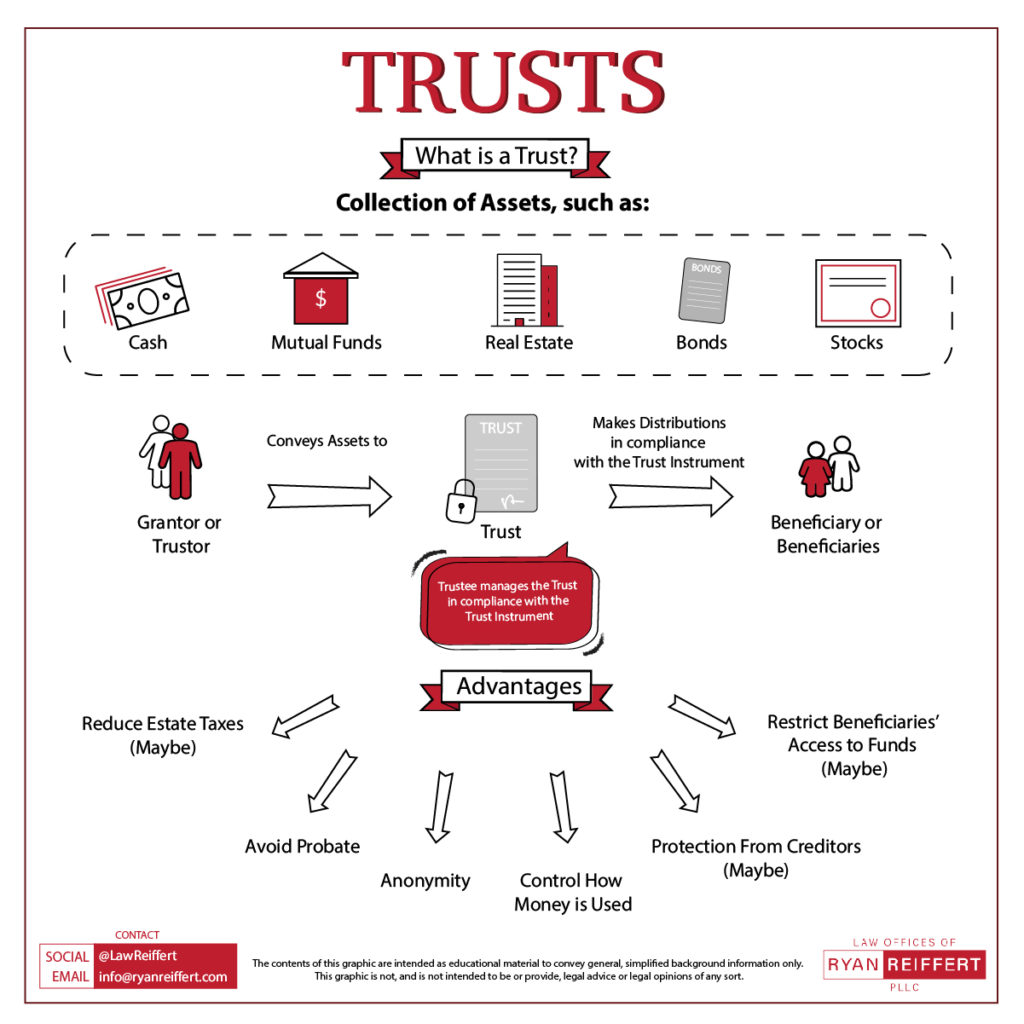

In the realm of fiduciary arrangements, understanding the distinctions between various types of trusts is paramount for effective estate planning, asset protection, and philanthropic endeavors. Trusts, at their core, are legal entities that hold assets for the benefit of designated beneficiaries, managed by a trustee. The nuances of their creation, purpose, and operational structure lead to a diverse spectrum of trust types, each serving unique objectives. This exploration delves into the fundamental categories of trusts, illuminating their defining characteristics and practical applications.

