Section 179 of the U.S. Internal Revenue Code is a powerful tax incentive designed to encourage businesses to invest in qualifying equipment. It allows businesses to deduct the full purchase price of qualifying equipment in the year it is placed in service, rather than depreciating it over several years. This immediate deduction can significantly reduce a business’s tax liability, freeing up capital for reinvestment and growth. However, the concept of “carryover” is crucial for understanding how Section 179 works, especially when a business’s eligible deductions exceed its taxable income.

Understanding the Basics of Section 179

At its core, Section 179 offers a dollar-for-dollar tax deduction for qualifying business expenses. This means that for every dollar spent on eligible equipment, a dollar can be subtracted from a business’s taxable income, up to a certain limit. The law is particularly beneficial for small and medium-sized businesses, as it levels the playing field by providing tax relief similar to that available to larger corporations through depreciation.

Qualifying Property and Expenditures

The type of property that qualifies for Section 179 expensing is primarily tangible personal property used in a trade or business. This includes machinery, equipment, computers, software, office furniture, and even certain improvements to nonresidential real property. The key criterion is that the property must be purchased (or leased under specific terms) and placed into service during the tax year for which the deduction is claimed.

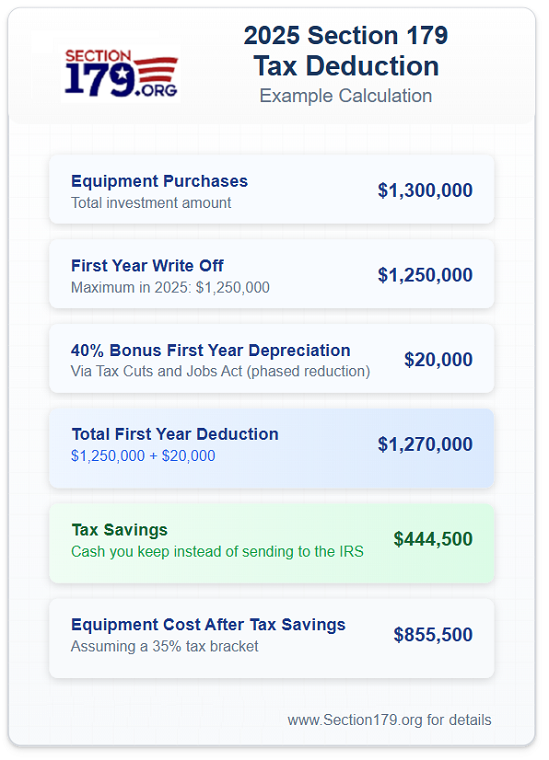

The Section 179 Limit

The Section 179 deduction is subject to annual limits. There’s a maximum amount that can be expensed in a given year, and this limit is adjusted for inflation periodically. For instance, the maximum Section 179 expense deduction for 2023 was $1,160,000. This limit is intended to ensure that the benefit primarily serves its intended purpose for smaller businesses, preventing larger corporations from leveraging it for disproportionately large deductions.

The Phase-Out Threshold

In addition to the overall limit, there’s a phase-out threshold. If the total cost of qualifying equipment purchased and placed in service during the tax year exceeds this threshold, the Section 179 deduction is reduced dollar-for-dollar. For 2023, this threshold was $2,890,000. This means that businesses exceeding this spending level will see their Section 179 deduction incrementally decrease until it reaches zero.

The Concept of Section 179 Carryover

The term “Section 179 carryover” arises when the total amount a business is eligible to deduct under Section 179 exceeds its taxable income for the year. In simpler terms, if your potential Section 179 deduction is $50,000, but your business only has $30,000 in taxable income for the year, you can only deduct $30,000. The remaining $20,000 cannot be lost. This is where the carryover provision comes into play.

How Carryover Works

When a business cannot fully utilize its Section 179 deduction due to insufficient taxable income, the unused portion is “carried over” to the subsequent tax year. This carried-over amount is treated as if it were an expense incurred in that following year. It can then be deducted in that next year, subject to the Section 179 limits and taxable income limitations applicable to that year.

