Understanding the nuances of the Inflation Adjustment for Medicare-Related Amounts (IRMAA) is crucial for individuals anticipating or already receiving Medicare benefits, particularly as the cost of living and healthcare expenses continue to evolve. As we look ahead to 2024, a comprehensive grasp of IRMAA is not just about financial planning; it’s about ensuring access to vital healthcare services without undue burden. This article will delve into the intricacies of IRMAA for 2024, exploring its purpose, how it’s calculated, who it affects, and strategies for managing its impact.

Understanding the Foundation of IRMAA

The concept of IRMAA stems from the need to ensure that individuals with higher incomes contribute a fairer share towards their Medicare Part B and Medicare Part D premiums. This mechanism is designed to maintain the solvency of the Medicare program while acknowledging that those with greater financial capacity can afford to contribute more.

What is Medicare?

Medicare is the United States federal health insurance program primarily for people aged 65 or older, as well as for younger people with certain disabilities and people with End-Stage Renal Disease (ESRD). It is a critical component of the healthcare safety net for millions of Americans, covering a wide range of medical services and prescription drugs.

Medicare is divided into several parts:

- Part A (Hospital Insurance): Helps cover inpatient hospital stays, care at a skilled nursing facility, hospice care, and some home health care.

- Part B (Medical Insurance): Helps cover doctor services, outpatient care, medical supplies, and preventive services. Most people pay a monthly premium for Part B.

- Part D (Prescription Drug Coverage): Helps cover the cost of prescription drugs. This coverage is offered through private insurance companies that have been approved by Medicare. Most people with Part A or B enroll in a stand-alone Part D plan or a Medicare Advantage Plan with drug coverage.

The Purpose and Rationale Behind IRMAA

The Higher Income Surtax, which IRMAA is a part of, was introduced to address the financial sustainability of Medicare. As the population ages and healthcare costs increase, the program faces significant financial pressures. By requiring higher earners to pay more for their Medicare premiums, the government aims to supplement the program’s funding and alleviate some of the burden on taxpayers who do not have higher incomes.

The rationale is rooted in the principle of progressive taxation, where those with greater ability to pay contribute more. For Medicare, this means that individuals whose Modified Adjusted Gross Income (MAGI) exceeds certain thresholds are subject to an additional amount on top of their standard Medicare premiums. This surtax applies to both Medicare Part B and Part D premiums.

Who Administers IRMAA?

The Internal Revenue Service (IRS) is responsible for determining an individual’s IRMAA. The Social Security Administration (SSA) then uses the IRS’s findings to collect the additional premiums from beneficiaries. This collaboration ensures that income data is used accurately to calculate the correct IRMAA amounts.

The process typically involves the IRS reviewing tax returns from two years prior to the current benefit year. For instance, when determining IRMAA for 2024, the IRS will look at tax returns filed in 2023 for income earned in 2022. This lag time is intentional, allowing the IRS to process tax returns and the SSA to implement the necessary premium adjustments.

Calculating IRMAA for 2024: Income Thresholds and Surcharges

The core of understanding IRMAA lies in grasping how your income directly influences your Medicare premiums. The calculation is not static; it’s tied to specific income brackets and adjustments made annually to account for inflation.

Modified Adjusted Gross Income (MAGI) and Tax Returns

The primary determinant of your IRMAA is your Modified Adjusted Gross Income (MAGI). MAGI is your Adjusted Gross Income (AGI) with certain deductions added back. The IRS typically uses your tax return from two years prior to determine your MAGI for IRMAA purposes.

For 2024, the SSA will look at your 2022 tax return to determine your MAGI. It’s important to note that MAGI is not simply your reported income. It’s a specific calculation that can be found on your tax forms. If you file jointly with a spouse, the combined MAGI of both individuals is used to determine the IRMAA applicable to both.

