The American Express (Amex) Card Verification Value (CVV) is a critical security feature designed to protect cardholders from fraud during online and telephone transactions. Unlike some other card networks that refer to this as a CVC (Card Verification Code) or CSC (Card Security Code), American Express specifically uses the term CVV. Understanding its purpose, location, and proper usage is paramount for both consumers and merchants engaging in e-commerce and remote transactions. This article delves into the intricacies of the Amex CVV, its significance in safeguarding financial data, and how it functions within the broader ecosystem of secure payment processing.

The Amex CVV: A Deeper Dive into its Functionality and Significance

The CVV on an American Express card is more than just a string of numbers; it’s a vital component of the payment processing security infrastructure. Its primary role is to act as a deterrent against fraudulent transactions by providing an additional layer of verification that is not stored by merchants after the transaction is authorized. This is a key distinction from the Primary Account Number (PAN), expiration date, and cardholder name, which are essential for processing transactions and are sometimes retained by merchants for future reference or recurring billing. The CVV, however, is intended to be a one-time-use code for a given transaction, making it a powerful tool against the exploitation of stolen card details.

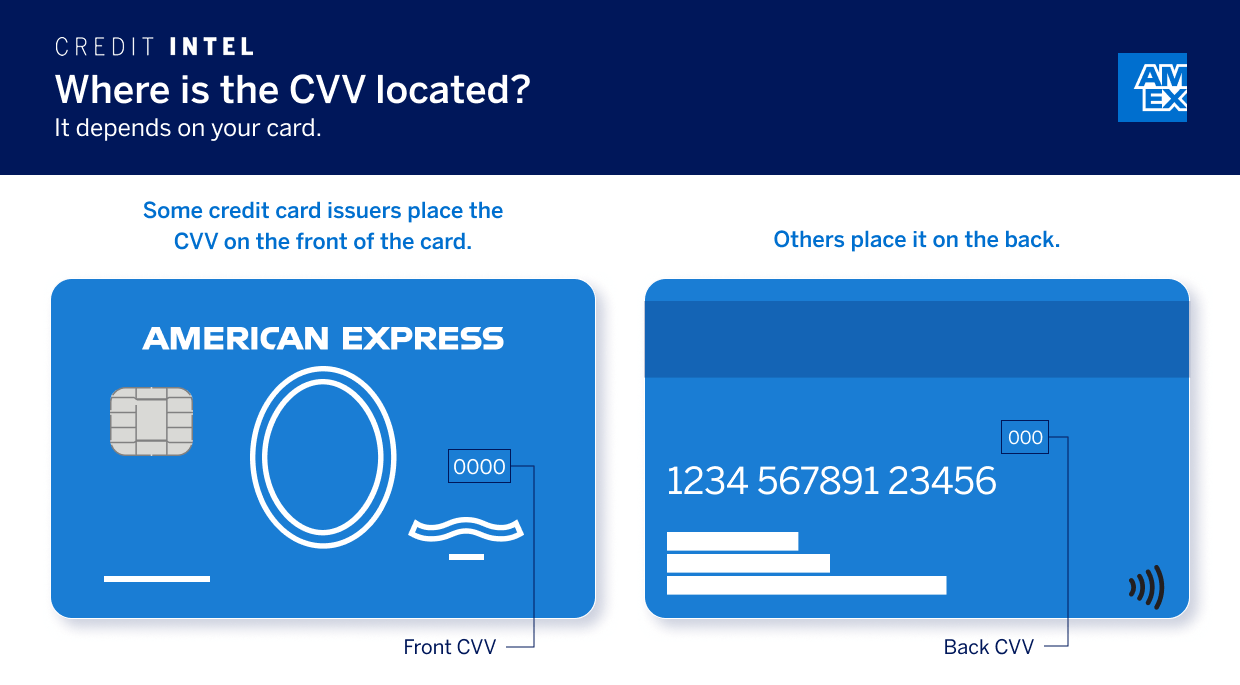

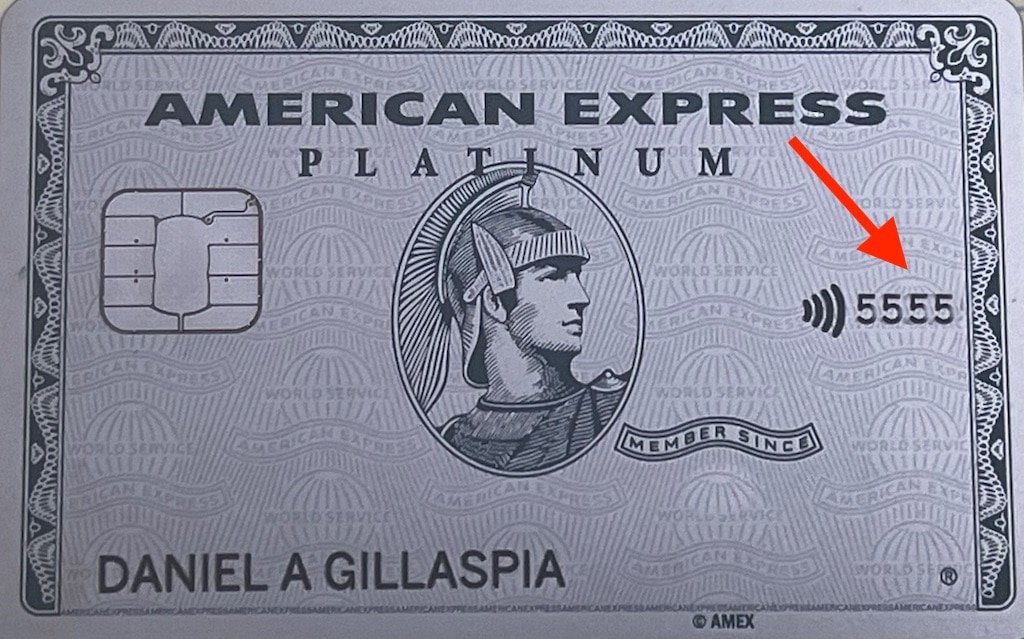

The security offered by the CVV is rooted in its generation and its intended use. It is a unique three-digit code embossed on the front of the American Express card, positioned to the right of the embossed account number. This physical placement is a deliberate design choice. It means that a fraudster would need to physically possess the card to obtain the CVV. This significantly mitigates the risk of online data breaches where card numbers and expiration dates might be compromised without the physical card being stolen. While magnetic stripe data can be skimmed without physical possession, the CVV is not typically stored on the magnetic stripe and thus remains more secure against such attacks.

The underlying technology that powers the CVV system is complex, involving algorithms developed by American Express and other card networks to generate and verify these codes. When a cardholder enters their CVV during an online transaction, this code is transmitted to the payment processor along with the other transaction details. The processor then sends this information, including the CVV, to American Express for verification. American Express compares the CVV provided with the one stored in its secure databases, which are linked to the specific card account. If the CVV matches, the transaction is deemed more likely to be legitimate. If it doesn’t match, the transaction may be declined, prompting further investigation or a manual review.

