Endorsing a check is a critical step in the financial transaction process, allowing for the transfer of ownership and the ability to deposit or cash a check. While seemingly straightforward, understanding the nuances of endorsement is essential for both individuals and businesses to avoid potential issues and ensure smooth financial dealings. This article delves into the various aspects of check endorsement, from its fundamental purpose to different types of endorsements and best practices.

The Fundamental Purpose of Check Endorsement

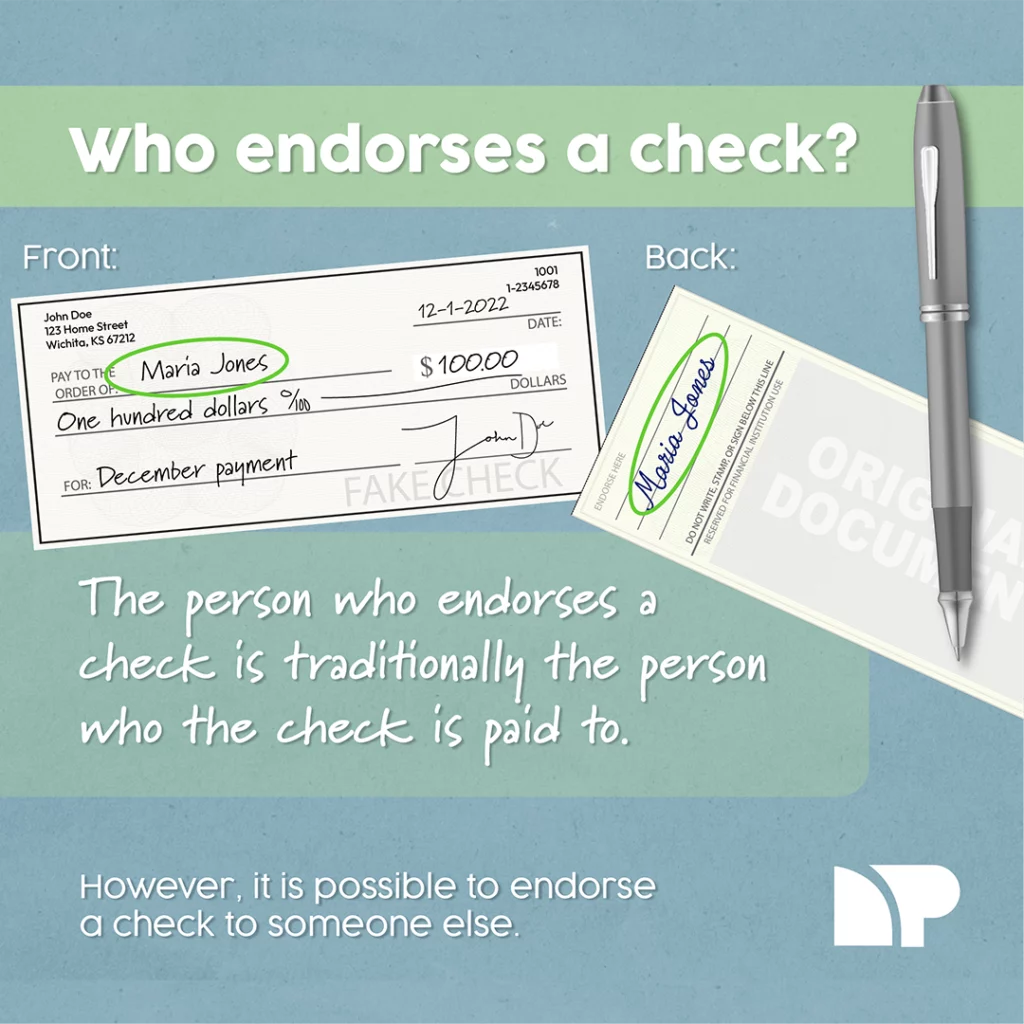

At its core, endorsing a check is a signature on the back of the instrument that validates the transfer of rights and responsibilities associated with that check. When a check is written to a specific payee, only that payee has the legal authority to receive the funds. The endorsement serves as the payee’s official acknowledgment and authorization for the check to be processed. Without a proper endorsement, a bank will likely refuse to honor the check, regardless of whether the funds are available.

