Understanding the fundamental distinctions between banks and credit unions is crucial for anyone navigating the financial landscape. While both institutions offer a similar array of services—checking accounts, savings accounts, loans, and investment products—their underlying structures, ownership models, and philosophical approaches to technology and innovation diverge significantly. These differences directly impact their service delivery, product development, and the overall customer or member experience, positioning them uniquely in the evolving world of financial technology.

Foundational Structures and Ownership Models

At the core of the bank-credit union dichotomy lies their organizational structure, which dictates their operational priorities, investment strategies in innovation, and ultimately, their approach to serving constituents. This foundational difference profoundly influences how each entity develops and deploys technology.

For-Profit vs. Not-for-Profit Ethos

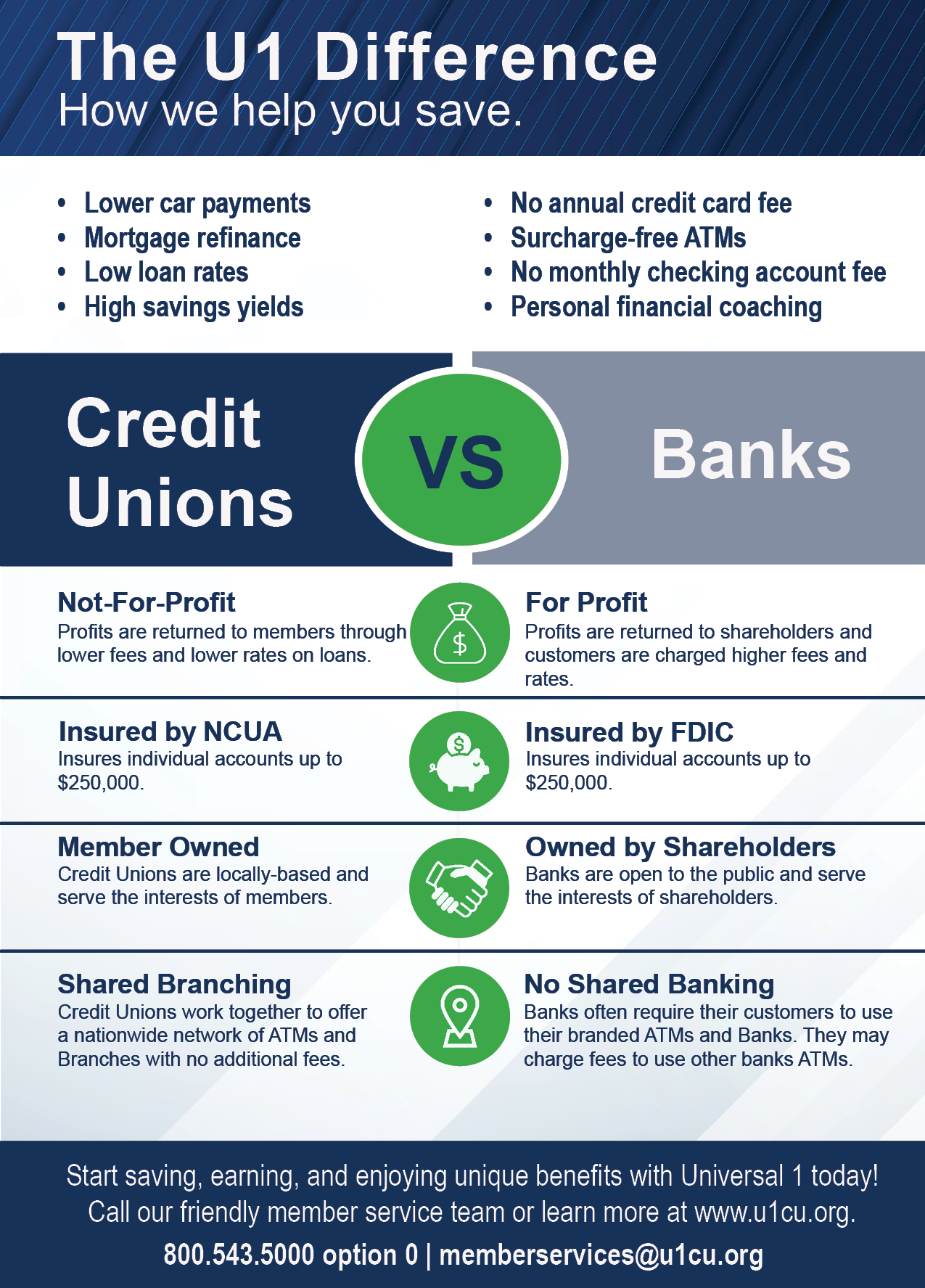

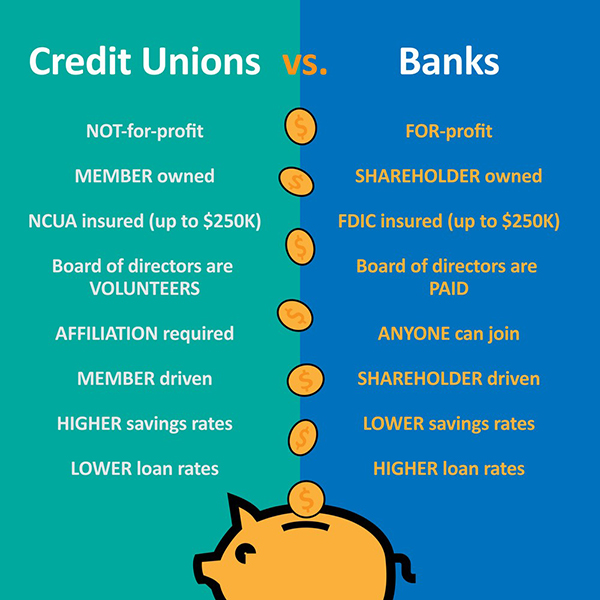

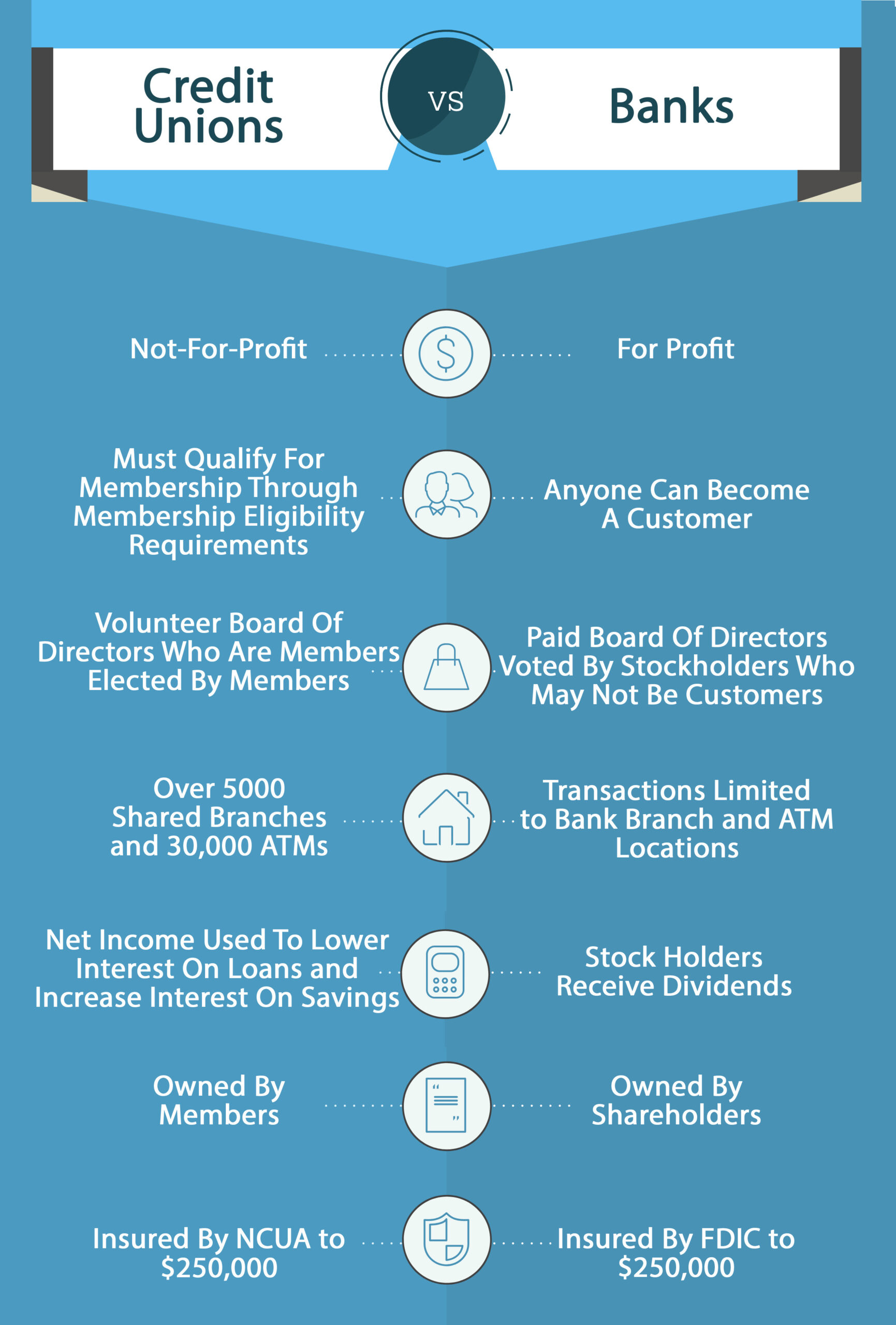

Banks operate primarily as for-profit corporations, owned by shareholders who invest with the expectation of a return on their capital. This shareholder-driven model inherently prioritizes profit maximization. Every strategic decision, including investments in new technologies, digital platforms, and innovative financial products, is typically weighed against its potential to enhance shareholder value. Banks