The landscape of retirement savings can often feel like navigating a complex financial maze, with various account types and acronyms designed to help individuals plan for their golden years. Among the most common and important are the 401(k) and 457 plans, both offered by employers to facilitate tax-advantaged savings. While they share the fundamental goal of accumulating wealth for retirement, significant distinctions exist in their eligibility, withdrawal rules, and specific benefits. Understanding these differences is crucial for making informed decisions about where to allocate your retirement savings, especially if you are fortunate enough to have access to both types of plans.

Understanding the Core Purpose and Structure

At their heart, both 401(k) and 457 plans are employer-sponsored retirement savings vehicles. They allow employees to contribute a portion of their salary on a pre-tax basis, which means the money contributed is deducted from your gross income, thereby lowering your current taxable income. The investments within these plans then grow tax-deferred, meaning you don’t pay taxes on the earnings until you withdraw the money in retirement. This dual benefit of immediate tax relief and tax-deferred growth is the cornerstone of their appeal.

The 401(k) Plan: A Mainstay for Private Sector Employees

The 401(k) plan is arguably the most widely recognized retirement savings vehicle in the United States. It is predominantly offered by private sector companies. The “401(k)” designation comes from the section of the Internal Revenue Code that governs these plans.

Key Characteristics of a 401(k):

- Employer-Sponsored: Primarily found in the private sector, though some non-profit organizations also offer them.

- Pre-Tax Contributions: Funds are deducted from your paycheck before federal and state income taxes are calculated.

- Tax-Deferred Growth: Investment earnings are not taxed until withdrawal.

- Contribution Limits: The IRS sets annual limits on how much individuals can contribute. These limits are adjusted periodically for inflation. For example, in 2023, the employee contribution limit was $22,500, with an additional $7,500 catch-up contribution allowed for those aged 50 and over.

- Employer Match: A significant advantage of many 401(k) plans is the potential for an employer match. This is essentially free money contributed by your employer, often a percentage of your salary, up to a certain limit. This can dramatically accelerate your retirement savings.

- Withdrawal Rules: Generally, withdrawals before age 59½ are subject to a 10% early withdrawal penalty, in addition to ordinary income tax. Exceptions exist for certain circumstances, such as disability or separation from service.

