Understanding the fundamental principles of interest is crucial in the world of finance. Whether you’re saving money, taking out a loan, or investing, knowing how interest accrues can significantly impact your financial outcomes. At its core, interest is the cost of borrowing money or the reward for lending it. The way this interest is calculated, however, can vary, leading to two primary methods: simple interest and compound interest. While both involve a percentage of a principal amount, their long-term effects are vastly different, with compound interest often hailed as a cornerstone of wealth creation. This article will delve into the nuances of each, highlighting their calculations, implications, and practical applications.

Understanding Simple Interest

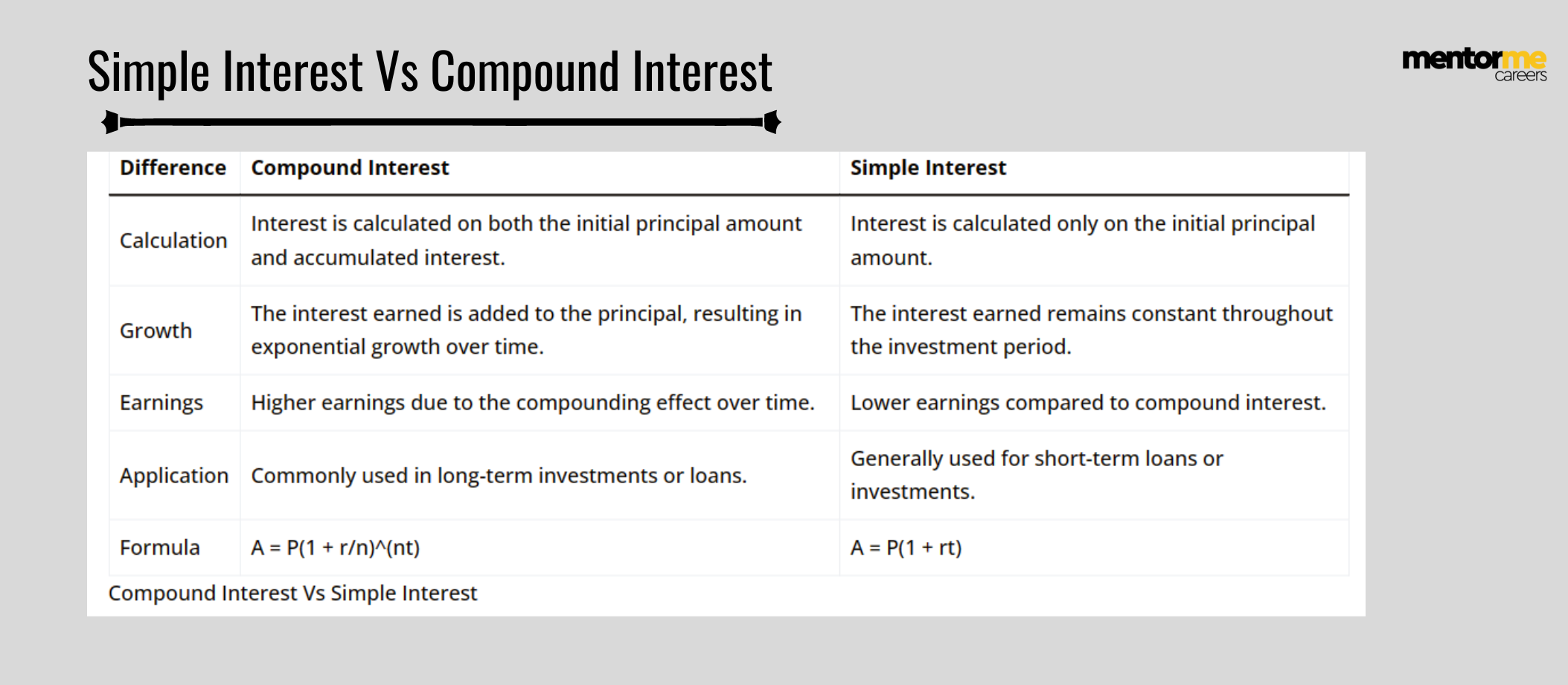

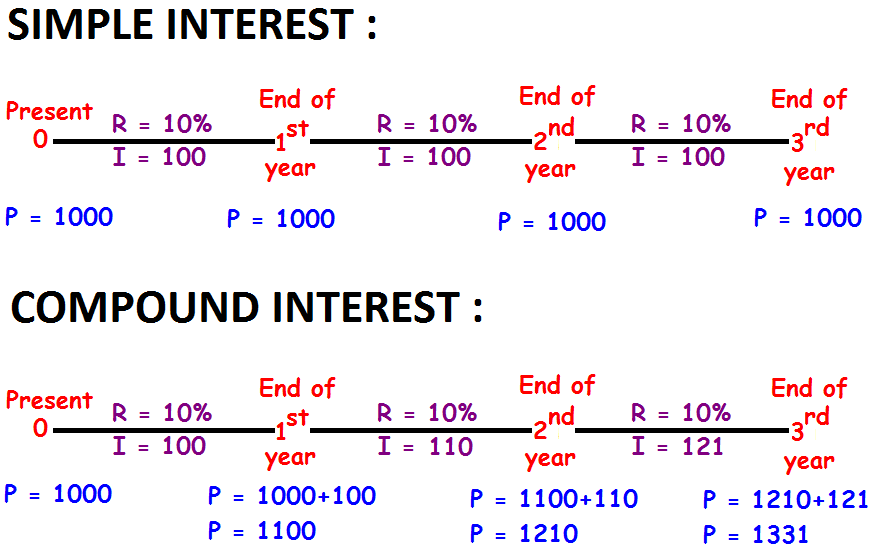

Simple interest is the most straightforward method of calculating interest. It is calculated solely on the initial principal amount of a loan or deposit. This means that the interest earned or paid remains constant over the entire term of the loan or investment. The principal amount never changes in its role as the basis for interest calculation.

The Formula and Calculation of Simple Interest

The formula for simple interest is elegantly uncomplicated:

Simple Interest (SI) = Principal (P) × Rate (R) × Time (T)

Where:

- Principal (P): This is the initial amount of money borrowed or invested.

- Rate (R): This is the annual interest rate, expressed as a decimal. For example, 5% would be written as 0.05.

- Time (T): This is the period for which the money is borrowed or invested, typically expressed in years.