often have access to vast capital pools, enabling significant investments in cutting-edge technology, research and development, and large-scale digital transformation projects aimed at attracting and retaining a broad customer base and optimizing operational efficiencies to boost the bottom line. Their innovation is often geared towards developing proprietary systems, expanding market reach, and offering sophisticated, often fee-generating, services.

Credit unions, conversely, are not-for-profit financial cooperatives. They are owned by their members—the very individuals who use their services. This member-ownership structure means that any profits generated are typically reinvested back into the credit union to benefit members through lower fees, better interest rates on savings, lower loan rates, or improved services. Innovation within credit unions is thus driven by a member-centric ethos rather than a profit motive. Their technological advancements and service enhancements are designed to improve member value and satisfaction. While they may not always command the same scale of capital as large banks for massive tech overhauls, their focus on direct member benefit often leads to agile, tailored innovations that address specific community needs and enhance personal financial well-being. This can manifest in user-friendly mobile apps, personalized financial planning tools, or localized digital services.

Member-Centric vs. Shareholder-Driven Innovations

The differing ownership models lead to distinct approaches to innovation. For banks, innovation is often a competitive advantage in a crowded market. They invest heavily in sophisticated AI-driven analytics for personalized marketing, advanced cybersecurity measures, and expansive digital banking ecosystems that can handle millions of transactions daily. Their scale allows for significant R&D into areas like blockchain for payments, advanced algorithmic trading, and comprehensive wealth management platforms that cater to a global clientele. The imperative is to attract and service a diverse customer base, from retail consumers to large corporations, necessitating a broad and deep technological infrastructure.

Credit unions, being member-owned, tend to foster innovations that directly empower their members. This might involve developing intuitive budgeting tools within their mobile banking apps, offering educational resources integrated with digital platforms, or pioneering more accessible digital loan application processes for underserved communities. Their innovation often emphasizes security, user-friendliness, and transparency, ensuring that technology serves to simplify financial management for their specific membership. While perhaps not always at the forefront of every bleeding-edge financial technology, credit unions often excel in adapting and integrating technologies that enhance the direct member experience, focusing on solutions that deliver clear, tangible value to their individual members rather than optimizing for shareholder returns.

