In the realm of accounting, particularly for businesses that extend credit to customers, the concept of “Allowance for Bad Debts” is a crucial one. It directly impacts a company’s financial statements, specifically its reported revenue and asset values. Understanding its classification is fundamental to grasping the nuances of financial reporting and the management of accounts receivable. This allowance is not a tangible asset, nor is it a direct expense in the same way as operational costs. Instead, it falls into a specific category that reflects an estimation of future uncollectible amounts, playing a vital role in presenting a true and fair view of a company’s financial health.

The Nature of Allowance for Bad Debts

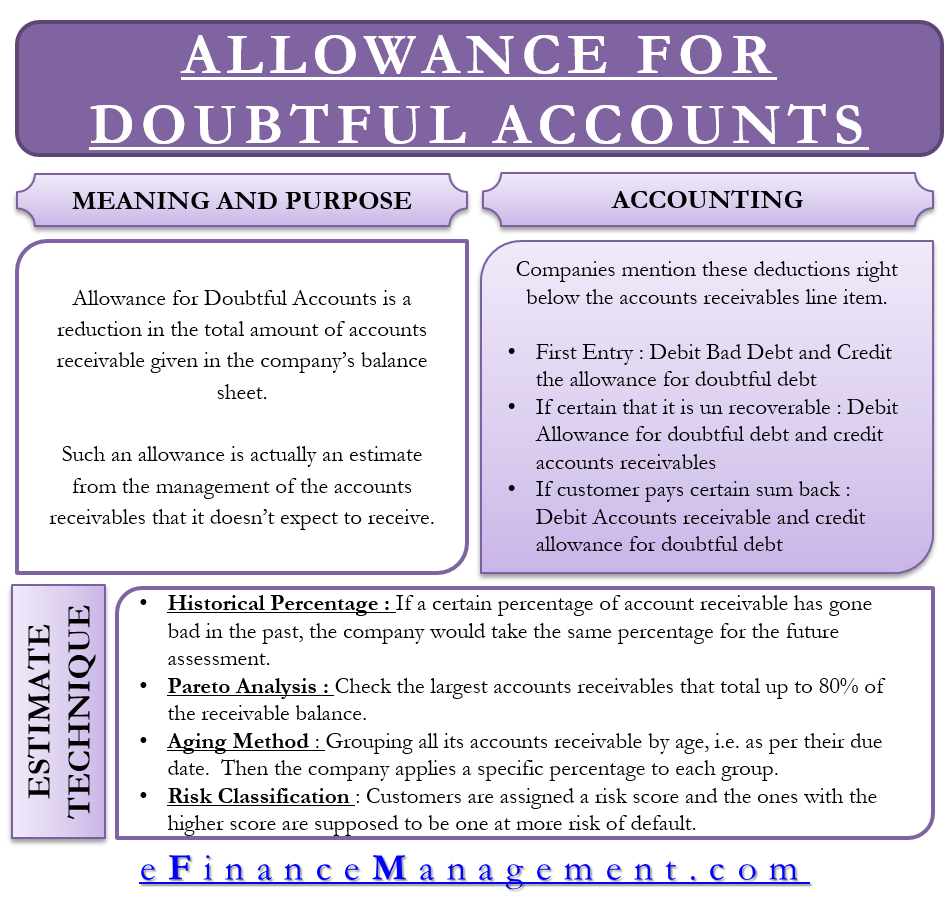

At its core, the Allowance for Bad Debts represents an estimate of the portion of a company’s accounts receivable that is expected to be uncollectible. When a business sells goods or services on credit, it creates an account receivable. This is an asset because it represents money that the customer owes to the business. However, experience and historical data often indicate that not all customers will pay their debts. The Allowance for Bad Debts is established to proactively account for these potential losses. It is a contra-asset account, meaning it reduces the carrying value of the related asset account, which is Accounts Receivable.

