If you have ever been fallen behind on a credit card bill, medical bill, or personal loan, you may have dealt with debt collectors. While they have a right to collect what is owed, they do not have a right to harass or deceive you. This is where the Fair Debt Collection Practices Act (FDCPA) comes into play.

But exactly what is the FDCPA, and how does it protect you? This guide breaks down everything you need to know.

1. Defining the FDCPA

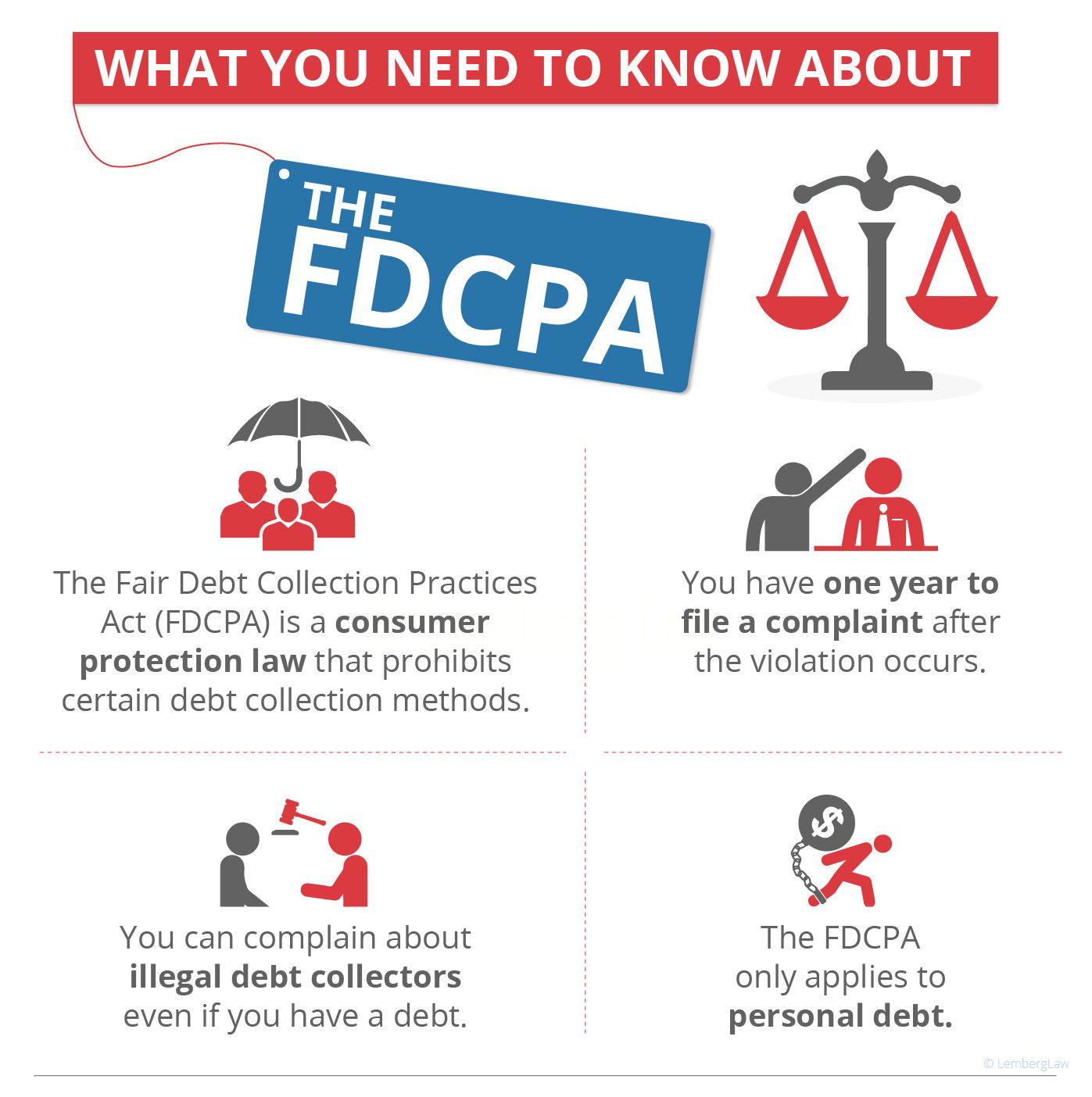

The Fair Debt Collection Practices Act (FDCPA) is a federal law enacted in 1977. Its primary goal is to eliminate abusive, deceptive, and unfair debt collection practices by debt collectors. It also provides consumers with a way to dispute debt information and ensure its accuracy.

The law is enforced by the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB).

2. Who Must Follow the FDCPA?

It is important to note that the FDCPA does not apply to everyone.

- It applies to: Third-party debt collectors (agencies that buy delinquent debts or are hired to collect for others) and attorneys who regularly collect debts.

- It generally does NOT apply to: The original creditor (e.g., the bank or store where you originally opened the account).

