VUL life insurance, or Variable Universal Life insurance, is a sophisticated and flexible type of permanent life insurance that offers policyholders the potential for cash value growth linked to investment sub-accounts. Unlike traditional whole life policies, VUL allows for a degree of control over how the policy’s cash value is invested, providing an opportunity to accumulate wealth over time. This dual benefit of a death benefit and investment potential makes VUL an attractive option for individuals seeking a comprehensive financial planning tool.

At its core, VUL is a form of universal life insurance, which itself is a type of permanent life insurance designed to provide coverage for the entire lifetime of the insured, as long as premiums are paid. Universal life policies offer flexibility in premium payments and death benefit amounts. The “variable” component of VUL introduces an investment dimension, where a portion of the premium paid goes towards the death benefit, and another portion is invested in a selection of sub-accounts, similar to mutual funds.

Understanding the mechanics of VUL requires delving into its key features: the death benefit, the cash value, and the investment component. The death benefit is the tax-free lump sum amount paid to the designated beneficiaries upon the insured’s death. The cash value is the portion of the premium that grows over time on a tax-deferred basis, influenced by the performance of the chosen investments. This cash value can be accessed by the policyholder during their lifetime through loans or withdrawals, though doing so can impact the death benefit.

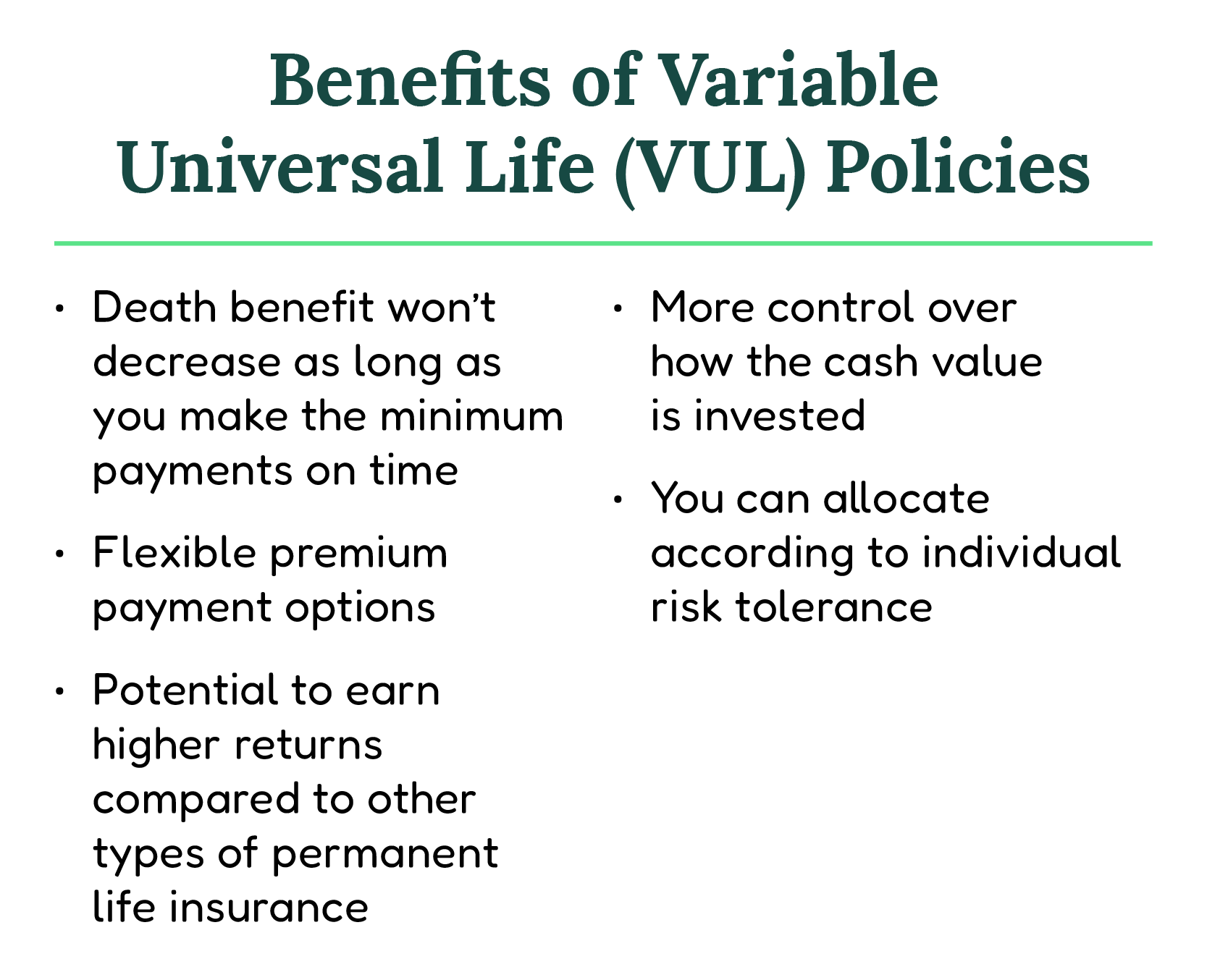

The flexibility inherent in VUL is one of its most significant advantages. Policyholders can often adjust the premium payments within certain limits, either increasing or decreasing them, as their financial circumstances change. Similarly, the death benefit can also be adjusted, allowing for modifications to suit evolving needs. This adaptability is a departure from the fixed premiums and death benefits of traditional whole life insurance.

