The landscape of retirement and disability income in the United States can seem complex, with various programs designed to provide financial support to those in need. Among these, Supplemental Security Income (SSI) and Social Security benefits often cause confusion due to their similar-sounding names and shared administrative body, the Social Security Administration (SSA). However, these two programs serve distinct purposes, cater to different eligibility criteria, and offer varying levels of support. Understanding these differences is crucial for individuals seeking financial assistance, ensuring they apply for and receive the benefits for which they qualify.

Understanding Social Security Benefits

Social Security benefits, officially known as Old-Age, Survivors, and Disability Insurance (OASDI), are primarily an earned benefit. This means that eligibility and the amount of benefit received are directly tied to an individual’s work history and the amount of Social Security taxes they have paid throughout their working lives. When you or your employer pays into Social Security, these contributions fund the program, building up credits that determine your future benefit entitlement.

Eligibility for Social Security Benefits

There are several primary categories under which individuals can receive Social Security benefits:

Retirement Benefits

These are the most widely recognized Social Security benefits. To qualify for retirement benefits, an individual must have worked and paid Social Security taxes for a sufficient period, earning a minimum number of work credits. Most workers earn these credits by working and paying Social Security taxes. You can earn up to four credits per year. The number of credits required to be eligible for retirement benefits depends on your age when you become disabled, die, or retire. Generally, most people need 40 credits, equivalent to about 10 years of work.

Your full retirement age (FRA) is the age at which you are entitled to your full Social Security retirement benefit. This age varies depending on your birth year, ranging from 66 to 67. You can choose to start receiving retirement benefits as early as age 62, but your monthly benefit amount will be permanently reduced. Conversely, you can delay receiving benefits beyond your FRA, up to age 70, which will result in a higher monthly benefit.

Survivors Benefits

Social Security also provides benefits to the surviving spouse, children, and sometimes parents of a deceased worker who had earned enough work credits. These benefits are designed to offer financial support to families who have lost a primary breadwinner. The amount of the survivor benefit depends on the deceased worker’s earnings record and the beneficiary’s relationship to the deceased. For example, a surviving spouse may receive a percentage of the deceased’s benefit, while benefits for children are typically a fixed amount per child, up to a family maximum.

Disability Benefits (SSDI)

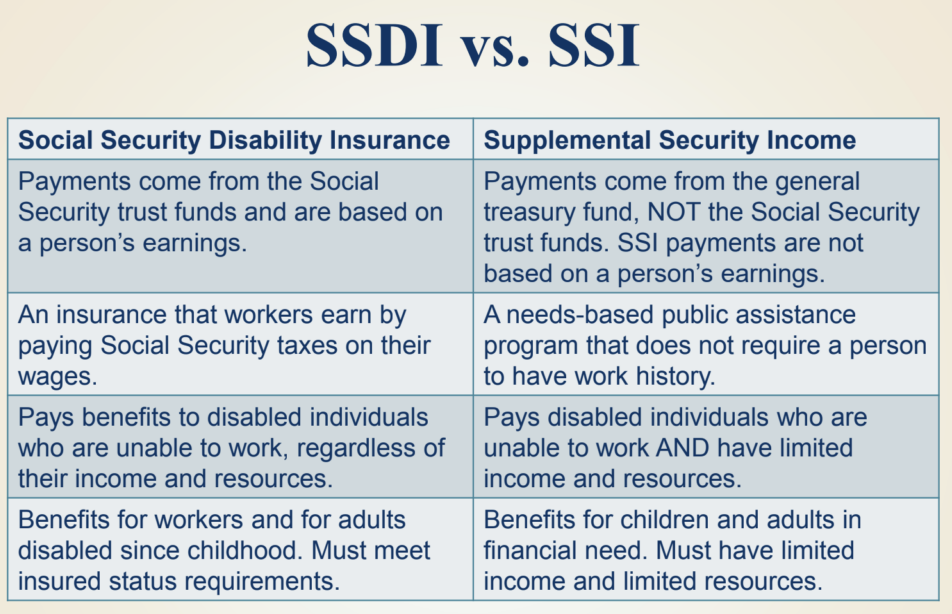

The Social Security Disability Insurance (SSDI) program provides benefits to individuals who have a qualifying disability and have a sufficient work history. To be considered disabled under SSDI, you must have a medical condition that is expected to last at least 12 months or result in death, and that prevents you from engaging in substantial gainful activity. The definition of “substantial gainful activity” is based on your earnings. For 2023, the monthly earnings limit for substantial gainful activity is $1,350 for non-blind individuals and $2,260 for individuals with blindness.

Unlike SSI, SSDI is an insurance program funded by Social Security taxes. Therefore, eligibility is based on your past earnings and the amount of Social Security taxes you have paid. If you are approved for SSDI, your benefit amount is calculated based on your average lifetime earnings.

Funding and Administration of Social Security Benefits

Social Security benefits are funded through dedicated payroll taxes, primarily levied on wages and self-employment income. These taxes are collected by the IRS and managed by the SSA. The funds collected are used to pay current beneficiaries. This pay-as-you-go system means that today’s workers are supporting today’s retirees and disabled individuals.

