As the drone industry transitions from a hobbyist’s playground into a cornerstone of industrial innovation, the intersection of high-end technology and financial regulation has become increasingly complex. For professionals operating in the realms of Tech & Innovation—specifically those utilizing remote sensing, AI-driven autonomous flight, and advanced mapping—the arrival of the 2025 tax season is more than just a date on the calendar. It represents a critical window for leveraging the massive capital investments required to stay competitive in the rapidly evolving Unmanned Aerial Vehicle (UAV) sector.

Understanding the deadline to file taxes in 2025 is the first step in a strategic financial plan that allows drone tech companies to reinvest in R&D, upgrade their sensor arrays, and scale their autonomous fleet operations. This guide explores the essential deadlines, tax incentives, and compliance requirements tailored specifically for the drone innovation niche.

Understanding the 2025 Tax Landscape for the Drone Tech Industry

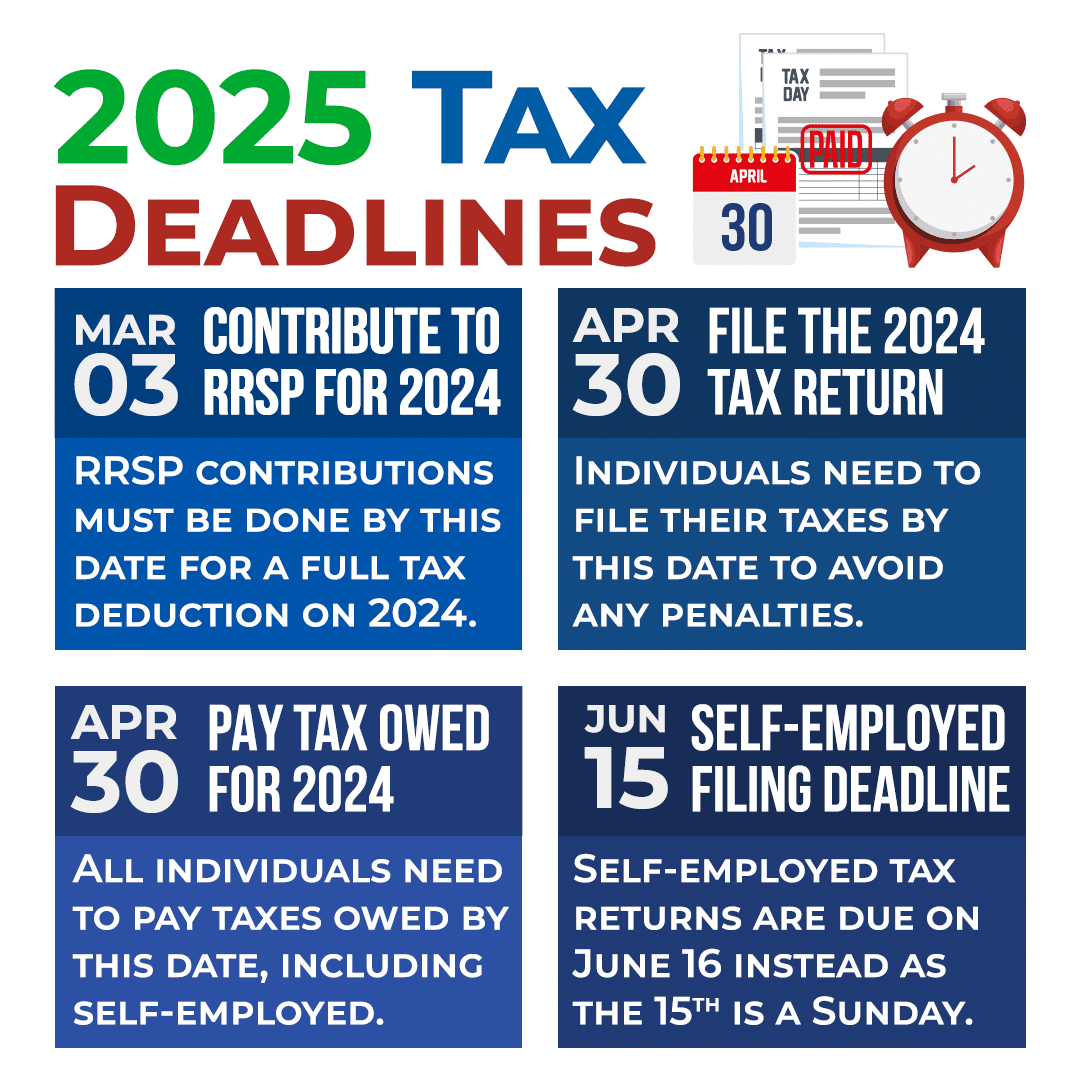

For the 2025 tax season (covering income and expenses incurred during the 2024 calendar year), the standard deadline for individual filers and most corporations is Tuesday, April 15, 2025. However, in the world of high-tech innovation and remote sensing, “the deadline” is rarely a single date. Depending on your business structure and the nature of your innovation projects, multiple dates may dictate your fiscal health.

Key Deadlines for Remote Sensing Startups and Innovators

If you are operating as an S-Corporation or a Partnership—common structures for boutique drone mapping firms and software developers—your primary deadline is actually March 17, 2025 (since March 15 falls on a weekend). For these entities, filing on time is crucial to ensure that K-1 forms are distributed to shareholders, who then must report that data on their personal returns by the April 15 deadline.

For innovators working as independent contractors or “solopreneurs” in the mapping and sensing space, the April 15 deadline is the final cutoff to settle any remaining balances for the 2024 tax year. However, it is important to remember that the tech industry often relies on quarterly estimated tax payments. To avoid penalties before the 2025 deadline, drone professionals must have made payments throughout 2024, with the final estimated payment for the fourth quarter due on January 15, 2025.

Why the 2025 Filing Year is Different for AI and Mapping Innovators