However, this flexibility comes with inherent risks and complexities. The investment component means that the cash value is subject to market fluctuations. If the chosen sub-accounts perform poorly, the cash value can decline, potentially impacting the policy’s ability to remain in force without additional premium payments. Conversely, strong market performance can lead to significant cash value growth.

The Dual Nature of VUL: Protection and Investment

Variable Universal Life insurance is fundamentally designed to serve two primary purposes: to provide a death benefit that financially protects beneficiaries and to offer a vehicle for cash value accumulation through investment. This dual nature distinguishes it from term life insurance, which offers protection only, and from traditional whole life insurance, which typically offers a guaranteed, albeit lower, rate of return on cash value.

The Death Benefit: Lifelong Protection

The death benefit in a VUL policy serves the paramount purpose of life insurance: to provide financial security for loved ones upon the insured’s passing. This benefit is typically paid out tax-free to the beneficiaries, offering them a crucial financial cushion during a difficult time. The amount of the death benefit can be structured in various ways. Many VUL policies offer two death benefit options:

- Option A (Level Death Benefit): This option provides a death benefit that remains level throughout the life of the policy. For example, if the policy has a death benefit of $500,000, this amount will remain constant. In this scenario, the cash value grows independently of the death benefit. If the cash value grows substantially, the death benefit may be reduced by the amount of the outstanding loans or withdrawals taken against the cash value.

- Option B (Increasing Death Benefit): This option provides a death benefit that is equal to the face amount of the policy plus the accumulated cash value. This means the total payout to beneficiaries will increase as the cash value grows. This option generally results in higher policy costs due to the increased insurance risk.

The choice between these options depends on the policyholder’s objectives. Option A might be preferred if the primary goal is to maximize the amount available for investment growth. Option B might be chosen if the intention is to ensure that beneficiaries receive both the guaranteed death benefit and any accumulated cash value, providing a larger potential payout.

The Cash Value: A Growing Asset

The cash value component is where the “variable” aspect of VUL truly shines. A portion of each premium payment, after deducting policy charges, is allocated to investment sub-accounts chosen by the policyholder. These sub-accounts are typically similar to mutual funds and can include a variety of asset classes, such as stocks, bonds, and money market funds.

The growth of the cash value is directly tied to the performance of these chosen investments. If the markets perform well, the cash value can grow significantly, potentially outpacing inflation and the returns offered by traditional whole life insurance policies. This growth occurs on a tax-deferred basis, meaning that policyholders do not pay taxes on any earnings until they withdraw the funds or surrender the policy.

Policyholders have a considerable degree of control over how their cash value is invested. They can select from a range of investment options provided by the insurance company, diversifying their portfolio across different asset classes and risk levels. This allows for a personalized investment strategy aligned with individual risk tolerance and financial goals. Furthermore, most VUL policies allow for the reallocation of funds between sub-accounts, enabling policyholders to adjust their investment strategy as market conditions change or their objectives evolve.

It is crucial to understand that the cash value is not guaranteed. While the potential for growth is attractive, it also carries the risk of loss if the underlying investments perform poorly. This is a key differentiator from fixed-rate policies or traditional whole life insurance, where cash value growth is guaranteed at a predetermined rate.

Flexibility and Control: Managing Your Policy

One of the most compelling features of Variable Universal Life insurance is its inherent flexibility, allowing policyholders to adapt their coverage and premium payments to meet changing life circumstances and financial goals. This adaptability is a cornerstone of the universal life design and is further enhanced by the investment choices available in VUL.

Premium Payment Flexibility

Unlike the rigid premium schedules of traditional whole life insurance, VUL policies offer considerable flexibility in how and when premiums are paid. Within the guidelines set by the insurance company, policyholders can:

- Adjust Premium Amounts: Policyholders can choose to pay more than the minimum required premium to accelerate cash value growth or less if facing temporary financial constraints. However, it’s essential to understand that paying less than the target premium can impact the policy’s duration and death benefit. Insufficient premium payments can lead to the policy lapsing if the cash value is not sufficient to cover policy charges.

- Skip Premiums: In certain situations, policyholders may be able to skip premium payments, provided that there is enough accumulated cash value to cover the policy’s ongoing costs, such as the cost of insurance and administrative fees. This feature offers a valuable safety net during periods of financial hardship.

- Timing of Payments: Universal life policies typically allow for more flexibility in the timing of premium payments, offering a broader window compared to fixed schedules.

This flexibility empowers policyholders to manage their VUL policies in alignment with their evolving financial situations, making it a more adaptable long-term financial planning tool.