This verification process is crucial because it helps to establish that the person making the purchase is likely in physical possession of the card. While it’s not an infallible system – sophisticated fraudsters may still manage to obtain the CVV through other means, such as phishing scams or malware – it significantly raises the bar for fraudulent activities. The CVV is a testament to the continuous efforts by financial institutions and card networks to evolve their security protocols in response to emerging threats in the digital landscape.

Understanding the CVV’s Location and Format

For American Express cardholders, locating the CVV is a straightforward process, though it differs slightly from how it appears on other major credit card brands. The Amex CVV is a distinct three-digit number. Unlike Visa and Mastercard, which typically place their CVV on the back of the card, American Express prints its CVV on the front of the card. It is located to the right of the embossed card account number. This placement, while seemingly minor, is a distinguishing characteristic of American Express cards and a key identifier for cardholders.

The three digits are usually presented in a clean, embossed format, consistent with the other account details on the card. It is important for cardholders to familiarize themselves with this location to ensure they are entering the correct code during online purchases. Misplacing or misinterpreting this number can lead to transaction failures, which can be frustrating.

The format of the Amex CVV is consistently three digits. This is a crucial detail that differentiates it from the four-digit security code found on the back of most other credit and debit cards. When prompted for a CVV on a website or through a payment gateway, Amex users must ensure they are inputting the correct three-digit number from the front of their card. Entering a four-digit number, or the wrong three-digit number, will result in an authentication failure.

This unique placement and format also serve as a subtle security measure. It means that even if a merchant’s system were compromised and card numbers were stolen, the associated CVVs would not necessarily be obtained from the same data set if the breach focused solely on rear-card magnetic stripe data. While the CVV is transmitted and processed, the intention is for it not to be stored permanently by the merchant, thereby limiting the long-term risk associated with a data compromise.