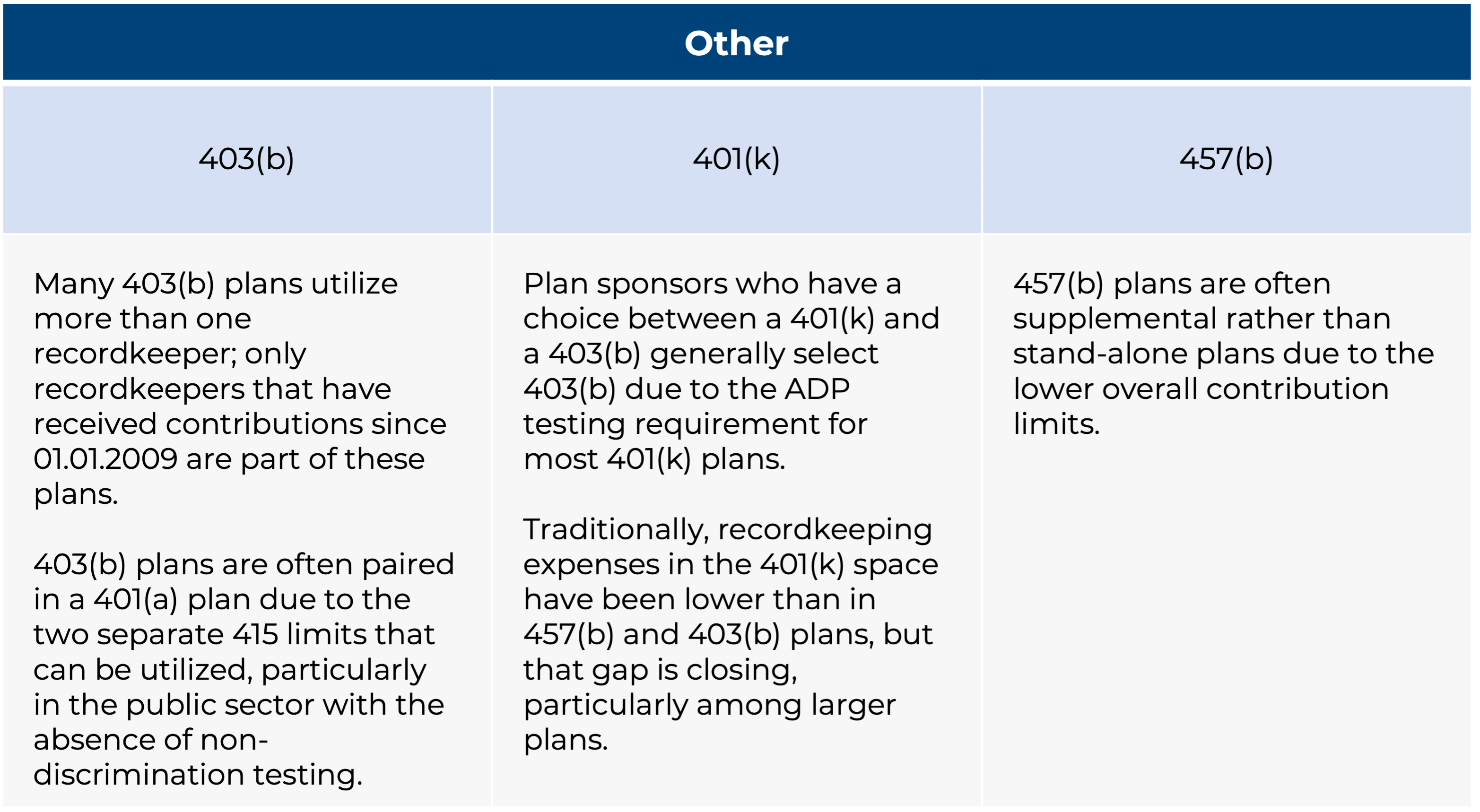

- Loan Provisions: Many 401(k) plans allow participants to take loans against their vested balance, which must be repaid with interest.

- Rollover Options: Upon leaving an employer, 401(k) funds can typically be rolled over into an Individual Retirement Account (IRA) or into a new employer’s 401(k) plan without incurring taxes or penalties.

