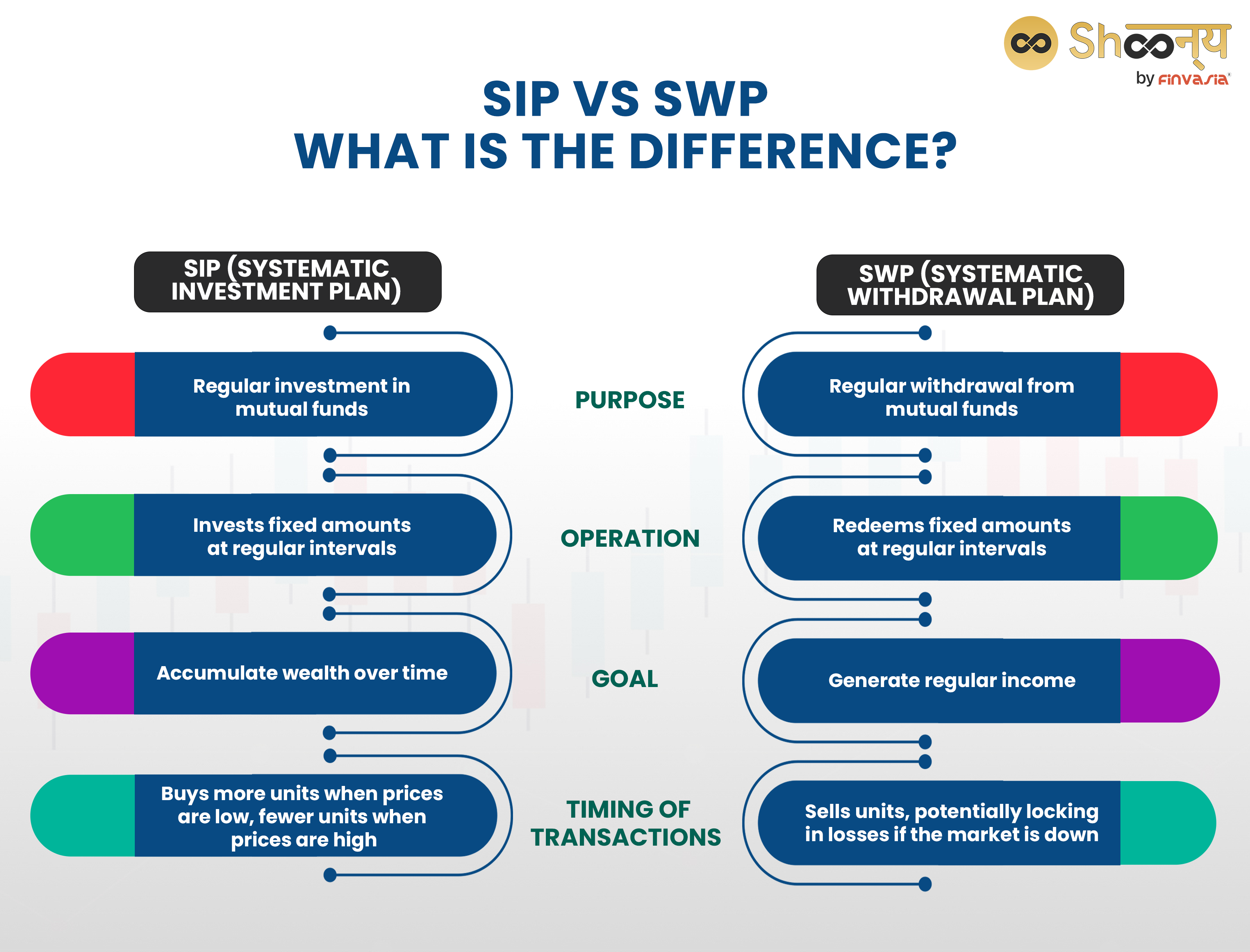

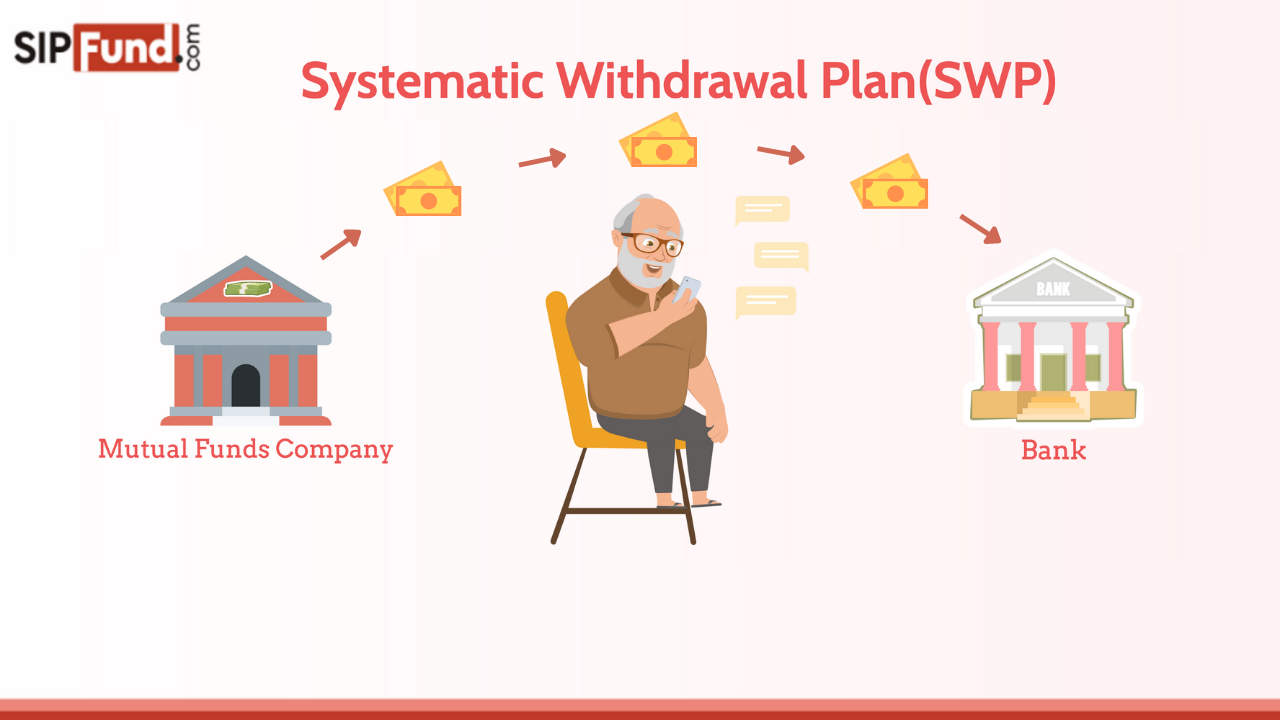

A Systematic Withdrawal Plan (SWP) is a sophisticated financial tool that allows investors to receive regular, predetermined income from their investments. It’s a structured approach to drawing down assets, typically from mutual funds or other investment portfolios, at scheduled intervals. Unlike lump-sum withdrawals, which can be volatile and subject to market timing, an SWP offers a disciplined and predictable stream of income, making it an invaluable strategy for retirees, individuals seeking supplemental income, or those managing large investment portfolios. The core principle of an SWP lies in its ability to provide financial stability and peace of mind by ensuring a consistent inflow of cash, regardless of short-term market fluctuations.

The genesis of the SWP as a financial strategy is rooted in the need for retirees to manage their accumulated wealth effectively. Traditionally, retirees would rely on pensions, Social Security, or simply withdraw funds as needed. However, with the increasing longevity of the population and the variability of market returns, a more systematic approach became necessary to ensure that retirement funds lasted throughout an individual’s lifetime. Mutual funds, with their diversified holdings and professional management, proved to be an ideal vehicle for implementing SWPs. This method allows investors to tap into their capital gains and dividends, thereby preserving the principal amount of their investment for as long as possible.

How a Systematic Withdrawal Plan Works

The mechanics of an SWP are relatively straightforward, yet powerful in their application. An investor decides on a specific amount of money they wish to withdraw at regular intervals – typically monthly, quarterly, or annually. This withdrawal amount is then automatically debited from their investment portfolio. The investment provider, such as a mutual fund house, then redeems the necessary units of the fund to facilitate the withdrawal. This process is repeated at each scheduled interval.

The key to the effectiveness of an SWP lies in the underlying mechanism of unit redemption. When the market is performing well, the value of the investor’s units increases. This means that fewer units need to be redeemed to meet the fixed withdrawal amount, thereby preserving more of the principal. Conversely, when the market experiences a downturn, the value of the units decreases. In such scenarios, more units are redeemed to meet the same fixed withdrawal amount. This inverse relationship between market performance and unit redemption is a crucial aspect of how an SWP helps mitigate the risks associated with sequence of returns risk, a phenomenon where poor investment returns early in retirement can significantly deplete an individual’s savings.