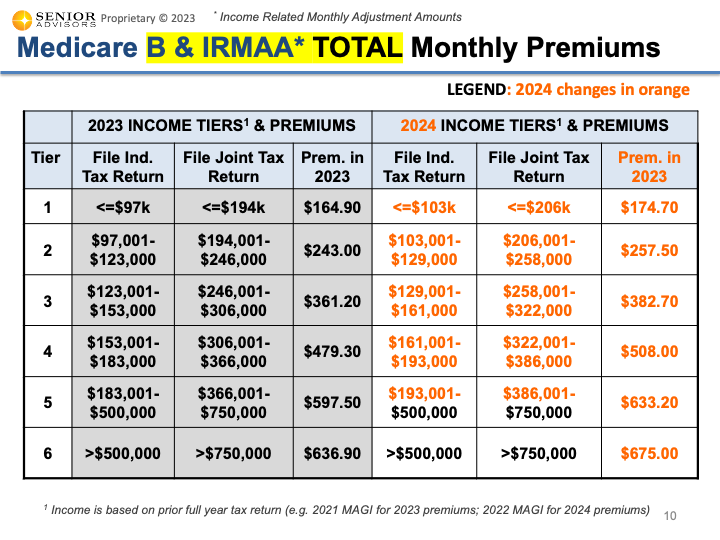

IRMAA Tiers and Surcharges for 2024

Medicare beneficiaries are categorized into several tiers based on their MAGI. Each tier corresponds to a specific surcharge amount that is added to the standard Medicare Part B and Part D premiums. These tiers and their associated surcharges are adjusted annually for inflation.

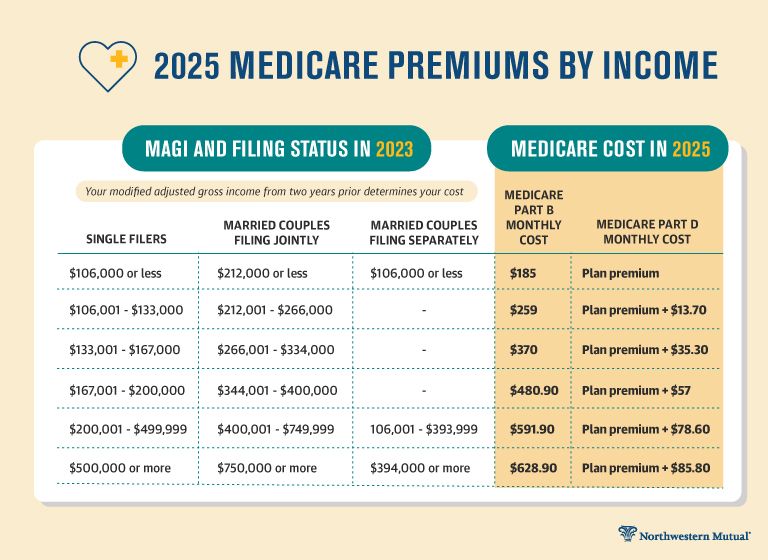

For 2024, the IRMAA surcharges for Medicare Part B are as follows:

- Individuals:

- $97,000 or less: Standard premium (no IRMAA)

- $97,001 to $123,000: $164.90 (plus standard premium)

- $123,001 to $153,000: $329.80 (plus standard premium)

- $153,001 to $183,000: $494.70 (plus standard premium)

- $183,001 to $400,000: $659.60 (plus standard premium)

- Over $400,000: $989.40 (plus standard premium)

- Married Couples Filing Jointly:

- $194,000 or less: Standard premium (no IRMAA)

- $194,001 to $246,000: $164.90 (per person, plus standard premium)

- $246,001 to $306,000: $329.80 (per person, plus standard premium)

- $306,001 to $366,000: $494.70 (per person, plus standard premium)

- $366,001 to $800,000: $659.60 (per person, plus standard premium)

- Over $800,000: $989.40 (per person, plus standard premium)

The standard Medicare Part B premium for 2024 is $174.70. Therefore, the total monthly premium for an individual in the highest IRMAA tier would be $174.70 (standard) + $989.40 (IRMAA) = $1164.10.

