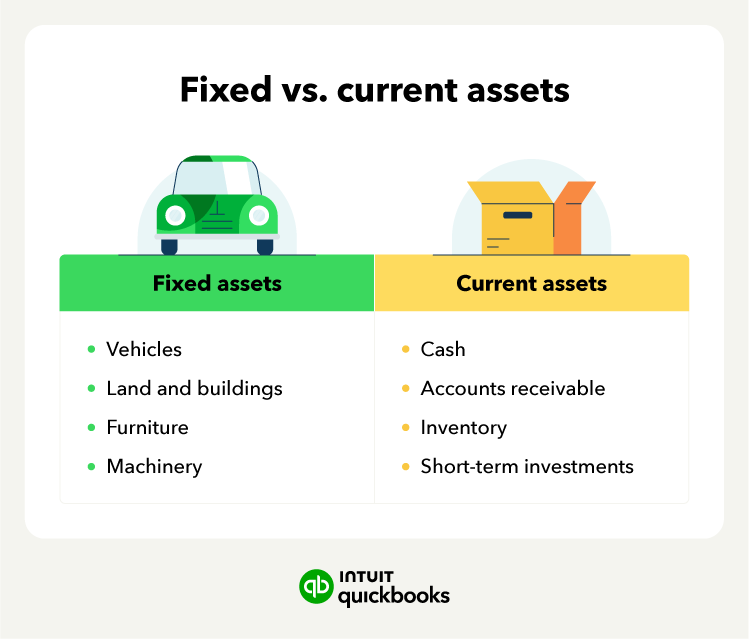

In the realm of business and accounting, understanding the fundamental components of an organization’s financial structure is paramount. Among these components, fixed assets hold a position of significant importance. They represent the tangible, long-term investments that a company makes to facilitate its operations and generate revenue. Unlike current assets, which are expected to be converted into cash within a year, fixed assets have a lifespan extending beyond this period, often for many years. This inherent longevity and their role in the core business activities distinguish them as crucial elements in a company’s balance sheet and its overall economic strategy.

The term “fixed” in fixed asset refers to their relatively permanent nature. They are not intended for resale in the ordinary course of business. Instead, they are acquired to be used in the production of goods or services, for rental to others, or for administrative purposes. Their value is not consumed quickly; rather, it depreciates over time due to wear and tear, obsolescence, or usage. Consequently, their accounting treatment involves a systematic allocation of their cost over their useful economic life through a process known as depreciation.

Defining Fixed Assets: Beyond the Tangible

While the most common understanding of fixed assets leans towards the tangible, it’s important to acknowledge that the definition can extend to certain intangible items that share similar characteristics of long-term use and value generation. However, for clarity and the purposes of this discussion, we will primarily focus on the tangible fixed assets that form the bedrock of most businesses.

Tangible vs. Intangible: A Crucial Distinction

Tangible fixed assets are those that have a physical form. They can be touched, seen, and measured. Examples abound across industries: a manufacturing plant with its machinery, an office building, a fleet of delivery trucks, computer hardware, and even basic office furniture. These are the physical tools that enable a business to operate on a daily basis.

Intangible fixed assets, on the other hand, lack a physical form but still represent long-term economic benefits. These might include patents, copyrights, trademarks, software licenses, and goodwill. While they are critical for business success, their valuation and accounting treatment differ significantly from tangible assets. For the scope of this article, our emphasis remains on the tangible.

The Purpose of Acquisition: Driving Business Operations

The fundamental reason a business acquires fixed assets is to support its ongoing operations and generate future economic benefits. A restaurant needs ovens and dining tables. A software company needs computers and office space. A transportation company needs vehicles. Each of these assets is an investment designed to facilitate the core business activities, increase efficiency, enhance productivity, or provide a service that generates revenue.

Types of Fixed Assets: A Diverse Portfolio

The category of fixed assets is broad and encompasses a wide array of items. Understanding these different types is crucial for accurate financial reporting and effective asset management. They can be broadly categorized based on their nature and function within the business.

Property, Plant, and Equipment (PP&E)

This is perhaps the most widely recognized subset of fixed assets. PP&E includes land, buildings, machinery, equipment, furniture, fixtures, and vehicles.

- Land: This is unique among fixed assets as it is generally not depreciated. Its value is considered to be perpetual, although its market value can fluctuate. Land improvements, such as landscaping or paving, are depreciated.

- Buildings: This includes factories, warehouses, office buildings, and retail stores. Their cost includes not only the purchase price but also any costs incurred to prepare them for use, such as architect fees and construction costs.