The 2025 tax season arrives at a time when the federal government is increasingly interested in “Dual-Use” technology—tech that has both civilian and defense applications. Drone tech involving autonomous flight and advanced mapping often falls into this category. Consequently, there are shifting perspectives on how software development costs (particularly those related to AI and machine learning for flight stabilization) are amortized.

Recent changes in Section 174 of the tax code require businesses to amortize research and experimentation (R&E) expenses over five years rather than deducting them in the year they were incurred. For a drone tech startup developing a proprietary AI follow-mode or a new remote sensing algorithm, this change makes meeting the 2025 deadline even more critical, as the calculation of taxable income may be higher than in previous years, requiring more sophisticated cash flow management.

Maximizing Tax Deductions for Drone Hardware and Software Innovation

In the niche of Tech & Innovation, the hardware is often the most significant expense. High-precision LiDAR (Light Detection and Ranging) sensors, multispectral cameras for agricultural sensing, and heavy-lift UAV platforms represent capital investments that can reach hundreds of thousands of dollars. As you approach the 2025 tax deadline, understanding how to write off these assets is paramount.

Section 179 Deductions for LiDAR and Mapping Equipment

One of the most powerful tools for drone professionals is the Section 179 deduction. This allows businesses to deduct the full purchase price of qualifying equipment bought or financed during the tax year. For example, if a mapping firm purchased a $50,000 LiDAR-equipped drone in 2024 to enhance their remote sensing capabilities, they may be able to deduct the entire $50,000 from their 2024 gross income, provided the equipment is put into service before December 31, 2024.

This is particularly relevant for the 2025 filing because the deduction limit and the “total equipment purchased” threshold are adjusted for inflation annually. Utilizing Section 179 effectively can significantly reduce the tax burden for drone innovators, essentially providing a “discount” on the next generation of mapping tech through tax savings.

R&D Tax Credits for Autonomous Flight Software Development

Innovation isn’t just about the hardware; it’s about the code that makes the hardware intelligent. If your business is focused on developing AI-driven autonomous flight paths, obstacle avoidance systems, or specialized mapping software, you likely qualify for the Research and Development (R&D) Tax Credit.

