, taxes you paid, interest you paid, and charitable contributions here.

- Schedule C (Form 1040): Profit or Loss From Business (Sole Proprietorship). This is essential for self-employed individuals and small business owners to report their business income and expenses.

- Schedule D (Form 1040): Capital Gains and Losses. This form is used to report the sale or exchange of capital assets, such as stocks, bonds, and real estate.

- Schedule SE (Form 1040): Self-Employment Tax. This schedule is used to calculate the self-employment tax (Social Security and Medicare taxes) for individuals who are self-employed.

The specific schedules and forms an individual needs to file depend entirely on their unique financial circumstances and the types of income earned, deductions claimed, and credits sought. The IRS provides detailed instructions for each form to help taxpayers navigate this complex landscape.

The Importance of Accuracy and Timely Filing

Ensuring the accuracy of the information provided on Form 1040 and filing it by the designated deadline are paramount. Mistakes can lead to delays in refunds, unexpected tax bills, penalties, and interest charges. Moreover, understanding the implications of your filing choices can have a long-term impact on your financial well-being.

Avoiding Errors and Penalties

Accuracy on Form 1040 is not just about avoiding penalties; it’s about ensuring you receive the correct refund or pay the accurate amount of tax owed. Common errors include miscalculating income, incorrectly applying deductions or credits, or transposing Social Security numbers. The IRS uses sophisticated computer systems to match the information reported on your return with data received from employers and financial institutions. Discrepancies can trigger inquiries or audits. Penalties can be levied for filing late, not paying taxes owed by the due date, or for underpayment of estimated tax. Interest is also charged on underpayments. Thoroughly reviewing your return before submission and using tax preparation software or consulting a tax professional can significantly reduce the risk of errors.

The Tax Deadline and Extensions

The deadline for filing federal income tax returns (Form 1040) is typically April 15th each year, unless it falls on a weekend or holiday, in which case it is the next business day. It is crucial to meet this deadline to avoid late-filing penalties and interest. If you cannot complete your return by the deadline, you can request an automatic six-month extension to file by submitting Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return. However, it’s important to note that an extension to file is not an extension to pay. You are still required to estimate your tax liability and pay any amount owed by the original April deadline to avoid penalties and interest on the unpaid portion.

The Impact of Filing Choices on Future Financial Planning

The decisions made when completing Form 1040 have ripple effects on your financial future. For example, choices regarding retirement account contributions (e.g., Traditional IRA vs. Roth IRA) impact your current taxable income and future tax-free withdrawals. Decisions about which deductions to take (standard vs. itemized) can influence your overall tax burden year after year. Understanding tax-advantaged investment vehicles and available credits can lead to significant long-term savings. By approaching the 1040 not just as a compliance obligation but as an opportunity for strategic financial management, individuals can optimize their tax situation and build a stronger financial foundation.