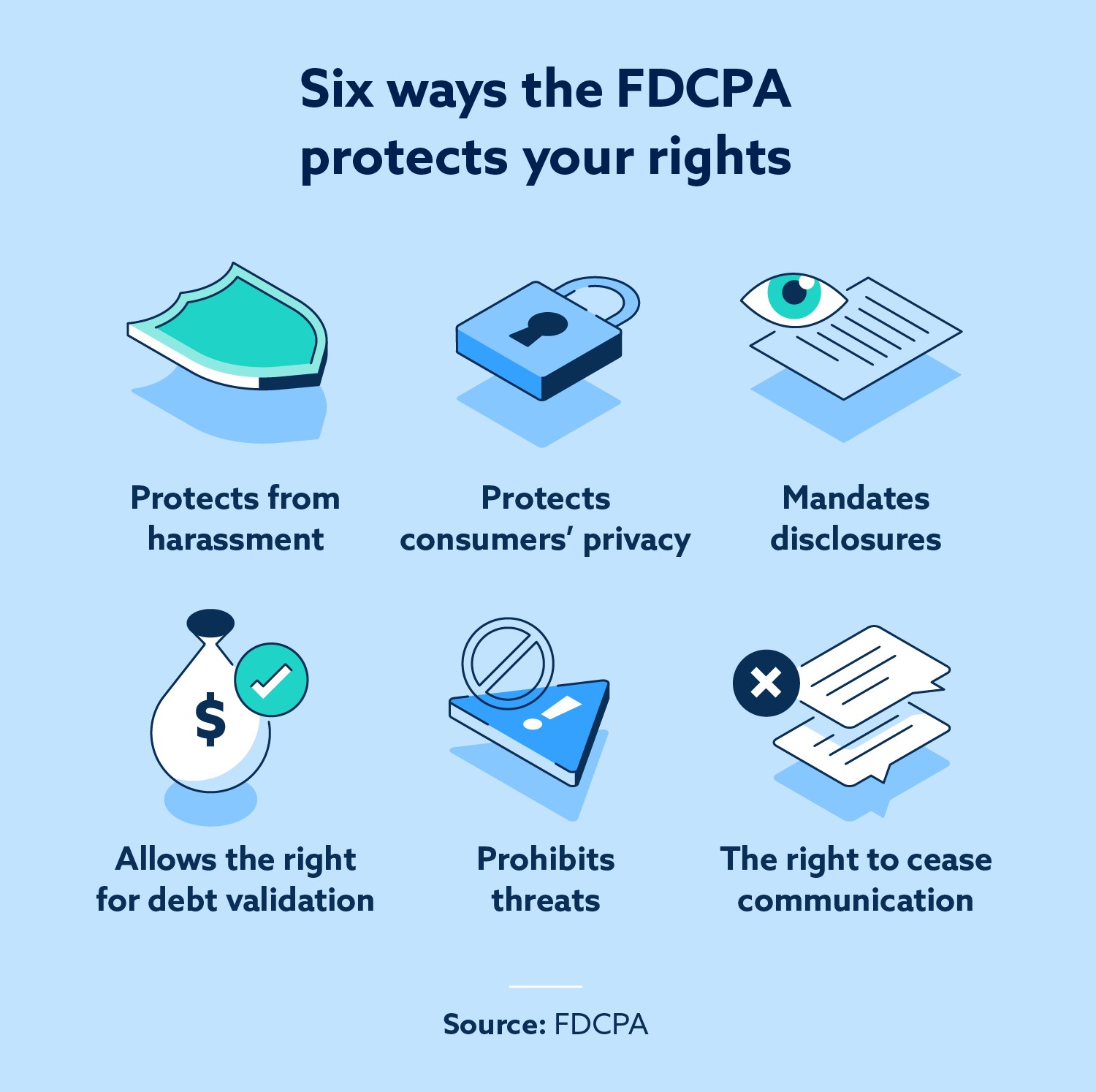

3. Key Rules: What Debt Collectors CANNOT Do

The FDCPA sets strict boundaries on how and when a collector can contact you. Under this law, debt collectors are prohibited from:

Harassment and Abuse

- Violence or Threats: They cannot threaten you with physical harm or use profane language.

- Repeated Calling: They cannot ring your phone incessantly with the intent to annoy or harass you.

- Public Shaming: They cannot publish your name on a “bad debt” list or discuss your debt with anyone other than you, your spouse, or your attorney.

False or Misleading Representations

- Impersonation: They cannot claim to be law enforcement, a government official, or an attorney if they are not.

- Legal Threats: They cannot threaten to arrest you or garnish your wages unless they actually intend to (and have the legal right to) do so.

- Lying about the Debt: They cannot misrepresent the amount you owe or the legal status of the debt.

Unfair Practices

- Hidden Fees: They cannot collect interest, fees, or charges on top of the debt unless the original contract or state law allows it.

- Post-dated Checks: They cannot solicit a post-dated check for the purpose of threatening criminal prosecution.

4. Restrictions on Communication

The FDCPA dictates exactly how communication should happen:

- Time of Day: Collectors may only call between 8:00 AM and 9:00 PM (your local time).

- At Work: If you tell a collector (verbally or in writing) that your employer forbids personal calls, they must stop calling you at work immediately.

- Representation: If you hire an attorney, the collector must communicate with the attorney, not you.

5. Your Rights as a Consumer