Service Philosophy and Community Engagement

The foundational structures of banks and credit unions significantly influence their service philosophies, particularly concerning community engagement and the localization of innovative solutions. These philosophies, in turn, shape their technological development and deployment strategies.

Localized Innovation and Personalization

Credit unions typically operate with a strong local or community focus. Their membership often derives from a specific geographic area, employer, or association. This inherent community connection drives a service philosophy centered on personalized attention and understanding the unique financial needs of their members. Innovation within this context often manifests as highly tailored solutions. For instance, a credit union might develop a mobile app feature specifically designed to help local small businesses manage their finances, or integrate a digital platform that facilitates access to community-specific grants or loan programs.

Their technology often aims to deepen member relationships, not just process transactions. This could include AI-powered chatbots trained on local FAQs, or digital tools for financial literacy that are culturally relevant to their community. The size and localized nature of many credit unions allow for greater agility in testing and implementing these niche technological innovations. They can often receive direct feedback from members and iterate quickly, leading to digital services that feel more integrated into the community’s fabric. This member-centric approach encourages technology that fosters financial well-being and strengthens local economic ties.

Broad Market Reach and Standardized Offerings

In contrast, most banks, particularly larger ones, aim for a broad market reach, serving customers across regions, nationally, and even globally. Their service philosophy is often designed to provide consistent, standardized experiences across a vast and diverse customer base. Technological innovation for banks, therefore, frequently focuses on scalability, robustness, and universal applicability. This means investing in enterprise-level systems that can handle millions of users, developing mobile banking platforms with feature parity across different operating systems, and building extensive ATM networks.

Their digital solutions prioritize efficiency and convenience for a general population, such as universal payment systems, sophisticated fraud detection algorithms, and self-service digital onboarding processes. While banks do offer personalized services, especially for high-net-worth clients, their mass-market offerings are designed for broad appeal and operational efficiency at scale. Their technological advancements are geared towards capturing market share, streamlining operations across vast networks, and offering a comprehensive suite of services that can compete on a national or international level. The innovation here is about global reach and consistent quality, leveraging technology to manage a massive customer ecosystem efficiently.

Technological Adoption and Digital Transformation

The pace and nature of technological adoption and digital transformation vary significantly between banks and credit unions, primarily due to their different scales, regulatory environments, and underlying business models.

Agility in Fintech Integration

Credit unions, often smaller and with fewer bureaucratic layers, can sometimes exhibit greater agility in integrating new financial technologies (Fintech) that complement their member-centric approach. While they may not always be pioneers in developing entirely new technologies from scratch, they are frequently adept at adopting and customizing existing Fintech solutions. This might involve partnering with third-party providers for advanced mobile payment systems, personal finance management (PFM) tools, or blockchain-based solutions for secure data sharing. Their ability to make quicker decisions and adapt to changing member needs allows them to implement innovative solutions that enhance member experience or operational efficiency without the extensive corporate approvals required by larger institutions.

The focus here is often on seamless integration of user-friendly technologies that offer tangible benefits to members, such as simplified online loan applications, enhanced digital security features, or improved accessibility for mobile banking. This targeted adoption of technology allows credit unions to punch above their weight, providing members with modern digital services that might rival those of larger banks, but with a more personalized, localized feel.

Scale and Investment in Digital Infrastructure

Banks, especially large national and international ones, have the capital and resources to invest massively in their own proprietary digital infrastructure and research and development. Their digital transformation initiatives are often multi-year, multi-billion-dollar projects aimed at overhauling legacy systems, building robust cloud-based platforms, and developing cutting-edge artificial intelligence and machine learning capabilities. They are at the forefront of developing sophisticated algorithms for fraud detection, predictive analytics for market trends, and advanced digital wealth management tools.

Their scale allows them to attract top tech talent and build dedicated innovation labs. The result is often a highly integrated digital ecosystem that offers a vast array of services, from complex investment platforms to real-time international transfers. While this scale can sometimes lead to slower decision-making and implementation cycles for certain innovations due to regulatory complexities and the sheer size of their operations, it ultimately allows them to deliver a comprehensive, globally accessible, and highly resilient digital banking experience. Their innovation is about pushing the boundaries of what’s possible in financial services, often leading to industry-wide standards and advancements.