- Machinery and Equipment: This encompasses the specialized tools and machines used in production processes, as well as general office equipment like computers and printers. Their useful life and depreciation rate are determined by factors like technology, wear and tear, and expected usage.

- Vehicles: This category includes cars, trucks, vans, and other modes of transport used for business purposes, such as deliveries, sales calls, or employee transportation.

Natural Resources

These are assets that are extracted from the earth and are considered to be “consumed” as they are used. Examples include timber, minerals, and oil reserves. Unlike PP&E, their depletion is accounted for, reflecting the physical exhaustion of the resource.

Investments in Other Entities (Long-Term)

While not always classified strictly as “fixed assets” in the same vein as PP&E, long-term investments in the stock or bonds of other companies are considered long-term assets. They are held for an extended period to generate income or gain capital appreciation, and they are not intended for immediate sale.

The Lifecycle of a Fixed Asset: From Acquisition to Disposal

The journey of a fixed asset within a business is a structured process that involves several key stages. Each stage has specific accounting implications and impacts the company’s financial statements.

Acquisition: The Initial Investment

The acquisition of a fixed asset represents a significant capital expenditure. The cost of an asset includes not only its purchase price but also all expenditures necessary to bring the asset to its intended use. This can include transportation costs, installation fees, testing costs, and any legal or brokerage fees associated with the purchase. For instance, when a company buys a new manufacturing machine, its cost will include the price of the machine, shipping fees to the factory, and the cost of specialized technicians to install and calibrate it.

Depreciation: Allocating the Cost

As mentioned earlier, fixed assets, with the exception of land, lose value over time. Depreciation is the accounting method used to systematically allocate the cost of a tangible asset over its useful economic life. It’s not about reflecting the market value but rather matching the expense of using the asset with the revenue it helps to generate during its operational period.

Methods of Depreciation

There are several methods of depreciation, each with its own approach to allocating cost:

- Straight-Line Depreciation: This is the simplest and most common method. It allocates an equal amount of depreciation expense to each year of the asset’s useful life. The formula is: (Cost – Salvage Value) / Useful Life.

- Declining Balance Method: This is an accelerated depreciation method that recognizes more depreciation expense in the earlier years of an asset’s life and less in the later years.

- Units-of-Production Method: This method bases depreciation on the asset’s usage rather than the passage of time. The depreciation expense varies with the level of production or usage.

Maintenance and Improvements: Extending Lifespan and Value

Businesses invest in maintaining their fixed assets to ensure they function optimally and to extend their useful lives. Routine maintenance, such as oil changes for vehicles or servicing for machinery, is typically expensed as incurred. However, significant improvements or additions that extend the asset’s useful life or increase its productivity are often capitalized, meaning they are added to the asset’s book value and depreciated over the remaining life of the asset.

Disposal: Realizing the End of the Road

Eventually, a fixed asset will reach the end of its useful life or become obsolete. When this happens, the asset is disposed of. Disposal can occur through sale, scrapping, or retirement. The accounting treatment for disposal involves removing the asset and its accumulated depreciation from the balance sheet and recognizing any gain or loss on the disposal. For example, if a company sells an old delivery truck for less than its book value, it will record a loss on the sale.

The Importance of Fixed Assets in Business Strategy

Fixed assets are not merely accounting entries; they are integral to a company’s strategic planning, operational efficiency, and long-term financial health. Their acquisition and management require careful consideration.

Capital Budgeting and Investment Decisions

The acquisition of fixed assets often involves substantial capital outlays. This necessitates a robust capital budgeting process, where businesses evaluate the potential return on investment, the payback period, and the strategic alignment of proposed asset purchases. Decisions regarding which fixed assets to acquire, when to acquire them, and how to finance them have a profound impact on a company’s future profitability and competitiveness.

Impact on Financial Statements

Fixed assets significantly influence a company’s balance sheet, income statement, and cash flow statement. On the balance sheet, they represent a substantial portion of total assets. Depreciation expense, recorded on the income statement, reduces net income. The capital expenditures related to fixed assets are also a key component of the investing activities section of the cash flow statement. Understanding these impacts is crucial for investors, creditors, and management to assess a company’s financial performance and position.

Enhancing Competitive Advantage

Strategic investment in modern and efficient fixed assets can provide a significant competitive advantage. For instance, a manufacturing company that invests in state-of-the-art machinery may be able to produce goods at a lower cost or with higher quality than its competitors. Similarly, a logistics company with a technologically advanced fleet can offer faster and more reliable delivery services. The right fixed assets are enablers of innovation, efficiency, and ultimately, market leadership.