Revocable vs. Irrevocable Trusts

The primary distinction in trust classification often hinges on the grantor’s ability to modify or terminate the trust after its creation. This fundamental difference dictates the level of control the grantor retains and the implications for asset protection and tax treatment.

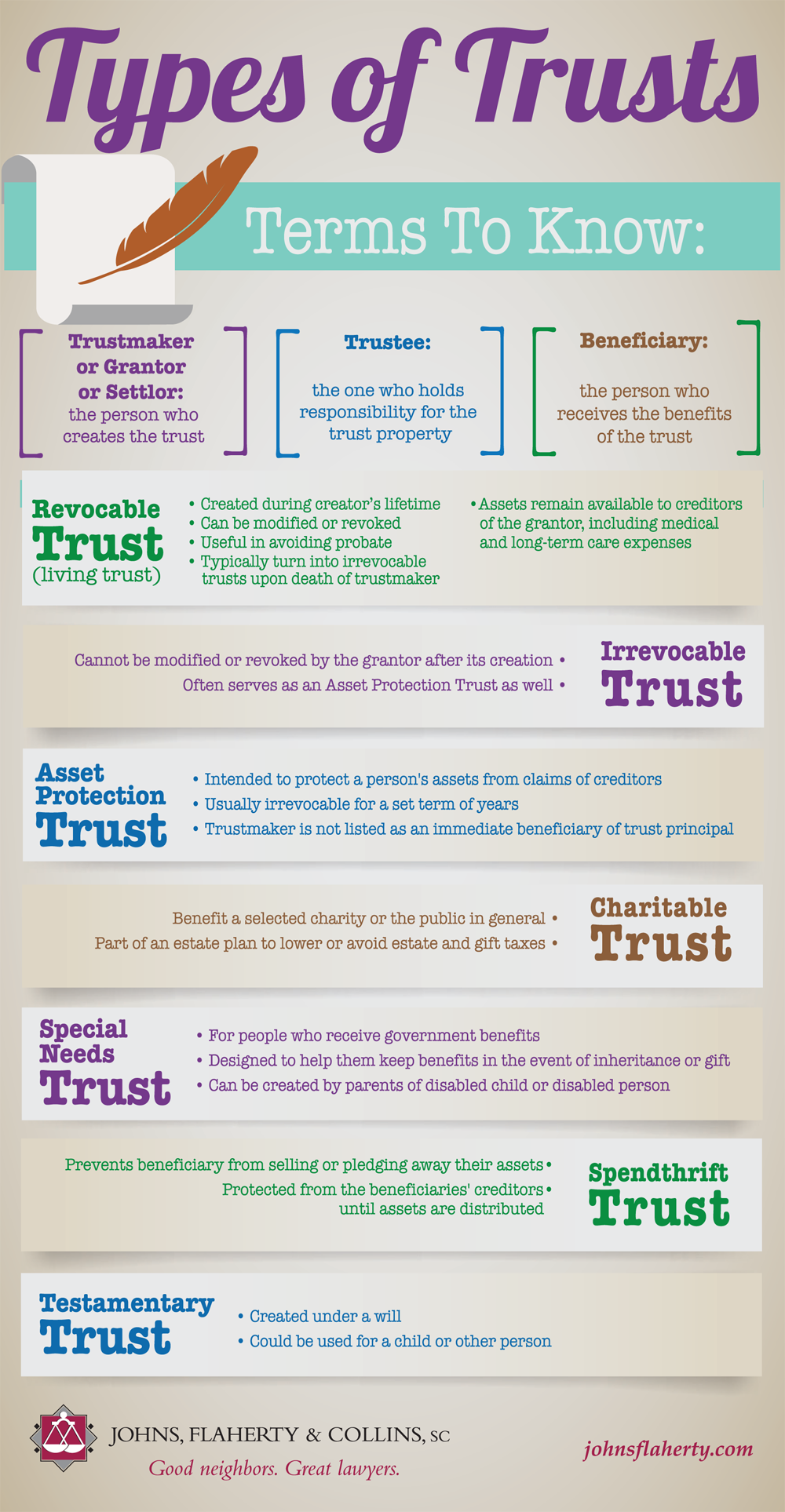

Revocable Trusts

A revocable trust, also known as a living trust, grants the grantor significant flexibility. During their lifetime, the grantor can amend, alter, or even dissolve the trust at their discretion. This means the assets held within a revocable trust are still considered the grantor’s property for tax purposes and are subject to their creditors.