Death Benefit Adjustments

The death benefit amount in a VUL policy can also be adjusted, providing another layer of flexibility. Policyholders may have the option to:

- Increase the Death Benefit: If financial needs increase, such as having more children or taking on greater financial responsibilities, the death benefit can often be increased. This typically requires a new underwriting process and may involve additional costs.

- Decrease the Death Benefit: If financial responsibilities decrease or the need for a large death benefit diminishes, the death benefit amount can sometimes be reduced. This can lead to lower policy charges and potentially faster cash value growth.

The ability to adjust the death benefit ensures that the VUL policy remains relevant to the policyholder’s needs throughout their life, preventing it from becoming an outdated or excessive financial commitment.

Investment Allocation and Rebalancing

The “variable” aspect of VUL empowers policyholders with the control to actively manage their investment portfolio. This includes:

- Sub-Account Selection: Policyholders can choose from a diverse range of investment sub-accounts offered by the insurer. These often mirror mutual fund offerings and span various investment categories like equities, fixed income, and money markets, allowing for diversification across different risk profiles and asset classes.

- Portfolio Allocation: The policyholder decides how to allocate their premium payments and existing cash value across these chosen sub-accounts. This allows for the creation of a portfolio tailored to their individual risk tolerance, investment horizon, and financial objectives.

- Rebalancing and Fund Transfers: VUL policies typically permit policyholders to rebalance their portfolios or transfer funds between sub-accounts. This is a crucial feature for adapting to changing market conditions, adjusting risk levels, or capitalizing on new investment opportunities. For example, as retirement approaches, a policyholder might shift funds from more aggressive equity sub-accounts to more conservative bond or money market options.

This active management of investments is a key differentiator of VUL and requires a degree of financial acumen and a willingness to monitor market performance.

Understanding the Costs and Risks

While Variable Universal Life insurance offers significant advantages in terms of flexibility and potential cash value growth, it is essential for policyholders to be fully aware of the associated costs and inherent risks. These factors can significantly influence the policy’s performance and its long-term viability.

Policy Charges and Fees

VUL policies come with a multifaceted fee structure that can impact the net growth of the cash value. These charges are generally higher than those associated with traditional whole life or term life insurance policies. Key charges include:

- Cost of Insurance: This is the premium paid for the death benefit coverage itself. It is influenced by the insured’s age, health, gender, and the chosen death benefit amount. The cost of insurance typically increases with age.

- Administrative Fees: These fees cover the operational costs of managing the policy, such as record-keeping, customer service, and premium processing.

- Surrender Charges: If a policy is surrendered or significantly reduced within the early years, a surrender charge may apply. These charges are designed to recoup the acquisition costs incurred by the insurer.

- Investment Management Fees (for Sub-accounts): Each investment sub-account has its own management fee, similar to mutual fund expense ratios, which is deducted from the investment’s performance.

- Mortality and Expense (M&E) Charges: These are charges levied by the insurance company to cover the costs associated with providing insurance and to cover potential future claims exceeding premiums collected.

These charges are deducted from the premium payments and the cash value, meaning that a portion of the money paid into the policy does not directly contribute to investment growth. Understanding the total impact of these fees is critical for projecting the policy’s performance.

Investment Risks and Market Volatility

The defining characteristic of VUL is its investment component, which also introduces its most significant risk: market volatility. The cash value is directly linked to the performance of the chosen investment sub-accounts.

- Market Fluctuations: If the chosen sub-accounts experience downturns, the cash value can decline. In severe market conditions, the cash value could potentially fall below the amount needed to cover the policy’s expenses.

- Loss of Value: Unlike policies with guaranteed cash value growth, VUL cash value is not protected from market losses. If the investment performance is consistently poor, the policy’s cash value may not grow as anticipated, or it could even diminish.

- Impact on Policy Lapse: If the cash value depreciates significantly and is insufficient to cover the policy charges, the policyholder may need to pay additional premiums to keep the policy in force. Failure to do so could result in the policy lapsing, meaning the death benefit is lost, and any accumulated cash value beyond the surrender value may be forfeited.

Policyholders must have a strong understanding of their risk tolerance and the investment options available. Diversification across different sub-accounts can help mitigate some of the risk, but it does not eliminate the possibility of losses.

Tax Implications and Policy Lapse

While VUL offers tax-deferred growth on its cash value, there are tax considerations to be aware of, particularly when accessing the cash value or in the event of a policy lapse.

- Withdrawals and Loans: Withdrawals from the cash value are generally considered taxable income to the extent that they exceed the premiums paid. Loans taken against the cash value are not taxed at the time of the loan, but they reduce the death benefit, and if the policy lapses while there is an outstanding loan, the loan amount could be considered a taxable event.

- Policy Lapse: A policy lapse can have significant tax consequences. If the policy lapses with an outstanding loan, the loan balance may be treated as taxable income. Furthermore, if the cash surrender value exceeds the total premiums paid, that excess may also be subject to taxation.

Careful planning and monitoring of the policy’s performance are essential to avoid adverse tax outcomes and to ensure the policy remains in force to provide the intended lifelong protection and wealth accumulation benefits.