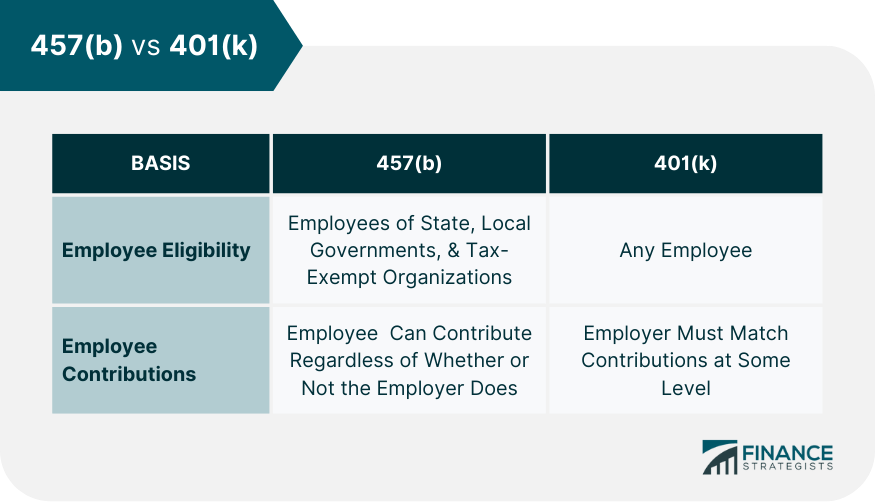

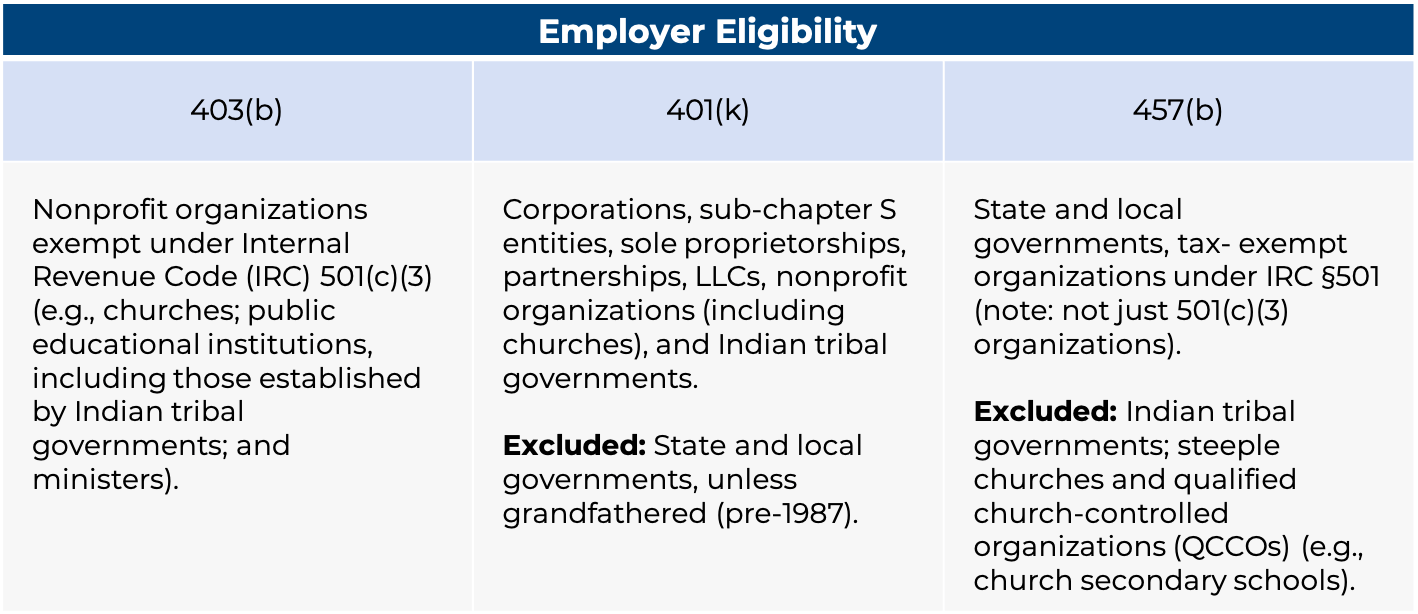

The 457 Plan: A Parallel Path for Public Sector and Select Non-Profits

The 457 plan, also named after a section of the Internal Revenue Code, serves a similar purpose to the 401(k) but is primarily available to employees of state and local governments, as well as certain tax-exempt organizations. It offers a compelling alternative or, in some cases, a complementary savings option.

Key Characteristics of a 457 Plan:

- Employer-Sponsored: Primarily offered to employees of state and local governments (e.g., teachers, police officers, firefighters, municipal workers) and employees of certain tax-exempt organizations (e.g., hospitals, charities).

- Pre-Tax Contributions: Similar to 401(k)s, contributions are made pre-tax, reducing current taxable income.

- Tax-Deferred Growth: Earnings grow tax-deferred until withdrawal.

- Contribution Limits: 457 plans have their own annual contribution limits, which are often similar to 401(k) limits. For 2023, the employee contribution limit was $22,500, with an additional $7,500 catch-up contribution for those aged 50 and over.

- Special Withdrawal Rule: No 10% Early Withdrawal Penalty: This is a critical distinction. Unlike 401(k)s, withdrawals from a 457 plan are generally not subject to the 10% early withdrawal penalty, regardless of age, as long as the funds are withdrawn after separation from service. This can provide valuable flexibility for those planning to retire or leave their employer before age 59½.

- Employer Match: Employer matches are less common in 457 plans compared to 401(k)s, but they do exist, particularly in governmental 457(b) plans.

- Rollover Options: Funds from a 457 plan can typically be rolled over into an IRA or another eligible retirement plan.

Key Differences and Strategic Considerations

While both 401(k) and 457 plans are powerful tools, their differences dictate how individuals might strategically utilize them for their retirement planning.

Eligibility and Availability

The most fundamental difference lies in who is eligible for each plan.

- 401(k) Plans: The vast majority of employees in the private sector will encounter 401(k) plans as their primary employer-sponsored retirement savings option.

- 457 Plans: These are exclusive to employees of governmental entities and certain non-profit organizations. If you work for a state or local government, or a qualifying tax-exempt organization, you might be eligible for a 457 plan.

Withdrawal Flexibility and Penalties

The early withdrawal rules represent one of the most significant practical distinctions.

- 401(k)s: Subject to a 10% early withdrawal penalty if funds are withdrawn before age 59½, unless an exception applies. This encourages long-term savings and discourages premature access to funds.

