Section 179 of the Internal Revenue Code (IRC) is a powerful tax deduction that allows businesses to immediately expense the full purchase price of qualifying equipment and software, rather than depreciating it over several years. This provision is designed to encourage businesses to invest in themselves by purchasing new or used assets that will help them grow and become more productive. For many businesses, especially those operating in rapidly evolving technological sectors, understanding and leveraging Section 179 can lead to significant tax savings and improved cash flow.

The core principle behind Section 179 is to provide an incentive for businesses to acquire assets that are put into service during the tax year. Instead of spreading the deduction over the useful life of the asset, which is the standard depreciation method, businesses can “expense” it all at once. This immediate deduction reduces a company’s taxable income, directly translating into lower tax liability. The legislation was enacted to help small and medium-sized businesses compete with larger corporations by providing them with a more accessible way to afford necessary capital expenditures. The “expense” refers to the amount of the qualified business property that can be deducted in the year it is placed in service, up to a certain annual limit.

The Mechanics of Section 179 Expensing

Eligibility Requirements for Qualifying Property

To qualify for the Section 179 deduction, the purchased asset must meet specific criteria. Primarily, it must be tangible personal property that is subject to depreciation and used more than 50% for business purposes. This includes a wide range of assets, from machinery and equipment to furniture and computer software. For example, if a business purchases a new server, a specialized piece of manufacturing equipment, or even qualifying software for business operations, these could all be eligible for Section 179 expensing.

Furthermore, the property must be purchased or financed and placed in service during the tax year for which the deduction is being claimed. “Placed in service” generally means that the property is ready and available for its intended business use. It doesn’t necessarily mean it’s actively being used, but it must be in a condition and location where it’s available for use. This distinction is important because acquiring an asset in December of a tax year, for instance, but not having it fully operational until January of the next year, means it wouldn’t qualify for the Section 179 deduction in the earlier year.

The type of business also plays a role. Section 179 is generally available to businesses that purchase qualifying property for use in the active conduct of their trade or business. This typically includes sole proprietorships, partnerships, and corporations. However, there are specific rules for certain types of property, such as those used for leasing, and for certain businesses like those providing lodging or engaged in specific entertainment-related activities, where the deduction may be limited or disallowed.

Deduction Limits and Phase-Outs

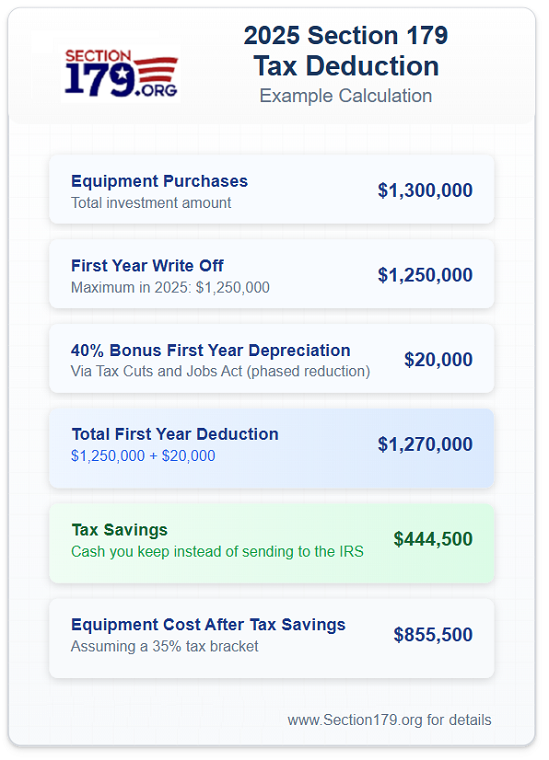

The Section 179 deduction is not unlimited. There are annual caps on the total amount a business can expense and a threshold that triggers a phase-out of the deduction. For the current tax year, there is a maximum amount of expenditure that can be deducted under Section 179. This annual dollar limit is adjusted for inflation each year. For instance, if the maximum deduction limit is $1,080,000, a business cannot expense more than this amount, even if they purchase more qualifying property.

Beyond the expenditure limit, there’s also a phase-out provision. This means that if a business purchases more than a certain dollar amount of qualifying property during the tax year, the maximum Section 179 deduction is reduced dollar-for-dollar. This phase-out threshold is also adjusted annually. For example, if the phase-out begins at $2,700,000 in total qualified property purchases, and a business buys $3,000,000 worth of assets, their Section 179 deduction will be reduced by $300,000 (the amount exceeding the threshold). If the total purchases exceed the phase-out amount by more than the maximum deduction limit, the business may not be able to claim any Section 179 deduction at all. These limits and phase-outs are crucial for businesses to understand to accurately plan their tax strategies.

