Retained earnings are a fundamental concept in corporate finance, representing the accumulated profits of a company that have not been distributed to shareholders as dividends. This crucial figure offers a window into a company’s financial health, its reinvestment strategies, and its long-term growth potential. For businesses, understanding and accurately calculating retained earnings is paramount for strategic decision-making, including capital allocation, dividend policy, and overall financial planning. In essence, retained earnings are the portion of net income that a company keeps in its business for future use, rather than paying out.

The Core Components of Retained Earnings

At its most basic, the retained earnings calculation starts with a company’s net income. However, several adjustments and considerations are vital for a comprehensive understanding. The primary drivers are profitability, dividend payouts, and any prior period adjustments.

Net Income: The Starting Point

Net income, often referred to as the “bottom line,” is the profit a company earns after deducting all expenses, taxes, and interest from its total revenue. It is typically reported on the income statement. A positive net income signifies that the company has been profitable during a given period, thus generating funds that can potentially be retained. Conversely, a negative net income (a net loss) will reduce retained earnings.

Dividends Paid: The Outflow

Dividends are distributions of a portion of a company’s earnings to its shareholders. These can be paid in cash, stock, or other assets. When a company declares and pays dividends, these amounts are subtracted from its net income before they are added to the retained earnings balance. The decision to pay dividends is a strategic one, often influenced by the company’s profitability, its investment opportunities, and shareholder expectations. A high dividend payout ratio suggests that a company is returning a significant portion of its profits to shareholders, which will, in turn, lower its retained earnings growth.

Prior Period Adjustments: Correcting the Past

Occasionally, a company may discover errors in its financial statements from previous periods. These errors, when identified and corrected, can impact retained earnings. For instance, if an expense was understated in a prior year, the net income for that year would have been overstated, leading to an inflated retained earnings balance. A prior period adjustment would involve restating the prior period’s financial statements to correct this error, which would typically result in a reduction of the current period’s retained earnings. Conversely, if a revenue was understated, the adjustment would increase retained earnings. These adjustments are less common than the regular additions and subtractions but are crucial for ensuring the accuracy of the retained earnings figure over time.

The Retained Earnings Formula and Calculation

The calculation of retained earnings is a straightforward process, but it requires access to specific financial data. The general formula provides a clear roadmap for determining the retained earnings balance at any given point.

The Basic Retained Earnings Formula

The fundamental formula for calculating retained earnings is:

Ending Retained Earnings = Beginning Retained Earnings + Net Income – Dividends Paid

Let’s break down each element of this formula:

- Beginning Retained Earnings: This is the balance of retained earnings at the start of an accounting period (e.g., the beginning of a fiscal year or quarter). This figure is carried over from the ending retained earnings of the previous period.

- Net Income: This is the company’s profit for the current accounting period, as reported on the income statement. If the company incurred a net loss, this figure will be negative and will reduce retained earnings.

- Dividends Paid: This represents the total amount of dividends declared and paid to shareholders during the current accounting period. This can include both cash dividends and stock dividends, though stock dividends are typically accounted for differently and may not directly reduce the retained earnings balance in the same way cash dividends do.

Example Calculation

To illustrate, consider a company with the following financial data:

- Beginning Retained Earnings (January 1, 2023): $500,000

- Net Income for the year 2023: $200,000

- Dividends Paid during 2023: $50,000

Using the formula:

Ending Retained Earnings (December 31, 2023) = $500,000 (Beginning Retained Earnings) + $200,000 (Net Income) – $50,000 (Dividends Paid)

Ending Retained Earnings (December 31, 2023) = $650,000

This means that at the end of 2023, the company has $650,000 in accumulated profits that have been retained within the business.