Similarly, IRMAA surcharges apply to Medicare Part D premiums. These are calculated based on the same MAGI thresholds as Part B, but the actual dollar amounts of the surcharges are different and are added to the premium of your specific Part D plan. The national base beneficiary premium for Part D in 2024 is $34.70.

How Inflation Adjustments Affect IRMAA

The “Inflation Adjustment” in IRMAA signifies that the income thresholds and the corresponding surcharges are reviewed and potentially updated each year to reflect changes in the cost of living. This means that while your income might remain the same, you could find yourself falling into a higher IRMAA tier in a subsequent year if the thresholds are lowered due to inflation. Conversely, if inflation is low or the thresholds are adjusted upwards, you might remain in a lower tier.

The Social Security Administration utilizes the Consumer Price Index (CPI) to guide these annual adjustments. This ensures that the IRMAA provisions remain relevant and fair in the context of the prevailing economic conditions.

Navigating and Managing IRMAA

Understanding IRMAA is the first step; the next is knowing how to manage its financial implications. This involves being aware of the potential for adjustment and having strategies in place to mitigate its impact.

Appealing Your IRMAA Determination

If you believe your IRMAA determination is incorrect, you have the right to appeal. Common reasons for an appeal include having experienced a “life-changing event” that significantly reduced your income since the tax year used for the determination.

Life-changing events that may qualify for an IRMAA appeal include:

- Marriage: If you married and your combined MAGI is lower than what was used for the individual determination.

- Divorce or Annulment: If your divorce or annulment resulted in a lower MAGI.

- Death of a Spouse: If your spouse died and your MAGI is now lower.

- Work Stoppage or Reduction of Hours: If you or your spouse stopped working or had your work hours significantly reduced, leading to a lower MAGI.

- Loss of Income-Producing Property: If you lost income from property that was a primary source of income.

- Loss of Pension or Other Income: If you or your spouse lost a pension or experienced a significant reduction in other income.

To appeal, you will need to submit a Request for Reconsideration and provide documentation to support your claim. The SSA will review your case and make a determination.

Strategies for Reducing Your MAGI

While not always feasible, some individuals may be able to reduce their MAGI to avoid or lower their IRMAA surcharges. This often involves careful tax planning in the years prior to the IRMAA determination.

Some strategies might include:

- Maximizing Tax-Advantaged Retirement Accounts: Contributing to traditional IRAs or 401(k)s can reduce your AGI, and consequently your MAGI. However, be mindful of the two-year lookback period.

- Strategic Selling of Assets: If you have significant capital gains, timing the sale of assets to occur in years with lower income might be beneficial.

- Converting Traditional IRA to Roth IRA: While this creates a taxable event in the year of conversion, it can reduce your taxable income in future years, potentially lowering your MAGI.

- Donating to Charity: Certain charitable contributions can be tax-deductible and reduce your AGI.

It is essential to consult with a qualified tax advisor or financial planner before implementing any strategies to reduce your MAGI, as they can have broader financial implications.

Planning for Future IRMAA Increases

Given the annual inflation adjustments, it is prudent to anticipate that your IRMAA surcharges may increase over time. Proactive financial planning can help you prepare for these potential increases.

This includes:

- Reviewing Your Financial Projections: Regularly assess your income and assets to understand your potential MAGI for future years.

- Creating a Dedicated Savings Fund: Consider setting aside funds specifically to cover potential IRMAA increases.

- Staying Informed: Keep abreast of any changes to Medicare premiums and IRMAA regulations announced by the SSA.

By understanding the intricacies of IRMAA and employing proactive strategies, Medicare beneficiaries can better navigate the complexities of their healthcare costs and ensure continued access to essential medical services. The IRMAA for 2024, like in previous years, serves as a reminder of the importance of financial awareness as individuals age and access their Medicare benefits.