While the allure of tax-free income from municipal bonds is undeniable for many investors, particularly those in higher tax brackets, it’s crucial to understand that this municipal advantage isn’t without its drawbacks. These “munis”, as they are commonly known, are debt securities issued by state and local governments to finance public projects such as schools, hospitals, and infrastructure. Their primary appeal lies in the interest earned, which is generally exempt from federal income tax, and often from state and local taxes as well, if the bondholder resides in the issuing state. However, this tax shield can obscure other financial considerations that may lead to suboptimal investment outcomes.

Lower Yields: The Trade-Off for Tax Exemption

The most significant downside of tax-free municipal bonds, and the direct consequence of their tax-exempt status, is their typically lower yield compared to taxable bonds of similar credit quality and maturity. This phenomenon is often referred to as the “tax-equivalent yield.”

Understanding Tax-Equivalent Yield

To properly assess the attractiveness of a municipal bond, an investor must calculate its tax-equivalent yield. This calculation essentially determines what yield a taxable bond would need to offer to provide the same after-tax return as the tax-free municipal bond. The formula is as follows:

Tax-Equivalent Yield = (Municipal Bond Yield) / (1 – Marginal Tax Rate)

For example, if a municipal bond offers a yield of 3% and an investor’s marginal federal tax rate is 24%, the tax-equivalent yield would be:

Tax-Equivalent Yield = 0.03 / (1 – 0.24) = 0.03 / 0.76 = 0.03947, or approximately 3.95%.

This means that an investor in this tax bracket would need to find a taxable bond yielding around 3.95% to achieve the same after-tax return as the 3% municipal bond. If the investor is in a lower tax bracket, the tax-equivalent yield of the municipal bond will be lower, making it less appealing compared to taxable alternatives. Conversely, for individuals in the highest tax brackets, the tax savings can effectively make the municipal bond yield more competitive, or even superior, to taxable options.

The Impact of State and Local Taxes

The tax advantage can be further amplified if the municipal bond is issued within the investor’s home state, as the interest may also be exempt from state and local income taxes. This “double tax-exempt” or “triple tax-exempt” status (including federal) can significantly boost the attractiveness of certain municipal bonds. However, if an investor holds municipal bonds from other states, they may still be subject to state and local taxes on that interest, reducing the overall benefit. This adds another layer of complexity when comparing different municipal bond options and their relative attractiveness.

Interest Rate Risk and Market Fluctuations

Like all fixed-income securities, municipal bonds are subject to interest rate risk. When prevailing interest rates rise, the market value of existing municipal bonds with lower coupon rates tends to fall.

The Inverse Relationship Between Interest Rates and Bond Prices

The fundamental principle governing bond prices is their inverse relationship with interest rates. When new bonds are issued with higher coupon rates to reflect the current interest rate environment, older bonds with lower coupon rates become less attractive to investors. To sell these older bonds in the secondary market, their price must be discounted below their face value to compensate the buyer for the lower interest payments they will receive.

Impact on Bondholders

For investors who plan to hold their municipal bonds until maturity, rising interest rates might not directly impact their principal return (assuming the issuer doesn’t default). However, if an investor needs to sell their bonds before maturity, they could face a capital loss if interest rates have risen significantly. Conversely, if interest rates fall, the market value of existing municipal bonds with higher coupon rates will increase, offering a potential capital gain if sold before maturity.

Credit Risk and Default Potential

While municipal bonds are generally considered relatively safe investments, particularly those with high credit ratings, they are not entirely risk-free. The possibility of default, although rare for well-rated issuers, does exist.

Factors Influencing Creditworthiness

The creditworthiness of a municipal issuer is determined by various factors, including:

- Economic Health of the Municipality: A strong and diversified local economy, with a stable tax base and low unemployment, generally indicates a more secure issuer.

- Fiscal Management: Prudent budgeting, responsible debt management, and consistent revenue streams are crucial indicators of financial stability.

- Political Stability: Consistent governance and predictable policy-making can contribute to a municipality’s long-term financial health.