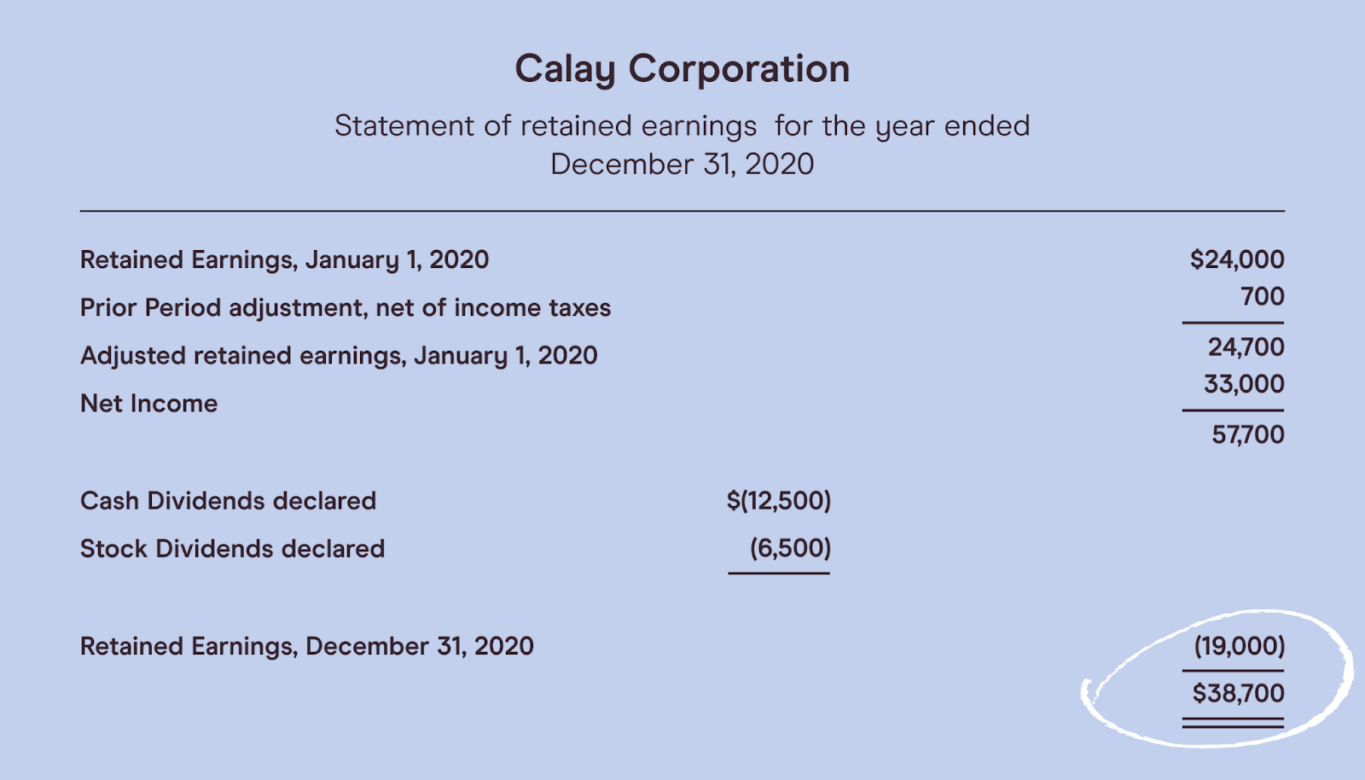

Incorporating Prior Period Adjustments

If prior period adjustments are necessary, the formula becomes slightly more nuanced. The adjustment is typically applied directly to the beginning retained earnings balance of the current period.

Ending Retained Earnings = (Beginning Retained Earnings + Prior Period Adjustments) + Net Income – Dividends Paid

For instance, if the company from the previous example discovered an error in 2022 that required a $20,000 upward adjustment to its 2022 net income, and the beginning retained earnings for 2023 were reported before this adjustment was made, then the calculation for the end of 2023 would be:

- Reported Beginning Retained Earnings (January 1, 2023): $500,000

- Prior Period Adjustment (increase in prior income): +$20,000

- Net Income for 2023: $200,000

- Dividends Paid during 2023: $50,000

Ending Retained Earnings (December 31, 2023) = ($500,000 + $20,000) + $200,000 – $50,000

Ending Retained Earnings (December 31, 2023) = $520,000 + $200,000 – $50,000

Ending Retained Earnings (December 31, 2023) = $670,000

It is crucial that prior period adjustments are clearly disclosed in the financial statements, along with their impact on retained earnings.

The Significance of Retained Earnings in Financial Reporting

Retained earnings are a key component of a company’s balance sheet, falling under the equity section. Their value provides insights into several critical aspects of a company’s financial strategy and performance.

Retained Earnings on the Balance Sheet

The balance sheet presents a snapshot of a company’s financial position at a specific point in time. Retained earnings appear on the equity side, representing the owners’ stake in the company derived from accumulated profits. The equity section typically includes common stock, additional paid-in capital, and retained earnings. The total equity represents the net worth of the company attributable to its shareholders.

A substantial retained earnings balance generally indicates that a company has been consistently profitable and has chosen to reinvest those profits back into the business rather than distributing them all as dividends. This can signal a growth-oriented strategy. Conversely, a low or negative retained earnings balance might suggest periods of unprofitability, aggressive dividend payouts, or significant losses.

Retained Earnings as a Source of Funding

Retained earnings represent internal financing for a company. Instead of issuing new debt or equity, a company can tap into its retained earnings to fund various initiatives. This can include:

- Reinvestment in Operations: Purchasing new equipment, upgrading technology, expanding facilities, or investing in research and development.

- Acquisitions: Funding the purchase of other companies.

- Debt Reduction: Paying down outstanding loans and improving the company’s leverage ratios.

- Share Buybacks: Repurchasing the company’s own stock, which can increase earnings per share and shareholder value.