Strategic Advantages of Section 179

Enhancing Cash Flow and Investment

One of the most significant benefits of Section 179 is its impact on a business’s cash flow. By allowing an immediate deduction, companies can effectively reduce their tax burden in the present year, freeing up capital that would otherwise be paid to the government. This extra cash can then be reinvested into the business, used for further expansion, research and development, or to cover operational expenses. For businesses that rely on capital expenditures to maintain their competitive edge, such as those in fast-paced industries, this immediate tax relief can be instrumental in their ability to innovate and grow.

Consider a business that needs to upgrade its equipment to improve efficiency. Without Section 179, they might have to spread the cost over five or ten years through depreciation. This means smaller tax deductions each year, and thus a larger tax bill in the short term. With Section 179, they can deduct the entire cost upfront, significantly lowering their current year’s taxable income and paying less tax. This enhanced cash flow makes it more feasible to acquire the necessary assets sooner, accelerating the realization of the benefits of the new equipment.

Stimulating Business Growth and Modernization

Section 179 acts as a powerful catalyst for business growth and modernization. It incentivizes businesses to purchase new or improved assets, which often leads to increased productivity, efficiency, and innovation. When businesses can more easily afford to acquire advanced technology, machinery, or software, they are better equipped to compete in the marketplace, meet customer demands, and adapt to evolving industry standards.

For example, a small manufacturing firm might be struggling with outdated machinery that limits its production capacity. By utilizing Section 179, they can acquire state-of-the-art equipment, write off a significant portion of the cost immediately, and boost their output. This increased capacity can lead to more sales, higher profits, and the ability to hire more employees. Similarly, a software development company might use Section 179 to purchase powerful new workstations and specialized development tools, accelerating their product release cycles and staying ahead of competitors. The provision essentially lowers the barrier to entry for businesses looking to invest in the tools they need to thrive.

Considerations and Limitations

Taxable Income Requirement

A critical aspect of claiming the Section 179 deduction is that it cannot create a net operating loss (NOL) for the business. The deduction is limited to the business’s taxable income for the year. If the Section 179 deduction would cause the business’s deductions to exceed its gross income, the amount of the deduction is limited to the business’s taxable income. Any excess deduction that cannot be taken due to this limitation can be carried forward to future tax years, subject to the same limitations.

This means that a business with no taxable income cannot benefit from Section 179, even if they purchase qualifying property. The deduction is intended to offset existing taxable income, not to generate a loss that can be used in other ways or carried back. Therefore, businesses with minimal or no profits might not see immediate tax savings from Section 179, although they can still carry forward the unused portion of the deduction to future profitable years.

Property Used for Both Business and Personal Purposes

As mentioned earlier, for property to qualify for Section 179 expensing, it must be used more than 50% for business purposes. If an asset is used for both business and personal use, and the business use percentage falls at or below 50%, the Section 179 deduction is disallowed entirely. If the business use percentage is above 50% but less than 100%, the Section 179 deduction is limited to the business portion of the asset’s cost.

For instance, if a business purchases a vehicle that will be used for both client visits and personal errands, and the business use is determined to be 70%, then only 70% of the vehicle’s cost is eligible for Section 179 expensing, provided it meets all other criteria. This “mixed-use” consideration requires careful record-keeping and accurate allocation of the asset’s use to ensure compliance with IRS regulations. Failure to maintain proper documentation for business use can lead to the disallowance of the deduction.

Interaction with Other Tax Provisions

Section 179 does not operate in isolation; it interacts with other tax provisions, such as bonus depreciation and the standard depreciation methods (like MACRS – Modified Accelerated Cost Recovery System). Businesses often have to choose between these different depreciation strategies for their qualifying assets. For example, bonus depreciation allows for an immediate deduction of a certain percentage of an asset’s cost in the year it is placed in service, and this percentage is often higher than what might be available through Section 179, especially if Section 179 limits have been reached.

However, Section 179 offers a distinct advantage in that it allows for the expensing of the full purchase price, up to the statutory limit, whereas bonus depreciation is typically a percentage of the cost. Furthermore, Section 179 can be applied to both new and used equipment, while bonus depreciation has historically been limited to new property, though this has evolved with recent tax law changes. Businesses need to carefully analyze their specific situation, including their projected taxable income, the total amount of qualifying asset purchases, and the tax benefits of each option, to determine the most advantageous depreciation strategy. Often, a combination of Section 179 and bonus depreciation might be employed to maximize tax savings.