- Revenue Sources: The diversity and reliability of an issuer’s revenue sources (e.g., property taxes, sales taxes, income taxes, fees) play a significant role in its ability to meet its debt obligations.

- Existing Debt Load: A high level of outstanding debt can strain an issuer’s financial capacity, increasing the risk of default.

Credit Ratings and Their Importance

Credit rating agencies, such as Moody’s, Standard & Poor’s, and Fitch, assess the creditworthiness of municipal issuers and assign ratings to their bonds. Bonds rated “AAA” are considered the highest quality, with the lowest risk of default, while bonds with lower ratings (e.g., “Baa” or below) carry a higher degree of credit risk. Investors should carefully consider these ratings when selecting municipal bonds.

The Impact of Defaults

While infrequent, municipal bond defaults can occur, especially during periods of severe economic downturn or when an issuer faces significant fiscal challenges. When a default occurs, bondholders may lose a portion or all of their principal investment, as well as any anticipated interest payments. Although historically rare, high-profile defaults, such as those experienced by the city of Detroit, serve as stark reminders of this potential risk.

Liquidity Concerns in the Municipal Bond Market

The municipal bond market, while substantial, can sometimes suffer from lower liquidity compared to the markets for U.S. Treasury bonds or actively traded corporate bonds. This means it might be more challenging to buy or sell certain municipal bonds quickly without impacting their price.

Market Fragmentation and Specificity

The municipal bond market is highly fragmented, with a vast number of individual issuers and unique bond issues. Many of these issues are relatively small and may not trade frequently. This can lead to wider bid-ask spreads, meaning the difference between the price at which you can buy a bond and the price at which you can sell it is larger. For investors who need to exit their positions unexpectedly, this can result in a less favorable selling price.

Impact on Trading and Pricing

For less frequently traded municipal bonds, finding a buyer or seller at a desired price can be time-consuming. This lack of immediate trading opportunities can be a significant disadvantage, especially for investors who require flexibility or anticipate needing access to their capital on short notice. The depth of the market for specific municipal bonds can vary greatly, and investors should be aware of this before investing.