Let’s illustrate with an example. Suppose you invest $1,000 at a simple annual interest rate of 5% for 3 years.

- P = $1,000

- R = 0.05

- T = 3 years

The simple interest earned each year would be:

$1,000 × 0.05 = $50

Over the course of 3 years, the total simple interest earned would be:

$50/year × 3 years = $150

The total amount you would have at the end of 3 years would be the principal plus the accumulated interest:

Total Amount = Principal + Simple Interest

Total Amount = $1,000 + $150 = $1,150

Characteristics of Simple Interest

Several key characteristics define simple interest:

- Constant Interest Accrual: The amount of interest earned or paid each period is always the same. It is directly proportional to the initial principal.

- Linear Growth: If you were to graph the total amount over time, it would form a straight line, indicating a steady, linear increase.

- Predictable Outcome: Because the interest is always based on the original principal, the final amount is easily predictable.

- Less Beneficial for Savers: For individuals saving or investing, simple interest leads to slower wealth accumulation compared to compound interest.

- Easier for Borrowers (in the short term): For borrowers, simple interest can appear more attractive for short-term loans as the interest payments are predictable and don’t escalate.

Practical Applications of Simple Interest

Simple interest is often used in specific financial scenarios:

- Short-Term Loans: Many personal loans, payday loans, or short-term business loans might employ simple interest.

- Certificates of Deposit (CDs): Some CDs, particularly shorter-term ones, might offer simple interest.