The FDCPA isn’t just a list of “don’ts” for collectors; it gives you active rights:

- The Right to Validation: Within five days of first contacting you, a collector must send a written “validation notice” stating the amount owed and the name of the creditor.

- The Right to Dispute: You have 30 days to dispute the debt in writing. Once you dispute it, the collector must stop collection activities until they provide proof of the debt.

- The Right to “Cease and Desist”: You can send a written letter to the collection agency telling them to stop contacting you. Once they receive it, they can only contact you to confirm they will stop or to notify you of a specific legal action (like a lawsuit).

6. What to Do if a Collector Violates the FDCPA

If you believe your rights have been violated, you have several options:

- Report them: File a complaint with the FTC, CFPB, or your State Attorney General.

- Sue for Damages: You can sue a debt collector in state or federal court within one year of the violation. If you win, you may be awarded $1,000 in statutory damages, plus actual damages (like lost wages or medical bills) and attorney fees.

- Keep Records: Always keep a log of calls, save voicemails, and keep copies of all written correspondence.

Conclusion

The FDCPA is a powerful shield for consumers. While you are still responsible for legitimate debts, you have the right to be treated with dignity and honesty. Knowing the rules of the FDCPA ensures that you won’t be bullied by aggressive collection tactics.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. If you are facing a legal issue regarding debt collection, please consult with a qualified attorney.