Types of Systematic Withdrawal Plans

While the fundamental concept remains the same, there are variations in how SWPs can be structured to suit different investor needs and risk appetites. These variations primarily revolve around the method of determining the withdrawal amount.

Fixed Withdrawal Amount

This is the most common and straightforward type of SWP. The investor chooses a fixed monetary sum to be withdrawn at each interval. For example, an investor might decide to withdraw $1,000 per month. This provides absolute certainty regarding the income received, making budgeting and financial planning easier. However, this method doesn’t account for inflation, which can erode the purchasing power of the fixed amount over time.

Step-Up Withdrawal Amount

To combat the effects of inflation, some SWPs offer a “step-up” feature. In this scenario, the withdrawal amount is increased annually by a predetermined percentage, often linked to the Consumer Price Index (CPI) or a fixed escalation rate. For instance, an investor might begin with a $1,000 monthly withdrawal and opt for a 5% annual step-up. This means that after one year, the monthly withdrawal would increase to $1,050, then to $1,102.50 in the subsequent year, and so on. This approach helps maintain the real value of the income stream.

Variable Withdrawal Amount (Based on Profit)

A less common but potentially beneficial variation is a variable SWP where the withdrawal amount is tied to the investment’s performance. Instead of a fixed amount, the investor might choose to withdraw a certain percentage of the fund’s value or a portion of the profits generated. This can lead to higher withdrawals during bull markets and lower (or even zero) withdrawals during bear markets, thus aligning income with investment performance. While this offers flexibility, it introduces less certainty in income planning compared to fixed withdrawals.

SWP based on Units

Another approach is to withdraw a fixed number of units at regular intervals. For example, an investor might decide to redeem 50 units of a mutual fund every month. The monetary value of this withdrawal will fluctuate daily based on the Net Asset Value (NAV) of the fund. This method can be advantageous in a rising market as the value of the redeemed units will increase, and it also benefits from the compounding effect of reinvesting dividends within the fund. However, it offers less predictability in terms of income.

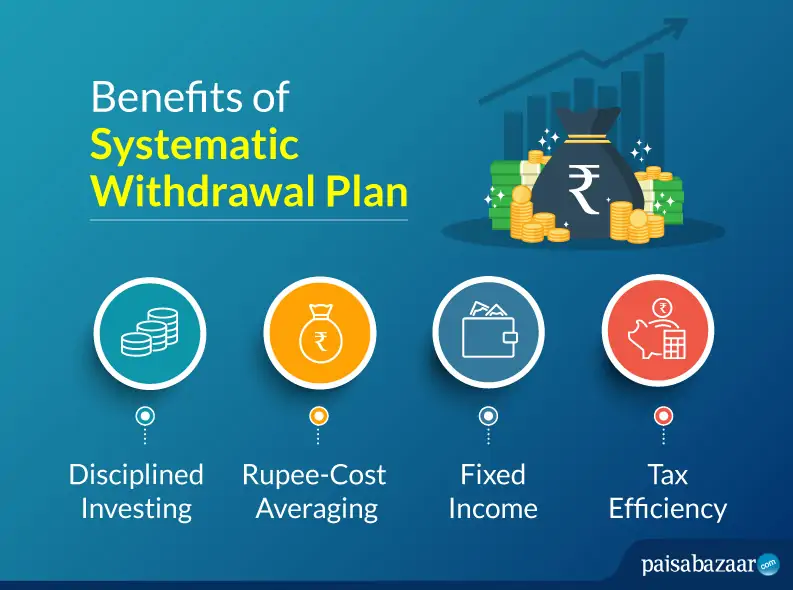

Benefits of a Systematic Withdrawal Plan

The adoption of an SWP offers a multitude of advantages for investors looking to manage their wealth systematically and sustainably. These benefits extend beyond mere income generation to encompass risk management, financial discipline, and potential long-term wealth preservation.

Predictable Income Stream

The primary allure of an SWP is the assurance of a regular, predictable income. This predictability is crucial for individuals who rely on their investments for their daily living expenses, particularly retirees. Knowing precisely how much income will be received each month or quarter simplifies budgeting, reduces financial anxiety, and allows for more effective long-term financial planning. This steady inflow contrasts sharply with the uncertainty of making ad-hoc withdrawals, which can be influenced by market sentiment and personal needs.