Contra-Asset Accounts Explained

Contra-asset accounts are accounts that reduce the balance of another asset account. They have the opposite normal balance of the asset they are paired with. Since assets typically have a debit balance, contra-asset accounts have a credit balance. For example, Accumulated Depreciation is a contra-asset account that reduces the book value of Property, Plant, and Equipment. Similarly, Allowance for Bad Debts reduces the net realizable value of Accounts Receivable. This accounting treatment ensures that the reported value of accounts receivable on the balance sheet reflects the amount the company realistically expects to collect, rather than the gross amount owed by customers.

Why is an Allowance Necessary?

The necessity of an Allowance for Bad Debts stems from the matching principle in accrual accounting. This principle dictates that expenses should be recognized in the same period as the revenues they help to generate. When a sale on credit is made, revenue is recognized. If some of those credit sales are later deemed uncollectible, the expense associated with that uncollectible revenue should also be recognized in the period of the sale, not when the specific debt is identified as bad. The Allowance for Bad Debts allows for this matching by estimating and recognizing the potential expense (Bad Debt Expense) in the same period the revenue is earned.

Classification on the Balance Sheet

The Allowance for Bad Debts is classified as a contra-asset account on the balance sheet. It is presented on the asset side of the balance sheet, but it has a credit balance. This credit balance serves to offset the debit balance of the gross Accounts Receivable. The net amount shown on the balance sheet for Accounts Receivable is therefore the gross amount less the Allowance for Bad Debts. This net amount is often referred to as the “net realizable value” of accounts receivable, representing the amount that the company anticipates it will actually collect.

Presentation on the Balance Sheet

Consider a company with $100,000 in gross Accounts Receivable. If, based on historical data and current economic conditions, the company estimates that $5,000 of these receivables will be uncollectible, it would establish an Allowance for Bad Debts of $5,000. On the balance sheet, this would be presented as:

Current Assets:

Accounts Receivable, gross $100,000

Less: Allowance for Bad Debts (5,000)

Net Accounts Receivable $95,000

This presentation clearly distinguishes between the total amount customers owe and the amount the company expects to recover, providing a more realistic picture of the company’s liquidity and asset valuation.

Importance of Net Realizable Value

The net realizable value of accounts receivable is a critical metric for assessing a company’s financial health. A significantly high Allowance for Bad Debts relative to gross Accounts Receivable could indicate poor credit policies, economic distress among customers, or ineffective collection efforts. Conversely, a very low allowance might suggest an overly optimistic assessment of collectibility, which could lead to overstated asset values and, consequently, misleading profitability.

Treatment on the Income Statement

While the Allowance for Bad Debts itself is a balance sheet account, its establishment and adjustments have a direct impact on the income statement. The expense recognized to create or increase the allowance is called Bad Debt Expense. This expense is typically classified as an operating expense, often falling under selling, general, and administrative (SG&A) expenses.

The Bad Debt Expense Entry

When the Allowance for Bad Debts is initially established or increased, the accounting entry typically involves a debit to Bad Debt Expense and a credit to Allowance for Bad Debts.

Example Entry:

Debit: Bad Debt Expense $5,000

Credit: Allowance for Bad Debts $5,000

This entry reflects the recognition of the cost of extending credit, acknowledging that some sales on credit will not result in cash inflow. It aligns with the matching principle by recognizing this expense in the same period as the related sales revenue.

Methods of Estimating Bad Debts

There are two primary methods used to estimate bad debts:

1. The Percentage of Sales Method

This method involves estimating bad debt expense based on a company’s historical percentage of credit sales that have resulted in bad debts. This percentage is applied to the current period’s credit sales to determine the Bad Debt Expense. The Allowance for Bad Debts is then adjusted to reach a balance that reflects this calculated expense.

Formula: Bad Debt Expense = Credit Sales x Estimated Bad Debt Percentage

2. The Aging of Receivables Method

This method involves analyzing the accounts receivable based on how long they have been outstanding. Older receivables are considered more likely to be uncollectible. Each age category is assigned a percentage of uncollectibility, and the total estimated uncollectible amount is calculated by summing the uncollectible amounts for each category. This method directly estimates the required balance in the Allowance for Bad Debts account. The Bad Debt Expense is then calculated as the amount needed to bring the Allowance for Bad Debts account to this required balance.