Transfer of Ownership

The primary function of an endorsement is to transfer ownership of the check. Imagine you receive a check but cannot deposit it yourself for some reason. You might want to give it to a friend or family member to deposit on your behalf. By endorsing the check, you legally transfer your right to the funds to that individual. This is where different types of endorsements become crucial, as they dictate the extent of this transfer.

Authorization for Deposit or Cashing

Once endorsed, the check becomes negotiable. This means it can be deposited into a bank account or, in some cases, cashed directly. The endorsement signals to the bank that the individual presenting the check is the rightful owner or has been authorized by the rightful owner to receive the funds. Banks rely on these endorsements to maintain accurate records and prevent fraudulent transactions.

Legal and Contractual Obligation

Endorsing a check also carries a degree of legal and contractual obligation. By signing, the endorser is essentially guaranteeing that the check is valid and that they have the right to transfer it. If the check later turns out to be fraudulent or if there are insufficient funds (resulting in a bounced check), the endorser may, under certain circumstances, be held liable for the amount of the check. This underscores the importance of endorsing checks only when you are certain of the transaction’s legitimacy and your own rights to the funds.

Types of Check Endorsements

The way a check is endorsed significantly impacts who can claim the funds and under what conditions. Understanding these different types is crucial for managing your finances effectively and securely.