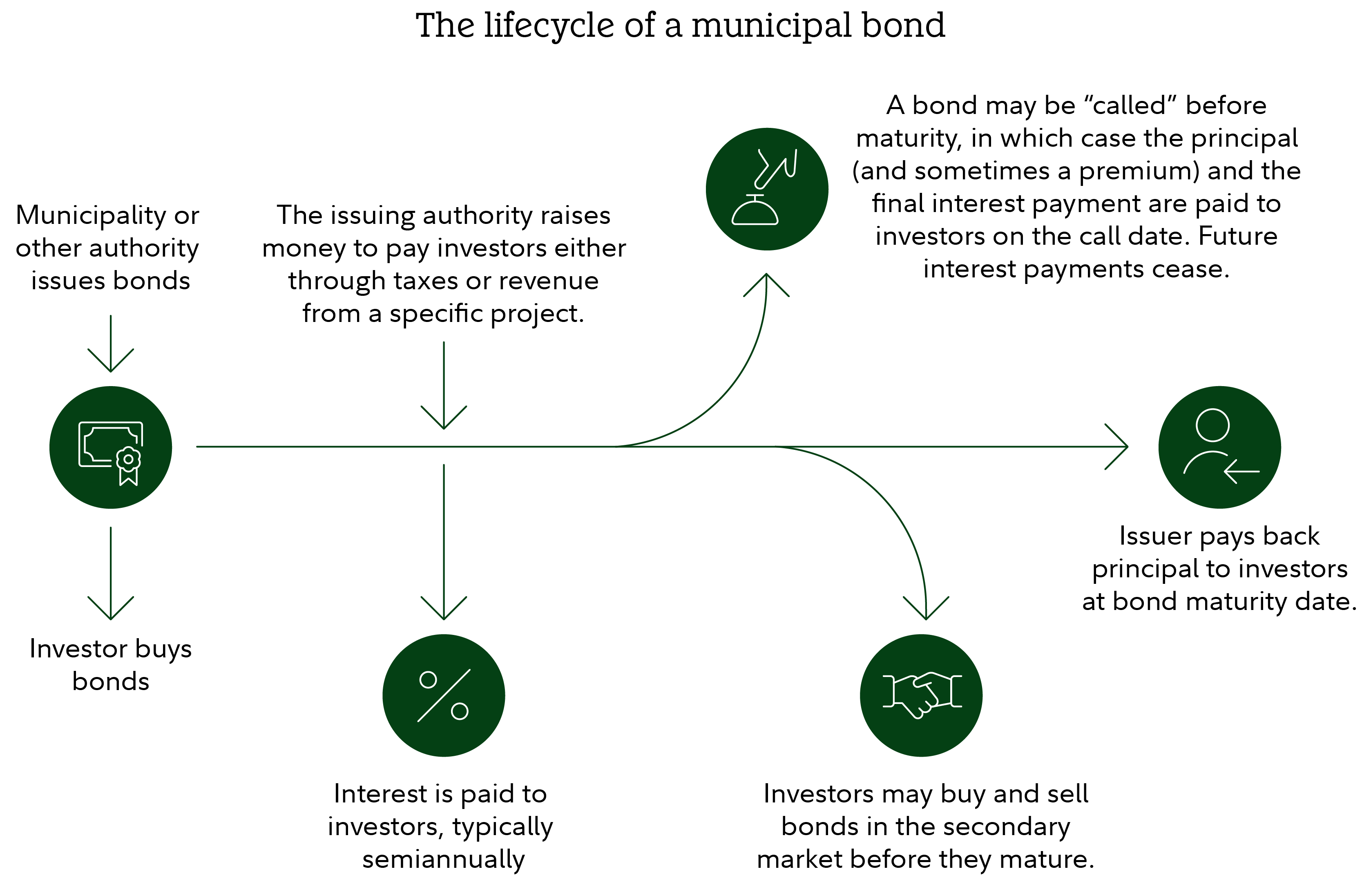

Call Provisions and Reinvestment Risk

Many municipal bonds are issued with a “call provision,” which gives the issuer the right to redeem the bond before its scheduled maturity date. This feature, while sometimes beneficial to the issuer, can create reinvestment risk for the bondholder.

How Call Provisions Work

An issuer might choose to call a bond if prevailing interest rates have fallen significantly since the bond was issued. By calling the bond, the issuer can then refinance its debt at a lower interest rate, saving money. For the bondholder, this means they receive their principal back sooner than expected, but at a time when interest rates are lower.

Reinvestment Risk Explained

The downside for the bondholder is the “reinvestment risk.” They are forced to reinvest the returned principal at the prevailing lower interest rates, potentially earning less income than they would have from the original, higher-coupon municipal bond. This can be particularly detrimental to investors who rely on the steady income stream from their bond investments.

Alternative Investments and Opportunity Cost

The tax advantages of municipal bonds are most pronounced for individuals in higher income tax brackets. For those in lower tax brackets, the lower yields may not adequately compensate for the tax savings, making other investment opportunities more attractive.

Evaluating the Opportunity Cost

When considering municipal bonds, it’s essential to weigh the opportunity cost. This involves comparing the potential returns of municipal bonds against other available investments, such as taxable bonds, dividend-paying stocks, real estate investment trusts (REITs), or even actively managed funds, after accounting for all relevant taxes and fees.

The Importance of a Holistic Financial Plan

A holistic financial plan, which considers an investor’s overall financial situation, risk tolerance, time horizon, and income level, is crucial in determining whether tax-free municipal bonds are an appropriate investment. For some investors, the tax benefits may be significant enough to outweigh the lower yields and other potential downsides. For others, taxable investments might offer a better risk-adjusted return profile.

In conclusion, while the tax-free nature of municipal bonds offers a compelling benefit for many, it is imperative to look beyond this primary advantage. A thorough understanding of lower yields, interest rate sensitivity, credit risk, liquidity concerns, call provisions, and the broader landscape of investment opportunities is essential for making informed decisions about whether tax-free municipal bonds align with an individual’s financial goals and risk profile.