Understanding Supplemental Security Income (SSI)

Supplemental Security Income (SSI) is a needs-based program that provides a modest monthly income to individuals who are aged, blind, or disabled and have very limited income and resources. Unlike Social Security benefits, SSI is not based on an individual’s work history or the amount of taxes they have paid. Instead, it is a federal program administered by the SSA but funded by general tax revenues.

Eligibility for SSI

Eligibility for SSI is determined by a combination of factors:

Age, Blindness, or Disability

To qualify for SSI, an individual must be 65 years or older, or be blind, or be disabled. The definition of disability for SSI is the same as for SSDI: a medical condition that is expected to last at least 12 months or result in death, and that prevents you from engaging in substantial gainful activity. Blindness is defined as having a visual acuity of 20/200 or less in the better eye with the use of correcting lenses, or having a limitation in the field of vision such that the widest diameter of the visual field subtends an angle no greater than 20 degrees.

Income and Resource Limits

This is the defining characteristic of SSI. To be eligible, an individual must have very limited income and resources.

- Income: This includes money you receive from any source, such as wages, pensions, other benefits, gifts, and food stamps. There are specific exclusions for certain types of income, but generally, most income is counted. The SSA has a complex system for calculating countable income, with different rules for individuals and couples, and for those who are blind or disabled versus those who are aged.

- Resources: These are things you own, such as cash, bank accounts, stocks, bonds, and property (other than the home you live in and one vehicle). For 2023, an individual can have no more than $2,000 in resources, and a couple can have no more than $3,000 in resources. Certain resources are excluded from this limit, including the home you live in, one vehicle, household goods, and personal effects.

U.S. Citizenship or Eligible Alien Status

To receive SSI, you must be a U.S. citizen, or a qualifying non-citizen, and meet specific residency requirements.

Funding and Administration of SSI

SSI is funded by general tax revenues, meaning it is supported by the overall federal budget. This differs significantly from Social Security benefits, which are funded by dedicated payroll taxes. While the SSA administers both programs, the funding source has significant implications for the program’s budget and the amount of benefits provided.

Key Differences Summarized

The fundamental distinctions between SSI and Social Security benefits can be categorized as follows:

Basis of Eligibility

- Social Security Benefits (OASDI): Based on work history and contributions made through Social Security taxes (earned benefit).

- SSI: Based on financial need (limited income and resources) and specific criteria of age, blindness, or disability (needs-based benefit).

Funding Source

- Social Security Benefits (OASDI): Funded by payroll taxes (FICA and SECA taxes).

- SSI: Funded by general federal tax revenues.

Benefit Amount Calculation

- Social Security Benefits (OASDI): Calculated based on your average lifetime earnings and the number of work credits earned. This can result in a wide range of benefit amounts.

- SSI: A fixed federal benefit rate (which is periodically adjusted for inflation) is provided, with state supplements sometimes adding to the total. The amount is reduced by countable income. The maximum federal benefit rate for an individual in 2023 is $914 per month, and for a couple is $1,371 per month (these figures can vary slightly with cost-of-living adjustments).

Impact on Other Benefits

- Social Security Benefits (OASDI): Generally does not affect eligibility for other needs-based programs unless the benefit amount is high enough to disqualify you based on income or resource limits.

- SSI: Recipients often automatically qualify for other programs like Medicaid, which provides health coverage. Eligibility for SSI itself is dependent on meeting strict income and resource limits, so receiving other benefits can impact SSI eligibility or the SSI benefit amount.

Overlap and Interaction

While distinct, there are instances where individuals may receive or be eligible for both types of benefits, or where one can transition to the other.

Receiving Both SSI and Social Security Benefits

It is possible for an individual to receive both Social Security disability benefits (SSDI) and SSI. This typically occurs when an individual qualifies for SSDI but their SSDI benefit amount is very low due to a limited work history. If their SSDI benefit, combined with any other income and resources, falls below the SSI limits, they may be eligible for SSI to supplement their SSDI payment up to the SSI federal benefit rate. In such cases, the individual receives two separate checks, one for SSDI and one for SSI.

Transitioning Between Programs

Individuals who become disabled and are unable to work may initially apply for SSDI if they have a sufficient work history. If they do not meet the work credit requirements for SSDI, or if their disability onset predates their ability to earn enough credits, they may still be eligible for SSI based on their disability and financial need. Similarly, individuals receiving Social Security retirement benefits who experience a significant decrease in income and resources and meet the disability criteria might explore SSI eligibility.

![]()

Conclusion: Navigating Your Options

The difference between SSI and Social Security benefits boils down to their fundamental purpose and eligibility criteria: earned benefit versus needs-based assistance. Social Security benefits (retirement, survivors, and SSDI) are a form of social insurance, rewarding contributions made through work. SSI, on the other hand, serves as a safety net, providing essential financial support to the most vulnerable individuals who lack the means to support themselves due to age, blindness, or disability. Understanding these core differences is the first step in navigating the Social Security Administration’s programs effectively and ensuring access to the financial support that best suits an individual’s circumstances. Both programs play vital roles in the nation’s social welfare system, offering crucial assistance to millions of Americans.