The Role of the CVV in Online and Telephone Transactions

The CVV plays a pivotal role in ensuring the security of transactions conducted without the physical presence of the card. These are often referred to as Card-Not-Present (CNP) transactions. The digital economy relies heavily on the ability to conduct commerce remotely, and the CVV is a cornerstone of trust in these interactions.

Online Transactions

In the realm of e-commerce, the CVV is typically requested during the checkout process. After a customer enters their card number, expiration date, and billing address, they will be prompted to enter the CVV. This step is crucial for verifying that the customer has physical possession of the card at the time of purchase. Online retailers are prohibited by payment card industry standards (PCI DSS) from storing the CVV after the transaction has been authorized. This policy is a critical safeguard against the widespread misuse of card details should a merchant’s database be breached. Without the CVV, stolen card numbers and expiration dates are significantly less useful for making fraudulent purchases.

The CVV acts as a dynamic security check for each transaction. It’s not a static piece of information that, once compromised, remains a perpetual threat in the same way a stolen card number might be. By requiring it for each CNP transaction, and prohibiting its storage, Amex and other networks ensure that the CVV’s utility for fraudsters is limited to the specific moment of a transaction. If the CVV is compromised during a single transaction, it cannot be reused for future fraudulent purchases from the same merchant if the merchant adheres to security protocols.

Telephone Transactions

Similarly, when a customer makes a purchase over the phone, the merchant will often ask for the CVV. This is another form of a Card-Not-Present transaction. The agent taking the order will verbally request the three-digit code from the customer. As with online transactions, the merchant is obligated not to store this CVV after the transaction is completed. This prevents scenarios where a call center employee could misuse a customer’s card details at a later time. The CVV provides an essential layer of assurance that the individual providing the card details over the phone is indeed the legitimate cardholder.

The effectiveness of the CVV in CNP transactions is a significant factor in the growth and security of online and telephone commerce. It builds confidence for consumers that their financial information is being protected, and it provides merchants with a tool to reduce chargebacks due to fraud. While no security system is entirely foolproof, the CVV remains an indispensable element in the ongoing battle against payment card fraud.

Protecting Your Amex CVV and Preventing Fraud

While the CVV is a powerful security tool, its effectiveness relies on the vigilance of both cardholders and merchants. Understanding best practices for protecting your Amex CVV is crucial to preventing fraudulent activity and safeguarding your financial identity.

Best Practices for Cardholders

- Never Share Your CVV Unnecessarily: Treat your CVV with the same level of confidentiality as your PIN or online banking passwords. Only provide it when making a legitimate purchase online or over the phone. Be wary of unsolicited requests for your CVV, whether via email, text message, or phone call.

- Be Cautious of Phishing Attempts: Phishing scams often aim to trick individuals into revealing sensitive information, including their CVV. Always verify the legitimacy of a website or request before entering your card details. Look for secure website indicators (e.g., “https://” and a padlock icon) and be skeptical of suspicious links or attachments.

- Regularly Monitor Your Statements: Review your American Express statements regularly for any unauthorized transactions. Promptly report any suspicious activity to American Express to initiate an investigation.

- Secure Your Physical Card: While the CVV is on the front, the entire card needs to be protected. Avoid leaving your card unattended in public places. If your card is lost or stolen, report it immediately to American Express.

- Use Strong, Unique Passwords for Online Accounts: While not directly related to the CVV itself, strong passwords for your online shopping accounts add another layer of security. If an account with stored card details is compromised, strong passwords can prevent unauthorized access to your payment information.

Merchant Responsibilities

- Adhere to PCI DSS Standards: Merchants who accept credit card payments are required to comply with the Payment Card Industry Data Security Standard (PCI DSS). This includes stringent rules regarding the handling, storage, and transmission of cardholder data, critically prohibiting the storage of CVV data.

- Secure Transaction Processing: Utilize secure payment gateways and ensure that all online transactions are encrypted using industry-standard protocols (e.g., SSL/TLS).

- Employee Training: Train employees who handle cardholder data on proper security procedures, including the importance of not storing CVVs and recognizing potential fraud indicators.

- Regular Security Audits: Conduct regular security audits and vulnerability assessments of systems that handle cardholder data.

By following these guidelines, cardholders can significantly enhance their security, and merchants can uphold the integrity of their payment systems, collectively contributing to a safer transaction environment. The Amex CVV, when used and protected correctly, remains a formidable defense against the ever-evolving landscape of financial fraud.