Key Characteristics of Revocable Trusts:

- Flexibility: The grantor can change beneficiaries, trustees, or the terms of the trust at any time.

- Probate Avoidance: Assets held in a revocable trust bypass the probate process upon the grantor’s death, leading to a faster and more private distribution of assets to beneficiaries.

- Management During Incapacity: A revocable trust can designate a successor trustee to manage the assets if the grantor becomes incapacitated, ensuring seamless financial management without court intervention.

- No Asset Protection: Because the grantor retains control, assets in a revocable trust are not protected from the grantor’s creditors during their lifetime.

- No Immediate Tax Benefits: The grantor typically pays income tax on earnings generated by the trust assets, and the assets are included in the grantor’s taxable estate.

Common Uses for Revocable Trusts:

Revocable trusts are frequently employed for straightforward estate planning, particularly for individuals who wish to avoid probate and maintain control over their assets during their lifetime. They are also beneficial for individuals who own property in multiple states, as it can simplify the transfer of those properties upon death.

Irrevocable Trusts

In contrast, an irrevocable trust is a trust that, once established, cannot be easily amended, revoked, or altered by the grantor. The grantor relinquishes significant control over the assets transferred into the trust, and in return, may gain substantial benefits in terms of asset protection and tax reduction.

Key Characteristics of Irrevocable Trusts:

- Permanence: The terms of an irrevocable trust are generally fixed, although specific provisions may allow for limited modifications under certain circumstances with court or beneficiary consent.

- Asset Protection: Assets transferred to an irrevocable trust are typically shielded from the grantor’s creditors, as the grantor no longer owns or controls them.

- Estate Tax Reduction: Assets placed in an irrevocable trust are generally removed from the grantor’s taxable estate, potentially reducing estate tax liabilities.

- Gift Tax Considerations: Transferring assets to an irrevocable trust may trigger gift tax implications, depending on the value of the assets and the grantor’s lifetime gift tax exemption.

- Trustee Independence: The trustee of an irrevocable trust operates with a degree of independence, bound by the trust document to act in the best interest of the beneficiaries.

Common Uses for Irrevocable Trusts:

Irrevocable trusts are often utilized for more complex estate planning goals, including:

- Charitable Giving: Charitable remainder trusts and charitable lead trusts allow for philanthropic contributions while providing income to beneficiaries or the grantor.

- Life Insurance Trusts: An irrevocable life insurance trust (ILIT) can hold life insurance policies, keeping the death benefit out of the grantor’s taxable estate.

- Medicaid Planning: Certain irrevocable trusts can be structured to protect assets from being counted towards Medicaid eligibility requirements.

- Special Needs Trusts: These trusts provide for the financial needs of a disabled individual without jeopardizing their eligibility for government benefits.

Testamentary vs. Living Trusts

Another significant classification distinguishes trusts based on when they become effective: either during the grantor’s lifetime or upon their death.

Living Trusts (Inter Vivos Trusts)

As previously discussed in the context of revocable trusts, living trusts are established and funded during the grantor’s lifetime. The term “living trust” is often used interchangeably with “revocable trust,” though technically, an irrevocable trust can also be a living trust if established during the grantor’s life. The primary benefit is their immediate effect and ability to manage assets while the grantor is alive, and to avoid probate upon death.

Testamentary Trusts

A testamentary trust is created through a will and only comes into existence after the grantor’s death and after the will has gone through the probate process. The terms of the trust are outlined in the will, and the appointed trustee is then responsible for establishing and administering the trust according to those instructions.

