The term “Plan G” is most commonly associated with Medicare Supplement Insurance, also known as Medigap. These plans are designed to help cover some of the out-of-pocket costs that Original Medicare (Parts A and B) doesn’t cover. While the specific details of Plan G can vary slightly by state and insurer, its core benefits and the concept of its deductible are consistent. This article will delve into the Plan G deductible, explaining its significance, how it works, and what it means for beneficiaries.

Understanding Medicare Supplement Insurance (Medigap) and Plan G

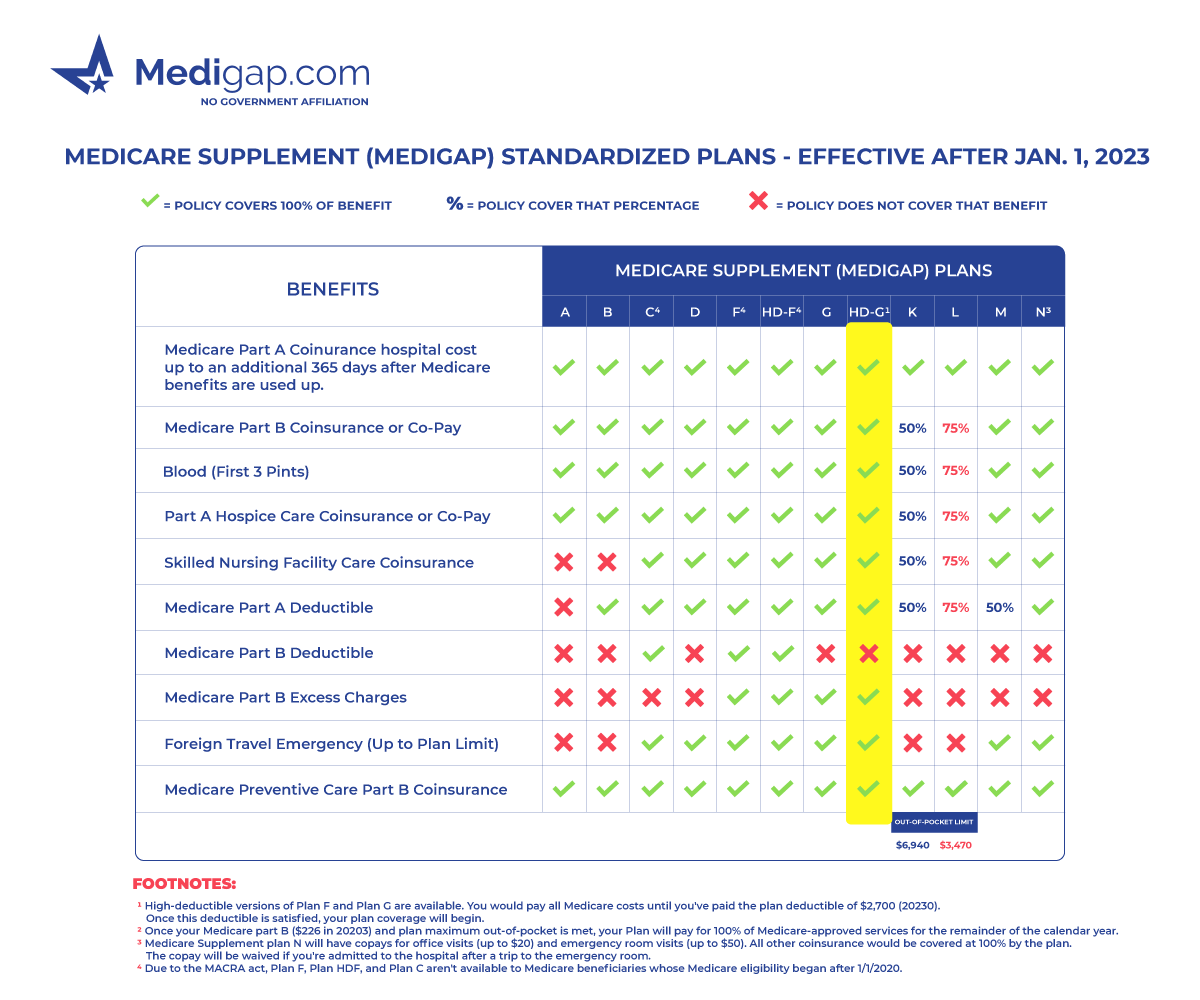

Medicare Supplement Insurance plans are standardized by the federal government. This means that each lettered plan (like Plan G) offers the same basic benefits, regardless of which insurance company sells it. However, premiums can differ between insurers. Plan G is one of the most popular Medigap plans because it offers comprehensive coverage and is often seen as a good value.

The Role of Original Medicare

Before understanding Medigap, it’s crucial to grasp the basics of Original Medicare.

Medicare Part A: Hospital Insurance

Medicare Part B is primarily for inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care. It helps cover costs like semi-private room charges, meals, general nursing, drugs and biologicals that are part of your inpatient treatment, and other hospital services and supplies.

Medicare Part B: Medical Insurance

Medicare Part B covers outpatient services, doctor’s visits, preventive care, durable medical equipment, and other medical services and supplies. It’s essential for covering the costs of seeing physicians, specialists, and receiving medical treatments outside of a hospital setting.

How Medigap Plans Fill the Gaps

Original Medicare doesn’t cover everything. There are deductibles, coinsurance, and copayments that beneficiaries are responsible for. Medigap plans are designed to pick up many of these costs. They work alongside Original Medicare, paying for the “gaps” in coverage. It’s important to note that you must have Original Medicare (Part A and Part B) to enroll in a Medigap plan. You cannot use a Medigap policy to have Medigap and Medicare Advantage (Part C) cover the same health services and costs.

The Plan G Deductible Explained

The Plan G deductible is a critical component of this Medigap plan and is directly tied to Medicare Part B.