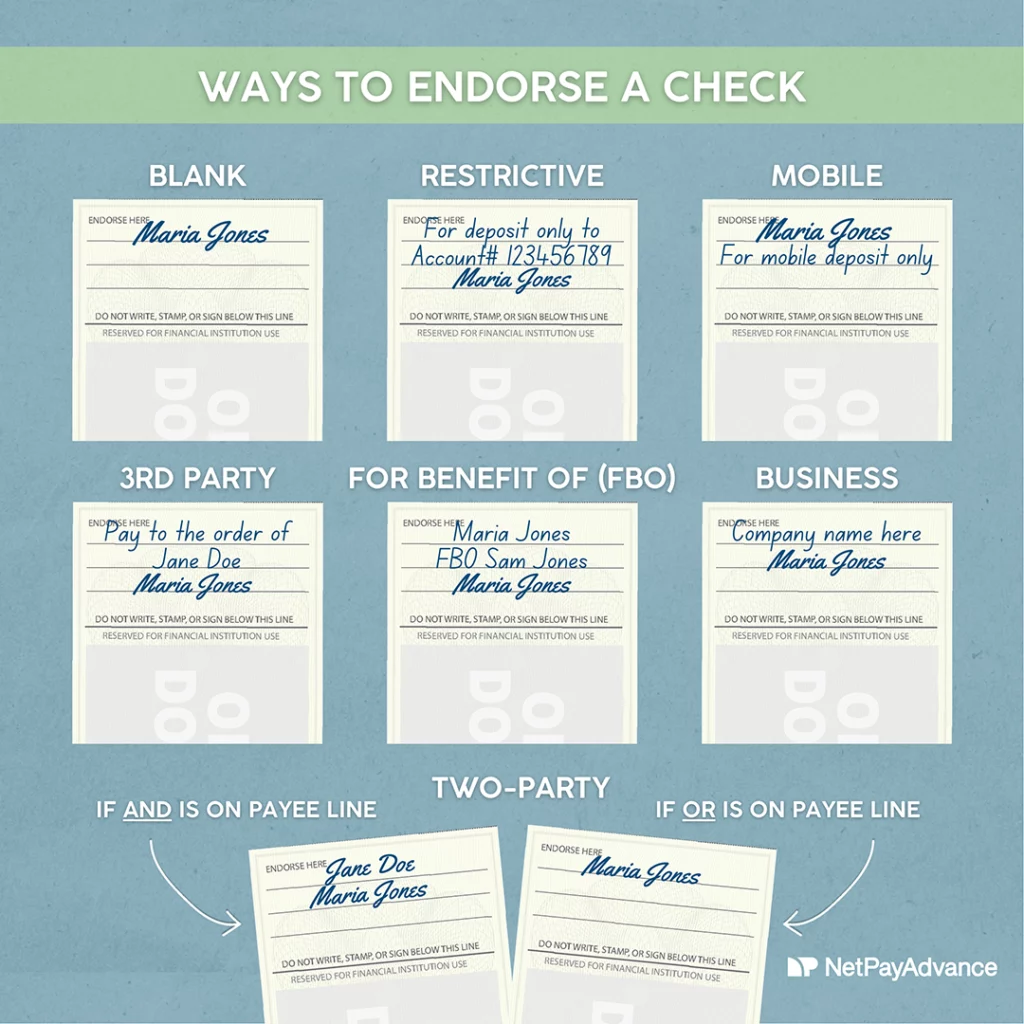

Blank Endorsement

A blank endorsement is the simplest form of endorsement. It involves simply signing your name on the back of the check, exactly as it appears on the “Pay to the order of” line.

How it Works:

When you endorse a check with a blank endorsement, you effectively turn it into a bearer instrument. This means whoever possesses the check can cash or deposit it.

Implications:

- Security Risk: Blank endorsements are generally not recommended for security reasons. If you lose a check with a blank endorsement, anyone who finds it can claim the funds.

- Convenience: They offer convenience if you intend for someone else to cash or deposit the check for you immediately, and you trust them implicitly. However, the risk often outweighs the convenience.

Special Endorsement (Full Endorsement)

A special endorsement, also known as a full endorsement, is a more secure method. It specifies exactly who the check is being transferred to.

How it Works:

To create a special endorsement, you first write “Pay to the order of [New Payee’s Name]” above your signature. Then, you sign your name below that. For example, if your name is Jane Doe and you want to endorse the check to John Smith, you would write:

“Pay to the order of John Smith”

Jane Doe

Implications:

- Enhanced Security: This method restricts the transfer of the check. Only the named new payee (John Smith in the example) can then endorse and deposit or cash the check.

- Clear Audit Trail: It provides a clear record of the transfer of ownership, which can be valuable for accounting and dispute resolution.

Restrictive Endorsement

A restrictive endorsement limits how the check can be used. It’s often used to ensure that funds are deposited into a specific account or for a particular purpose.

How it Works:

The most common restrictive endorsement is “For Deposit Only.” This is typically accompanied by your account number.

Example:

“For Deposit Only”

Account #123456789

Jane Doe

Implications:

- Prevents Cashing: A check endorsed “For Deposit Only” cannot be cashed directly at a bank teller. It must be deposited into the account specified by the endorser.

- Increased Safety: This significantly reduces the risk of loss or theft, as the funds can only be deposited, not withdrawn directly. It’s highly recommended for checks you are mailing to your bank or a third party for deposit.

- Other Restrictions: While “For Deposit Only” is most common, you could, in theory, add other restrictions, though these are less commonly used and may require bank clarification for acceptance.

Qualified Endorsement

A qualified endorsement is less common and is used to limit the endorser’s liability. It often includes phrases like “Without Recourse.”

How it Works:

When you endorse a check “Without Recourse,” you are stating that you are transferring your rights to the check but are not guaranteeing its payment.

Example:

“Without Recourse”

Jane Doe

Implications:

- Limited Liability: If the check bounces or is otherwise uncollectible, the person who received the check from you (and who is now the holder) cannot pursue you for the money. The risk shifts entirely to the new holder.

- Rarely Used by Individuals: This type of endorsement is more common in business transactions, such as when a business sells a note or debt to another entity and wants to disclaim responsibility if the underlying obligation isn’t met.

Best Practices for Endorsing Checks

To ensure your financial transactions are secure and efficient, adhering to certain best practices when endorsing checks is crucial.