Unlike a deduction, which lowers your taxable income, a credit is a dollar-for-dollar reduction of your actual tax bill. To claim this before the 2025 deadline, you must document the “Four-Part Test”:

- Permissible Purpose: The activity must relate to a new or improved function, performance, reliability, or quality.

- Elimination of Uncertainty: You must have been trying to discover information that would eliminate technical uncertainty.

- Process of Experimentation: You must have evaluated alternatives or used a systematic trial-and-error process.

- Technological in Nature: The research must rely on hard sciences like computer science, engineering, or physics.

For drone tech innovators, the process of refining an AI’s ability to navigate through complex urban environments (remote sensing and obstacle avoidance) almost always meets these criteria.

Compliance and Asset Management for Commercial Remote Sensing Fleets

As the 2025 tax deadline approaches, drone tech companies must reconcile their physical assets with their financial records. In the niche of Tech & Innovation, drone equipment is subject to rapid obsolescence, which means the way you handle depreciation is vital for long-term sustainability.

Depreciation Schedules for High-Tech Sensor Arrays

While Section 179 offers an immediate write-off, some businesses prefer Modified Accelerated Cost Recovery System (MACRS) depreciation. Most commercial drones and sensing equipment fall under a 5-year property category. However, because drone technology moves so fast, a 5-year schedule may not accurately reflect the “useful life” of a sensor that becomes obsolete in three years.

When filing by the 2025 deadline, tech-focused firms should consult with a specialist to determine if “Bonus Depreciation” is applicable. For assets placed in service in 2024, bonus depreciation allows for a 60% immediate deduction, which is a step down from the 80% available in 2023. This phase-out makes it even more important to accurately track the date of purchase and the date the tech was first used for a commercial mapping mission.

Tracking Business Use of AI-Integrated Drone Systems

A common pitfall for smaller drone innovators is the “mixed-use” trap. If a drone is used for both experimental R&D and occasionally for personal aerial filming, the tax implications change. To ensure compliance by the April 15, 2025 deadline, professionals must maintain rigorous flight logs. Modern drone apps and fleet management software (like AirData or DJI FlightHub 2) are essential tools here. They provide the “Tech & Innovation” professional with a digital paper trail, proving that 100% of the drone’s flight time was dedicated to commercial remote sensing or AI training, thereby justifying the full business deduction.

Strategic Financial Planning Beyond the April 15 Deadline

Meeting the 2025 tax deadline is a milestone, but for those in the high-stakes world of drone innovation, the work doesn’t end in April. True innovation requires a forward-looking financial strategy that anticipates the needs of the 2026 fiscal year and beyond.

Extensions and Quarterly Estimated Payments for Tech Contractors

If the complexity of your R&D tax credits or international sensor supply chain makes the April 15 deadline impossible, you can file for an extension. This moves the filing deadline to October 15, 2025. However, a common misconception in the tech world is that an extension to file is an extension to pay. Any taxes owed for the 2024 tax year must still be paid by April 15 to avoid interest and late-payment penalties.

For tech contractors specializing in remote sensing for agriculture or infrastructure, 2025 will also require a focus on “safe harbor” payments. To avoid underpayment penalties, you should aim to pay at least 90% of your 2024 tax liability or 100% of your 2023 tax liability through estimated payments throughout the year.

Long-term Investment in Drone Innovation and Capital Gains

Finally, for drone tech founders looking to exit or bring on venture capital, the 2025 tax season is a time to evaluate Qualified Small Business Stock (QSBS). If your drone innovation company is structured as a C-Corp and meets certain criteria, you may be eligible to exclude a significant portion of capital gains from the sale of your stock. This is a powerful incentive for tech innovators to build long-term value in the remote sensing and AI sectors, as it rewards the high risk associated with pioneering new flight technologies.

In conclusion, while the deadline to file taxes in 2025 is a standard date for the general public, it is a nuanced and strategic deadline for the drone tech community. By focusing on Section 179, R&D credits, and precise asset depreciation, innovators can ensure that their financial flight path is as stable and efficient as their most advanced autonomous systems. Staying ahead of the IRS allows you to keep your eyes where they belong: on the horizon of what’s next in UAV technology.