The Medicare Part B Deductible

The Plan G deductible per year is, in essence, the Medicare Part B deductible. For 2024, the Medicare Part B annual deductible is $233. This means that after you’ve enrolled in Original Medicare and a Plan G policy, you will be responsible for paying the first $233 of your Medicare-approved medical expenses each year. Once you’ve met this deductible, Medicare Part B begins to pay its share of the cost of your covered health care services, and then Plan G kicks in to cover the remaining copayments and coinsurance.

How the Plan G Deductible Works in Practice

Let’s illustrate with an example. Suppose you have a doctor’s visit that Medicare approves for $100.

- Initial Costs: You are responsible for paying the first $233 of your Part B covered services.

- Meeting the Deductible: You continue to incur medical expenses throughout the year. Once the total of these out-of-pocket expenses reaches $233, you have met your Part B deductible.

- After Deductible: For any subsequent Medicare-approved medical services within that calendar year, Medicare Part B will pay its standard portion (typically 80% of the Medicare-approved amount after the deductible is met).

- Plan G’s Role: Your Plan G policy will then cover the remaining 20% coinsurance that would otherwise be your responsibility. This is a significant benefit, as it means you’re generally not responsible for any further out-of-pocket costs for Part B covered services once the deductible is met and Medicare has paid its share.

Crucial Distinction: Plan G vs. Other Medigap Plans

It is vital to distinguish Plan G from other Medigap plans, particularly Plan F.

Plan G vs. Plan F

Plan F was historically the most comprehensive Medigap plan, covering all the same benefits as Plan G plus the Medicare Part B deductible. However, under the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), new Medicare beneficiaries who became eligible for Medicare on or after January 1, 2020, cannot purchase Medigap plans that cover the Part B deductible, including Plan F.

This means that if you are a new Medicare beneficiary, Plan G is the most comprehensive plan available. For those who already had Plan F before January 1, 2020, they can continue to keep their plan. The fact that Plan G does not cover the Part B deductible is its defining characteristic compared to the old Plan F.