Disciplined Investing and Redeeming

An SWP instills financial discipline. By pre-determining withdrawal amounts and frequencies, investors are less likely to make impulsive decisions based on market volatility or emotional responses. This disciplined approach helps prevent premature depletion of capital, especially during market downturns, when the temptation to sell might be high. The systematic nature of withdrawals encourages a more rational and long-term perspective on investment management.

Potential for Wealth Preservation

Contrary to simply cashing out investments, an SWP aims to preserve the underlying principal for as long as possible. By withdrawing only the necessary amount and allowing the remaining capital to continue growing, investors can potentially sustain their income stream for an extended period. When markets perform well, the growth in the portfolio can offset the withdrawals, and in some cases, even increase the principal amount.

Inflation Hedge (with Step-Up)

As mentioned earlier, SWPs with a step-up feature can act as a hedge against inflation. By increasing the withdrawal amount periodically, investors can ensure that their purchasing power is maintained over time. This is particularly important for long-term goals like retirement, where the cost of living can significantly increase over decades.

Tax Efficiency

In many jurisdictions, SWPs can offer tax advantages. Depending on the type of investment and the jurisdiction’s tax laws, withdrawals may be taxed as capital gains rather than as ordinary income, which often carries a lower tax rate. Furthermore, by systematically redeeming units, investors can potentially manage their tax liabilities more effectively by strategically realizing gains over time. It is advisable to consult with a tax professional to understand the specific tax implications.

Managing Sequence of Returns Risk

One of the most significant risks faced by retirees is the “sequence of returns risk.” This occurs when poor investment returns happen early in the retirement period, coinciding with regular withdrawals. This can lead to a rapid depletion of the retirement corpus. An SWP, by its systematic nature and the inverse relationship between withdrawal quantity and market performance, can help mitigate this risk by redeeming fewer units when the market is down.

Considerations When Implementing an SWP

While an SWP offers significant advantages, it’s not a one-size-fits-all solution. Careful consideration of several factors is paramount to ensure its effective and successful implementation.

Investment Selection

The choice of investment vehicle for an SWP is critical. Mutual funds, particularly diversified equity and debt funds, are popular choices due to their liquidity and professional management. However, the specific fund chosen should align with the investor’s risk tolerance, time horizon, and income needs. A fund with a history of stable returns and moderate volatility might be more suitable than a highly speculative one. Debt funds or balanced funds are often preferred for the income-generating phase of retirement due to their lower risk profile compared to pure equity funds.

Withdrawal Amount and Frequency

Determining the appropriate withdrawal amount is arguably the most crucial aspect of SWP planning. It should be a sustainable amount that the portfolio can generate without compromising the long-term principal. Financial advisors often recommend withdrawal rates of around 4-5% of the initial portfolio value per year, adjusted for inflation, as a starting point. The frequency of withdrawal (monthly, quarterly, etc.) should align with the investor’s cash flow needs.

Inflation and Lifestyle Changes

Investors must factor in the impact of inflation on their future purchasing power. As discussed, incorporating a step-up in the withdrawal amount can address this. Additionally, potential lifestyle changes, such as increased healthcare costs or desires for travel, should be considered when projecting future income needs.

Market Volatility and Risk Tolerance

While an SWP aims to mitigate risk, it doesn’t eliminate it. Investors must be prepared for market fluctuations. Their risk tolerance should guide the selection of the underlying investment. For individuals with a lower risk tolerance, a higher allocation to debt instruments within the SWP portfolio might be advisable.

Tax Implications

As with any investment strategy, understanding the tax implications of an SWP is essential. The tax treatment of withdrawals can vary significantly based on the type of investment, the duration of holding, and local tax laws. Consulting with a tax professional can help optimize the strategy for tax efficiency.

Rebalancing and Review

Periodic review and rebalancing of the investment portfolio are crucial for any SWP. As the market moves, the asset allocation within the portfolio can drift. Rebalancing ensures that the portfolio remains aligned with the investor’s original investment strategy and risk profile. Regular reviews also allow for adjustments to the withdrawal amount if circumstances change.

Conclusion

A Systematic Withdrawal Plan (SWP) stands as a cornerstone strategy for individuals seeking to convert their accumulated investments into a reliable stream of income. It offers a structured, disciplined, and often tax-efficient method to draw down assets, providing financial security and peace of mind, especially during retirement. By automating withdrawals and strategically redeeming investment units, SWPs help manage market volatility and preserve capital for the long term. When implemented with careful consideration of investment selection, withdrawal amounts, inflation, and individual risk tolerance, an SWP can be a powerful tool for achieving financial goals and ensuring a comfortable and sustainable income throughout one’s life.