Process:

- Categorize outstanding invoices by age (e.g., 0-30 days, 31-60 days, 61-90 days, 90+ days).

- Assign an estimated percentage of uncollectibility to each age category.

- Multiply the total amount in each category by its assigned percentage to calculate the estimated uncollectible amount for that category.

- Sum these amounts to arrive at the total estimated uncollectible receivables, which is the desired ending balance for the Allowance for Bad Debts.

- Calculate Bad Debt Expense as the difference between this desired ending balance and the existing credit (or debit) balance in the Allowance for Bad Debts account.

Recoveries of Previously Written-Off Debts

Occasionally, a debt that was previously written off as uncollectible may be recovered. In such cases, two entries are typically made: first, to reinstate the receivable that was written off, and second, to record the cash collection.

Entry 1 (Reinstatement):

Debit: Accounts Receivable

Credit: Allowance for Bad Debts

Entry 2 (Collection):

Debit: Cash

Credit: Accounts Receivable

This process ensures that both the Allowance for Bad Debts and Accounts Receivable are accurately reflected for the period the recovery occurs.

Accounting for Write-Offs

When a specific account receivable is deemed definitively uncollectible, it is “written off.” This involves reducing both the gross Accounts Receivable and the Allowance for Bad Debts. It is important to note that writing off a specific account does not impact Bad Debt Expense or net income at the time of the write-off, as the expense was already recognized when the allowance was initially established.

The Write-Off Entry

The accounting entry to write off a specific uncollectible account is:

Debit: Allowance for Bad Debts

Credit: Accounts Receivable

This entry removes the specific uncollectible balance from the gross Accounts Receivable and reduces the Allowance for Bad Debts by the same amount. The net realizable value of accounts receivable remains unchanged by this specific entry.

Example: If XYZ Corp. owes $1,000 and is deemed uncollectible, and the Allowance for Bad Debts has a balance of $5,000, the write-off entry would be:

Debit: Allowance for Bad Debts $1,000

Credit: Accounts Receivable (XYZ Corp.) $1,000

After this entry, the Allowance for Bad Debts would have a remaining balance of $4,000, and Accounts Receivable would be reduced by $1,000. The net realizable value is preserved.

Significance and Impact on Financial Reporting

The Allowance for Bad Debts plays a critical role in ensuring the accuracy and reliability of a company’s financial statements. Its proper accounting and reporting contribute to:

True and Fair View of Assets

By reducing gross Accounts Receivable by the estimated uncollectible amount, the balance sheet presents a more realistic and conservative value of the assets that are expected to convert into cash. This avoids overstating the company’s financial position.

Accurate Revenue Recognition

The matching principle, facilitated by the Allowance for Bad Debts, ensures that the expense associated with uncollectible credit sales is recognized in the same period as the revenue generated from those sales. This leads to a more accurate depiction of profitability in each accounting period.

Investor and Creditor Confidence

Investors and creditors rely on financial statements to make informed decisions. A well-managed Allowance for Bad Debts signals to stakeholders that the company is prudently managing its credit risks and providing transparent financial reporting. It demonstrates an understanding that not all sales are ultimately collected and that this risk is being proactively accounted for.

Management Decision-Making

The process of estimating and managing the Allowance for Bad Debts provides valuable insights for management. Analyzing the effectiveness of credit policies, collection procedures, and the overall economic climate of the customer base becomes more informed. Trends in bad debt write-offs and the adequacy of the allowance can prompt adjustments to credit terms, collection strategies, or even pricing.

In conclusion, the Allowance for Bad Debts is a crucial accounting mechanism that serves as a contra-asset account on the balance sheet and is directly linked to Bad Debt Expense on the income statement. Its primary purpose is to provide a realistic valuation of accounts receivable by accounting for potential uncollectible amounts, thereby ensuring that financial statements present a true and fair view of a company’s financial position and performance.