Product Offerings and Accessibility

The unique structures and philosophies of banks and credit unions influence not only their approach to technology but also the range and accessibility of the financial products they offer to their respective customer bases.

Tailored Solutions and Niche Markets

Credit unions, with their member-owned model and often localized focus, frequently excel at providing financial products and services that are specifically tailored to the needs of their defined membership or community. Their innovation in this area centers on creating solutions that might not be profitable for larger banks but are highly valuable to their niche markets. This can include flexible loan options for individuals with less-than-perfect credit, specialized savings programs linked to community initiatives, or financial education workshops integrated into their digital platforms for young families or first-time homebuyers.

Technologically, this often translates into more adaptable digital application processes, personalized advisory tools, and mobile features designed to support specific member demographics. For example, a credit union serving a particular industry might offer industry-specific business banking tools through its online portal. Their innovation is about depth and relevance to their members, ensuring accessibility to essential financial services and fostering financial inclusion within their chosen communities. Decisions about new product offerings are often made with direct member feedback, allowing for a more responsive and targeted innovation cycle.

Comprehensive Portfolios and Global Access

Banks, particularly larger ones, aim to offer a comprehensive portfolio of financial products and services designed to appeal to the broadest possible market. Their product innovation is often driven by market demand and competition, striving to provide a one-stop shop for all financial needs, from basic checking accounts to complex derivatives, international trade finance, and extensive wealth management services. This breadth requires robust technological infrastructure capable of managing diverse product lines, intricate regulatory compliance, and sophisticated risk management.

Digital platforms from banks are designed for universal functionality, offering everything from mobile check deposit and bill pay to advanced investment tools and foreign currency exchange, often with global accessibility. Their scale allows them to develop and market highly specialized products that require significant investment in technology and expertise, such as complex derivatives, large-scale commercial lending platforms, or sophisticated cash management solutions for multinational corporations. The innovation here is about expanding the spectrum of financial services, making them accessible and efficient for a global clientele through advanced digital channels.

Regulatory Landscape and Consumer Protection

While both banks and credit unions are heavily regulated, the specific regulatory bodies and the implications for consumer protection, and subsequently their approach to technology, can differ.

Federal Oversight and Insured Deposits

In the United States, both banks and credit unions are subject to federal regulation to ensure stability and protect consumers. Banks are primarily regulated by agencies such as the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and the Federal Deposit Insurance Corporation (FDIC). The FDIC insures deposits up to $250,000 per depositor, per institution, ensuring the safety of funds. This robust regulatory environment mandates significant investments in compliance technology, cybersecurity, and data privacy, particularly for larger banks dealing with vast amounts of sensitive customer data across complex systems.

Innovation in banks within this context often involves developing sophisticated regtech (regulatory technology) solutions to automate compliance, enhance fraud detection, and manage systemic risk. They invest in advanced encryption, biometric authentication, and secure network infrastructures to meet stringent regulatory requirements and protect customer assets. The emphasis on robust, compliant technology is paramount, influencing everything from system architecture to customer onboarding processes.

Governance and Member Accountability

Credit unions are typically regulated by the National Credit Union Administration (NCUA), which provides deposit insurance through the National Credit Union Share Insurance Fund (NCUSIF), also up to $250,000 per member, per institution. While subject to similar consumer protection laws as banks, the cooperative governance structure of credit unions adds another layer of accountability directly to their members. This often fosters a high degree of transparency in their operations and technology deployments.

Innovation in credit unions, while still adhering to strict federal regulations, can also be influenced by member feedback on security features, data privacy controls, and the accessibility of digital services. Their technological investments prioritize solutions that are trustworthy, easy to understand, and directly serve the financial well-being of their members, often with a strong emphasis on community trust and ethical data handling. This member-driven accountability encourages the adoption of technologies that are not only compliant but also perceived as highly beneficial and secure by their specific membership base, fostering a culture of innovation that balances regulatory adherence with direct member value.