Benefits of Choosing Plan G

Despite having a deductible, Plan G offers substantial benefits that make it a popular choice for many Medicare beneficiaries.

Comprehensive Coverage Beyond the Deductible

Once the Part B deductible is met, Plan G provides exceptional coverage for a wide range of medical expenses.

Coinsurance and Copayments for Part B Services

As mentioned, Plan G covers the 20% coinsurance that Original Medicare does not pay for Part B services. This includes:

- Doctor’s office visits

- Outpatient surgery

- Diagnostic tests (X-rays, lab work)

- Durable medical equipment (wheelchairs, walkers)

- Preventive services

Skilled Nursing Facility Care Coinsurance

Plan G also covers the coinsurance for skilled nursing facility (SNF) care. While Medicare Part A covers the first 20 days of SNF care at 100%, days 21 through 100 typically have a daily coinsurance. Plan G picks up this cost.

Medicare Part A Hospital Costs

Plan G offers extensive coverage for Medicare Part A hospital costs. This includes:

- Hospital Stays: It covers the Part A hospital deductible, which is the amount you pay for each benefit period.

- Inpatient Hospital Services: It covers the daily coinsurance for extended hospital stays.

- Blood: Plan G covers the cost of the first three pints of blood you need for a covered hospital or medical service.

Hospice Care and Foreign Travel Emergency

In addition to inpatient hospital services, Plan G also covers:

- Hospice Care: It helps with coinsurance and copayment for hospice care and respite care.

- Foreign Travel Emergency: This is a valuable benefit for those who travel internationally. Plan G covers 80% of the Medicare-approved amount for medically necessary emergency hospital care received while traveling outside the United States, up to a lifetime limit. This coverage applies after you’ve paid a $250 deductible.

Considerations When Choosing Plan G

While Plan G is highly beneficial, it’s essential to weigh its advantages against potential drawbacks and consider your personal circumstances.

Premium Costs

The most significant factor to consider with any Medigap plan is the premium. While Plan G offers comprehensive benefits, its monthly premium can be higher than some other Medigap plans that offer less coverage. Premiums can vary based on factors such as your age, gender, location, and the insurance company you choose. It’s crucial to shop around and compare quotes from different insurers to find the most affordable option for your budget.

The Annual Part B Deductible

The fact that you are responsible for the Part B deductible each year is a key consideration. If you anticipate having very few medical services in a given year, you might not even meet the deductible. However, if you have chronic conditions or expect to need significant medical care, the deductible will be paid early in the year, and then your comprehensive coverage will take over.

Enrollment Periods

Understanding Medicare enrollment periods is vital. The best time to enroll in a Medigap plan is during your Medigap Open Enrollment Period, which is a six-month period that begins on the first day of the month in which you are age 65 or older and enrolled in Medicare Part B. During this period, insurance companies cannot deny you coverage or charge you more due to your health status. If you try to enroll outside of this period, you may face medical underwriting, meaning your application could be denied or your premiums could be higher if you have pre-existing health conditions.

Conclusion: Plan G as a Comprehensive Coverage Option

The Plan G deductible per year is the Medicare Part B annual deductible. For 2024, this is $233. This deductible is the only out-of-pocket cost you will have for Part B covered services once it’s met, as Plan G then covers the remaining 20% coinsurance. Beyond Part B, Plan G provides robust coverage for Part A hospital deductibles and coinsurance, skilled nursing facility care, hospice care, and even foreign travel emergencies.

For individuals new to Medicare or those seeking a high level of predictable healthcare costs after an initial deductible, Plan G presents a compelling and valuable option. It offers peace of mind by significantly reducing the financial burden of unexpected medical expenses, allowing beneficiaries to focus on their health and well-being with confidence. As with any insurance decision, it is always recommended to consult with a licensed insurance agent or counselor to ensure Plan G aligns with your specific health needs and financial situation.