- Calculating Interest on Bonds: The interest payments (coupons) on some types of bonds are calculated using simple interest.

- Retail Financing: Interest on certain store credit cards or installment plans can be calculated on a simple interest basis.

While simple interest provides a clear and predictable way to calculate interest costs or earnings, its limitations become apparent when considering longer time horizons and the power of growth.

Exploring Compound Interest

Compound interest, often referred to as “interest on interest,” is where the true magic of financial growth lies. Unlike simple interest, compound interest is calculated on the principal amount and also on the accumulated interest from previous periods. This means that your earnings start earning money themselves, leading to exponential growth over time.

The Mechanics of Compounding

The core idea behind compounding is that your interest is added to your principal, and then the next interest calculation is based on this new, larger sum. This process repeats itself at regular intervals, which can be daily, monthly, quarterly, or annually.

Let’s revisit our previous example, but this time with compound interest. Suppose you invest $1,000 at an annual interest rate of 5%, compounded annually, for 3 years.

-

Year 1:

- Principal = $1,000

- Interest = $1,000 × 0.05 = $50

- Total Amount at end of Year 1 = $1,000 + $50 = $1,050

-

Year 2:

- New Principal (from end of Year 1) = $1,050

- Interest = $1,050 × 0.05 = $52.50

- Total Amount at end of Year 2 = $1,050 + $52.50 = $1,102.50

-

Year 3:

- New Principal (from end of Year 2) = $1,102.50

- Interest = $1,102.50 × 0.05 = $55.13 (rounded)

- Total Amount at end of Year 3 = $1,102.50 + $55.13 = $1,157.63

Comparing this to the simple interest example ($1,150), you can see that compounding earned an extra $7.63 in just three years. While this difference may seem small initially, the impact becomes astronomical over longer periods.

The Compound Interest Formula

The formula for compound interest is a bit more complex than simple interest, as it accounts for the reinvestment of earnings:

A = P (1 + r/n)^(nt)

Where:

- A: The future value of the investment/loan, including interest.

- P: The principal investment amount (the initial deposit or loan amount).

- r: The annual interest rate (as a decimal).

- n: The number of times that interest is compounded per year.

- t: The number of years the money is invested or borrowed for.

Let’s break down what each variable represents and how it influences the outcome:

- Principal (P): The foundational amount from which all interest accrues. A larger principal will naturally lead to larger absolute gains with compounding.

- Annual Interest Rate (r): A higher interest rate means more interest is generated, which in turn fuels faster compounding. Even a small increase in the rate can have a significant long-term impact.

- Compounding Frequency (n): This is a crucial factor. The more frequently interest is compounded (e.g., daily vs. annually), the sooner your interest starts earning its own interest. This accelerates the growth process.

- If compounded annually, n = 1.

- If compounded semi-annually, n = 2.

- If compounded quarterly, n = 4.

- If compounded monthly, n = 12.

- If compounded daily, n = 365.

- Time (t): This is arguably the most powerful variable in compound interest. The longer your money has to compound, the more pronounced the exponential growth becomes. Time allows small initial gains to snowball into substantial amounts.

The “Snowball Effect” and Exponential Growth

The concept of the “snowball effect” is central to understanding compound interest. Imagine a snowball rolling down a hill. As it rolls, it picks up more snow, making it larger. This larger snowball then picks up even more snow at a faster rate, and so on. Compound interest works similarly. Your initial investment is the small snowball, and the interest earned is the snow it collects. As the snowball grows, it collects more snow with each rotation.

The growth of compound interest is exponential, not linear. This means that the rate of growth increases over time. In the early stages, the gains might seem modest, but as the principal and accumulated interest grow, the interest earned in each subsequent period becomes progressively larger. This is why starting early with investing is so often recommended. The power of compounding has more time to work its magic.