The ability to fund these activities through retained earnings is often seen as a sign of financial strength and operational efficiency, as it avoids the costs associated with external financing, such as interest payments on debt or dilution of ownership from issuing new stock.

Impact on Dividend Policy and Investor Perception

The level of retained earnings directly influences a company’s dividend policy. Companies with ample retained earnings have greater flexibility to pay dividends. However, the decision to pay dividends versus retaining earnings for reinvestment is a delicate balance.

- Growth Companies: Younger or rapidly growing companies often prioritize reinvesting most of their earnings to fuel expansion. They may pay little to no dividends, as investors in these companies are typically looking for capital appreciation rather than immediate income.

- Mature Companies: Established, stable companies with fewer high-growth investment opportunities might distribute a larger portion of their earnings to shareholders in the form of dividends.

Investor perception of retained earnings can vary. Some investors see large retained earnings as a positive sign of a company’s ability to generate profits and reinvest them for future growth. Others might view it as a sign that management is not effectively deploying capital or that the company is being too conservative with its dividend payouts, preferring immediate income. Understanding the company’s industry, stage of development, and management’s stated strategy is crucial for interpreting the significance of its retained earnings.

Legal and Accounting Considerations for Retained Earnings

While retained earnings represent accumulated profits, there are legal and accounting constraints that govern their use and reporting. These ensure financial integrity and protect stakeholders.

Legal Restrictions on Retained Earnings

Many jurisdictions have legal restrictions on the amount of retained earnings that can be distributed as dividends. These restrictions are often in place to protect creditors by ensuring that a company maintains a certain level of equity to absorb potential losses. For example, some laws may limit dividend payouts to the amount of retained earnings that is not legally restricted or required for other purposes. A common restriction is a prohibition against paying dividends if the company is insolvent or would become insolvent as a result of the distribution.

Accumulated Deficits

A negative retained earnings balance is known as an accumulated deficit. This occurs when a company has incurred more losses than profits over its lifetime, or when dividend payouts have exceeded accumulated profits. An accumulated deficit can be a serious red flag, indicating persistent unprofitability. Companies with accumulated deficits may face challenges in obtaining financing and may be subject to stricter regulatory scrutiny. In some cases, companies might undertake actions like a reverse stock split or a recapitalization to eliminate an accumulated deficit, though this does not address the underlying cause of losses.

Disclosure Requirements

Accounting standards, such as Generally Accepted Accounting Principles (GAAP) in the United States and International Financial Reporting Standards (IFRS) globally, mandate specific disclosures related to retained earnings. Companies must report the beginning and ending balances of retained earnings and detail any changes during the period, including net income, net loss, and dividends paid. Prior period adjustments must also be clearly disclosed, explaining the nature of the error and its impact on the retained earnings balance. This transparency is vital for investors and other stakeholders to make informed decisions.

Analyzing Retained Earnings Trends and Implications

Beyond the static calculation, analyzing the trends and patterns in retained earnings over multiple periods provides a more dynamic and insightful view of a company’s financial trajectory.

Trend Analysis: Growth vs. Stagnation

Monitoring retained earnings over several accounting periods allows for trend analysis. An increasing retained earnings balance, especially when coupled with consistent net income growth, is generally a positive indicator. It suggests that the company is effectively generating profits and reinvesting them to fuel future growth.

Conversely, a stagnating or declining retained earnings balance, particularly if net income is not growing, could signal underlying issues. This might include declining profitability, an unsustainable dividend payout policy, or a lack of profitable investment opportunities. A careful examination of the components (net income and dividends) is necessary to understand the drivers behind the trend.

The Retained Earnings to Equity Ratio

A useful metric for assessing the proportion of equity derived from retained earnings is the retained earnings to total equity ratio.

Retained Earnings to Equity Ratio = Retained Earnings / Total Shareholder’s Equity

This ratio indicates how much of the company’s equity base is a result of internally generated profits versus external capital contributions (common stock, additional paid-in capital). A higher ratio suggests that the company has relied more on internal funding for its growth and operations, which can be a sign of financial prudence and success. However, as with all ratios, it should be analyzed in context with industry benchmarks and the company’s specific circumstances.

Strategic Implications for Management

For management, the retained earnings calculation is not merely an accounting exercise but a critical tool for strategic planning. The decision to retain earnings or distribute them as dividends has significant implications for the company’s financial flexibility, growth prospects, and shareholder value.

- Investment Decisions: Management must evaluate potential investments and determine if the expected returns justify retaining earnings rather than distributing them.

- Dividend Policy: Establishing a clear and consistent dividend policy that aligns with the company’s financial health and growth objectives is crucial.

- Capital Structure Management: Retained earnings contribute to the equity portion of the capital structure. Management must balance debt and equity financing to optimize the cost of capital and minimize financial risk.

By diligently calculating and analyzing retained earnings, companies can make more informed decisions that foster sustainable growth, enhance profitability, and ultimately maximize shareholder wealth.