For example, if a business has $50,000 in eligible Section 179 expenses but only $30,000 in taxable income, it can deduct $30,000 in the current year. The remaining $20,000 is carried over. In the next tax year, the business can deduct up to $20,000 of that carryover amount, in addition to any new Section 179 expenses it incurs and is eligible for in that future year, provided its taxable income is sufficient to cover both.

Interaction with Other Tax Provisions

It’s important to note that Section 179 carryover interacts with other tax provisions. For instance, if a business has a net operating loss (NOL), the taxable income limitation might prevent it from taking any Section 179 deduction, even if it has qualifying expenses. In such cases, the entire amount of eligible Section 179 expenses would be carried over. Similarly, if a business has a significant amount of unused Section 179 carryover from previous years, it will be considered when calculating the total Section 179 deduction for the current year.

Limitations and Considerations of Carryover

While the carryover provision is a valuable mechanism for ensuring businesses don’t lose out on tax benefits, there are important limitations and considerations to keep in mind.

Taxable Income Limitation Remains Key

The fundamental limitation for claiming a Section 179 deduction, whether it’s for current year expenses or carryover amounts, is the business’s taxable income. Even with carryover, a business cannot deduct more than its taxable income in any given year. This means that if a business continues to experience low profitability, it might carry over Section 179 deductions for several years.

The Carryover Period

Section 179 carryovers do not have an indefinite lifespan. They are generally carried forward until they are fully utilized or until the business disposes of the property. The specific rules can be complex, and it’s often advisable to consult with a tax professional to track carryover amounts accurately.

Record Keeping is Paramount

Proper and meticulous record-keeping is absolutely essential for any business utilizing Section 179. This includes detailed records of qualifying purchases, placement-in-service dates, the amount of Section 179 deduction claimed in prior years, and any carryover amounts. Without accurate records, it can be incredibly difficult, if not impossible, to substantiate Section 179 deductions and carryovers when audited by the IRS.

Strategic Utilization of Section 179 and Carryover

Understanding Section 179 and its carryover provisions allows businesses to engage in strategic tax planning.

Planning for Capital Expenditures

Businesses anticipating significant capital expenditures for qualifying equipment should factor in the Section 179 limits and their projected taxable income. If a planned purchase will exceed the current year’s taxable income, the carryover provision should be accounted for in future tax planning. This can help in budgeting and forecasting tax liabilities.

Timing of Purchases

The timing of equipment purchases can also be strategic. If a business is on the cusp of exceeding its taxable income, it might consider delaying some purchases until the following year to ensure full utilization of the Section 179 deduction and avoid unnecessary carryovers, assuming future years are expected to be more profitable. Conversely, if a business is expecting a highly profitable year, it might accelerate purchases to maximize the current year’s deduction.

The Impact of Business Cycles

The effectiveness of Section 179 and its carryover provisions can be significantly influenced by business cycles. In periods of strong economic growth and high profitability, businesses can fully leverage Section 179 deductions. During economic downturns, however, taxable income may fall, leading to increased Section 179 carryovers. The carryover mechanism provides a degree of flexibility, allowing businesses to defer tax benefits until they are in a better financial position to utilize them.

Conclusion on Section 179 Carryover

Section 179 carryover is an integral part of the Section 179 expensing deduction, designed to provide flexibility for businesses that invest in qualifying equipment but may not have sufficient taxable income in a given year to fully utilize the deduction. It allows the unused portion of the deduction to be carried forward to future tax years, where it can be applied against future taxable income. This provision underscores the intent of Section 179: to encourage business investment by offering a tangible tax advantage, even if the full benefit cannot be realized immediately. Diligent record-keeping and thoughtful tax planning are paramount for any business seeking to maximize the benefits of Section 179 and its carryover provisions. Consulting with a qualified tax advisor is always recommended to navigate the complexities of tax law and ensure optimal financial strategies.