Key Differences and Implications

The distinction between simple and compound interest, while subtle in calculation, leads to profoundly different outcomes in financial planning. Understanding these differences is vital for making informed decisions about savings, investments, and loans.

Comparing Growth Over Time

Let’s compare the growth of our initial $1,000 investment at 5% over a longer period, say 30 years, with both simple and compound interest.

Simple Interest:

SI per year = $1,000 × 0.05 = $50

Total Simple Interest over 30 years = $50 × 30 = $1,500

Total Amount = $1,000 (Principal) + $1,500 (Interest) = $2,500

Compound Interest (compounded annually):

Using the formula A = P (1 + r/n)^(nt)

A = $1,000 (1 + 0.05/1)^(1*30)

A = $1,000 (1.05)^30

A = $1,000 × 4.321942

A ≈ $4,321.94

In this scenario, compound interest yields a staggering $1,821.94 more than simple interest over 30 years. This illustrates the dramatic power of reinvesting earnings and the exponential nature of compounding.

Impact on Savings and Investments

For individuals aiming to build wealth through savings and investments, compound interest is their greatest ally.

- Accelerated Wealth Accumulation: The sooner you start saving and investing, the more time compound interest has to work, leading to significantly larger sums over the long term.

- The Power of Reinvestment: Regularly reinvesting dividends, interest payments, and capital gains allows your investments to grow at an accelerated pace.

- Achieving Financial Goals: Compounding is essential for long-term goals like retirement, college savings, or purchasing a home.

Impact on Loans and Debt

The implications of compound interest are equally significant, and often detrimental, when it comes to debt.

- Escalating Debt: When you take out a loan, especially with a high interest rate and frequent compounding, the debt can grow rapidly. If you only make minimum payments on credit cards (which often have high compound interest rates), you might find yourself paying much more in interest than the original purchase price.

- Importance of Paying Down Debt: Understanding compound interest underscores the urgency of paying down high-interest debt as quickly as possible. The longer you carry such debt, the more you will pay in interest.

- Mortgages and Long-Term Loans: While mortgages involve compound interest, the fixed repayment schedule and the principal reduction over time can manage the growth of interest. However, understanding how the interest is calculated in the early years is still important.

When to Use Which Method

The choice between simple and compound interest is rarely a matter of preference but rather dictated by the financial product or agreement. However, understanding the characteristics of each allows for strategic financial decision-making.

Simple Interest Scenarios

Simple interest is most common in situations where:

- Short-Term Transactions: The duration of the financial obligation is relatively brief, minimizing the difference between simple and compound interest.

- Predictable, Fixed Payments: The intention is to have a clear, unchanging interest cost or earning.

- Specific Loan Types: Certain personal loans, auto loans, or short-term business loans might use simple interest.

Compound Interest Scenarios

Compound interest is the default and most powerful mechanism in:

- Savings Accounts and Money Market Accounts: These accounts typically offer interest that compounds, usually monthly or quarterly.

- Certificates of Deposit (CDs): While some CDs might offer simple interest, many offer compounding interest.

- Retirement Accounts (401(k)s, IRAs): The growth within these long-term investment vehicles relies heavily on the power of compounding.

- Stock Market Investments: When you reinvest dividends or capital gains, you are essentially benefiting from compounding returns on your investments.

- Credit Cards and Most Loans: The majority of consumer loans and credit cards utilize compound interest, making it critical to manage debt effectively.

Conclusion: The Power of Compounding for Financial Success

The difference between simple and compound interest is not just a matter of mathematical definition; it represents a fundamental divergence in how money grows or how debt accumulates. Simple interest offers predictability and stability, making it suitable for certain short-term transactions. However, it is compound interest that holds the key to significant wealth creation and long-term financial success. By understanding how interest on interest works, how frequently it is applied, and the impact of time, individuals can make more strategic decisions about saving, investing, and managing their debt. Embracing the power of compounding, starting early, and staying consistent are paramount strategies for achieving financial prosperity.