Endorse Immediately Upon Receipt

As soon as you receive a check that you intend to deposit or transfer, endorse it. This minimizes the risk of losing the check before you have a chance to secure it. If you are mailing the check, endorse it restrictively (“For Deposit Only” with your account number) before sending it.

Use a Blue or Black Pen

Always use a blue or black ink pen for endorsing checks. These colors are typically required by banks for clarity and to prevent alteration. Avoid using pencils or erasable ink pens, as these can be easily altered and may lead to the check being rejected.

Endorse on the Correct Side

Checks have specific areas designated for endorsements. The endorsement should always be on the back of the check, usually within the top three inches of the left side. Banks have dedicated space for endorsements, and placing your signature or endorsement outside this area could lead to processing issues.

Match the Payee Name Exactly

When endorsing, ensure your signature or the name you write matches the payee name on the “Pay to the order of” line exactly. If the check is made out to “Jane Smith” but your legal name is “Jane A. Smith,” you might need to endorse it as “Jane Smith, then Jane A. Smith.” However, many banks will accept a signature that closely resembles the payee’s name. It’s advisable to check with your bank if you have consistent discrepancies.

Avoid Blank Endorsements Unless Necessary

As mentioned, blank endorsements are risky. Only use them if you are immediately handing the check to someone you trust implicitly to deposit or cash it, and you understand the potential security implications. For most situations, a special or restrictive endorsement is far more secure.

Be Wary of “For Deposit Only” with Other Endorsements

While “For Deposit Only” is a strong restrictive endorsement, be cautious if you see it combined with other endorsements that might seem contradictory or attempt to add further conditions without clear bank acceptance.

Keep a Record

For significant transactions, it can be helpful to keep a record of checks you’ve endorsed, especially if they are for large amounts or involve complex transfers. This can serve as a reference point if any disputes arise later.

What Happens When an Endorsement is Incorrect or Missing?

An incorrect or missing endorsement is one of the most common reasons a bank might reject a check. This can lead to delays in accessing your funds and can be frustrating.

Rejected Checks

If a check is presented with an improper endorsement, the bank will likely return it to the person who presented it. This means the funds will not be credited to the recipient’s account. The check will need to be corrected or reissued.

Potential Liability

In cases of incorrect endorsement that lead to a fraudulent transaction, the original payee or the bank could potentially face liability. This is why accuracy and adherence to proper procedures are so important. For example, if a check intended for “John Doe” is endorsed by “Jane Doe” and deposited into Jane’s account, and John Doe later claims the funds, there could be a dispute.

Rectifying Errors

If you realize you’ve made an endorsement error, contact your bank immediately. They can advise you on the best course of action. In some cases, you might be able to ask the bank to correct the endorsement if the error is minor and the intent is clear. However, for significant errors or to transfer ownership, it might be necessary to have the original issuer reissue the check.

The Role of Banks in Endorsements

Banks play a crucial role in processing checks and verifying endorsements. They have established procedures and systems to detect fraudulent or improper endorsements.

Verification Process

When you deposit or cash a check, the bank’s tellers and processing systems will examine the back of the check for endorsements. They look for signatures, dates, and adherence to the bank’s policies regarding the endorsement area. Special attention is paid to restrictive endorsements to ensure they are honored.

Fraud Detection

Banks are on the front lines of preventing financial fraud. They are trained to spot suspicious endorsements, such as signs of tampering, endorsements by individuals other than the named payee, or inconsistencies in the signature.

Endorsement Stamps

Businesses that receive many checks often use endorsement stamps. These stamps can be pre-configured with “For Deposit Only” and the business’s account information, streamlining the endorsement process. However, even with stamps, proper authorization and use are critical.

Conclusion

Endorsing a check is a fundamental financial action that requires careful attention to detail. Whether you are simply signing your name or specifying a new payee, understanding the different types of endorsements and following best practices ensures the security and efficiency of your financial transactions. From blank endorsements that carry inherent risks to restrictive endorsements that safeguard your funds, each method serves a distinct purpose. By mastering the art of check endorsement, individuals and businesses can navigate the complexities of financial dealings with greater confidence and avoid common pitfalls.