- 457(b) Plans: Generally, withdrawals from a 457(b) plan are not subject to the 10% early withdrawal penalty. This flexibility can be a major advantage for individuals who anticipate needing access to their retirement funds before the traditional retirement age of 59½, perhaps for early retirement or to cover unexpected expenses.

It’s important to note that the penalty-free withdrawal rule for 457(b) plans applies to the separation from service. This means that once you leave your employer, you can access the funds without the 10% penalty. The funds are still subject to ordinary income tax, of course.

Contribution Limits: The “Stacking” Advantage

For those fortunate enough to be eligible for both a 401(k) and a 457 plan (which can occur for some public sector employees or those who work for multiple employers over their careers), there’s a strategic advantage regarding contribution limits.

- Separate Limits: The IRS treats the contribution limits for 401(k) plans and 457 plans as separate. This means that if you contribute the maximum to your 401(k), you can also contribute the maximum to your 457 plan, effectively allowing you to save more on a pre-tax basis each year than someone who only has access to one type of plan.

- Example: In 2023, if you were eligible for both, you could contribute $22,500 to your 401(k) and another $22,500 to your 457 plan, for a total of $45,000 in pre-tax contributions. This significantly accelerates wealth accumulation.

Loan Provisions

- 401(k)s: Loan provisions are relatively common in 401(k) plans. While borrowing against your retirement savings should be approached with caution, it can offer a way to access funds for emergencies or major purchases without triggering taxes or penalties, provided the loan is repaid as per the plan’s terms.

- 457 Plans: Loan provisions are less common in 457 plans, particularly in governmental 457(b) plans. However, some non-governmental 457(b) plans may offer loan options.

Vesting Schedules

Both plan types can have vesting schedules. Vesting refers to the process by which you earn the right to keep your employer’s contributions to your retirement account.

- 401(k)s: Often feature graded or cliff vesting schedules. For example, you might be 20% vested after one year of service, 40% after two years, and so on, until you are 100% vested after five years (graded vesting). Alternatively, you might have to wait a specific period, say three years, to be 100% vested (cliff vesting).

- 457 Plans: Can also have vesting schedules, though some governmental 457(b) plans may have immediate 100% vesting for employer contributions.

Investment Options

The breadth and quality of investment options can vary significantly between individual 401(k) and 457 plans, regardless of the plan type itself.

- 401(k)s: Typically offer a range of mutual funds, target-date funds, and sometimes company stock.

- 457 Plans: Investment options can also include mutual funds and target-date funds. The specifics depend on the plan administrator and the employer. It’s always advisable to review the plan’s investment lineup to ensure it aligns with your risk tolerance and financial goals.

Navigating Your Retirement Savings Strategy

For individuals working in the private sector, the 401(k) is likely to be their primary retirement savings vehicle. The allure of an employer match is a strong incentive to contribute at least enough to capture the full match. Beyond that, understanding the contribution limits and the long-term benefits of tax-deferred growth is paramount.

For public sector employees or those in tax-exempt organizations, the 457 plan offers a unique set of advantages, most notably the penalty-free withdrawal option upon separation from service. This can be a powerful tool for those planning early retirement. If eligible for both a 401(k) and a 457 plan, maximizing contributions to both can significantly boost retirement savings due to the separate contribution limits.

Considerations for Those Eligible for Both

If you find yourself eligible for both a 401(k) and a 457 plan, a strategic approach is recommended:

- Prioritize the Employer Match: If your 401(k) offers an employer match, contribute enough to get the full match. This is essentially a guaranteed return on your investment.

- Maximize 457 Contributions for Flexibility: Consider prioritizing contributions to your 457 plan if you anticipate needing access to funds before age 59½ due to the lack of the 10% early withdrawal penalty.

- Maximize Both if Possible: If your financial situation allows and you don’t anticipate needing funds early, maximizing contributions to both plans is an excellent way to supercharge your retirement savings and take advantage of the separate contribution limits.

- Review Investment Options: Compare the investment choices offered in both plans. Sometimes, one plan may offer superior investment options or lower fees, which can influence your allocation decisions.

- Understand Rollover Rules: Be clear on how and when you can roll over funds from either plan when you change employers to maintain tax-deferred status.

In conclusion, while both 401(k) and 457 plans are designed to help individuals save for retirement in a tax-advantaged manner, their differences in eligibility, withdrawal penalties, and contribution treatment present distinct strategic opportunities. A thorough understanding of these nuances empowers individuals to make the most effective choices for securing their financial future.