Key Characteristics of Testamentary Trusts:

- Delayed Creation: The trust does not exist until the grantor’s death and the probate of their will.

- Probate Requirement: Assets intended for a testamentary trust must go through probate, which can be a lengthy and public process.

- Flexibility in Creation: A will is generally easier to change than a living trust, allowing for amendments to the trust’s terms before the grantor’s death.

- Less Privacy: Because they are part of a probated will, the terms of a testamentary trust are publicly accessible.

- No Management During Incapacity: A testamentary trust cannot provide for asset management during the grantor’s lifetime or in case of incapacity.

Common Uses for Testamentary Trusts:

Testamentary trusts are often used when:

- The grantor wishes to maintain flexibility in their estate plan until death.

- The primary goal is to control the distribution of assets after death, perhaps for minor children or beneficiaries who may not be financially responsible.

- The grantor wants to defer the costs and complexities of establishing a living trust during their lifetime.

Other Important Trust Classifications

Beyond the primary distinctions of revocability and timing, trusts can be further categorized based on their specific purpose and structure.

Charitable Trusts

Charitable trusts are established for philanthropic purposes, with the assets dedicated to charitable organizations or causes. They can take various forms, such as:

- Charitable Remainder Trust (CRT): Allows the grantor or other beneficiaries to receive an income stream for a set period or their lifetime, with the remaining assets passing to a designated charity.

- Charitable Lead Trust (CLT): Provides income to a charity for a specified term, after which the remaining assets revert to the grantor or other non-charitable beneficiaries.

Special Needs Trusts (Supplemental Needs Trusts)

Designed to benefit individuals with disabilities, special needs trusts allow for the provision of funds for their care and well-being without disqualifying them from essential government benefits like Supplemental Security Income (SSI) and Medicaid.

Spendthrift Trusts

A spendthrift trust is designed to protect a beneficiary’s inheritance from their own creditors or impulsive spending habits. The trust agreement typically restricts the beneficiary’s access to the principal, and payments are made directly to the beneficiary or for specific expenses.

Bypass Trusts (Bypass Trust, Credit Shelter Trust, A/B Trust)

These trusts are often used in estate planning for married couples to minimize estate taxes. Upon the death of the first spouse, assets are passed into a trust that may not be taxed in their estate. When the second spouse dies, the assets can then pass to beneficiaries without incurring further estate taxes, effectively “bypassing” the surviving spouse’s taxable estate.

Irrevocable Life Insurance Trusts (ILITs)

As mentioned earlier, ILITs are irrevocable trusts specifically designed to hold life insurance policies. By transferring ownership of the policy to the ILIT, the death benefit can be excluded from the grantor’s taxable estate, providing a tax-efficient way to pass wealth to beneficiaries.

Qualified Personal Residence Trusts (QPRTs)

A QPRT allows a grantor to transfer their primary or secondary residence to an irrevocable trust, retaining the right to live in the home for a specified number of years. After this term, ownership of the home passes to the beneficiaries, and the value transferred is discounted, potentially reducing gift tax.

Blind Trusts

In a blind trust, the trustee has complete control over the management and investment of the trust assets, with no knowledge on the part of the grantor or beneficiaries regarding the specific holdings. This is often used by individuals in positions of potential conflict of interest, such as public officials or corporate executives, to ensure impartiality.

Conclusion

The landscape of trusts is multifaceted, offering a sophisticated array of tools for managing wealth, protecting assets, and fulfilling philanthropic aspirations. Whether opting for the flexibility of a revocable living trust or the asset protection of an irrevocable arrangement, understanding the unique characteristics and implications of each trust type is crucial. Careful consideration, often with the guidance of experienced legal and financial professionals, ensures that the chosen trust structure aligns precisely with individual goals and provides the intended benefits for years to come. The strategic use of these legal instruments allows for a more controlled, efficient, and secure transfer of wealth and can offer peace of mind in navigating the complexities of financial legacy.