Understanding the Unseen Financial Landscape

The term “private debt” often evokes images of complex financial instruments and exclusive deals, far removed from the everyday consumer’s experience with banks and credit cards. Yet, private debt plays a crucial, albeit often invisible, role in the global economy, funding everything from burgeoning startups to established corporations seeking alternatives to traditional public markets. It represents a significant and growing segment of the financial universe, offering both unique opportunities and inherent risks for investors and borrowers alike.

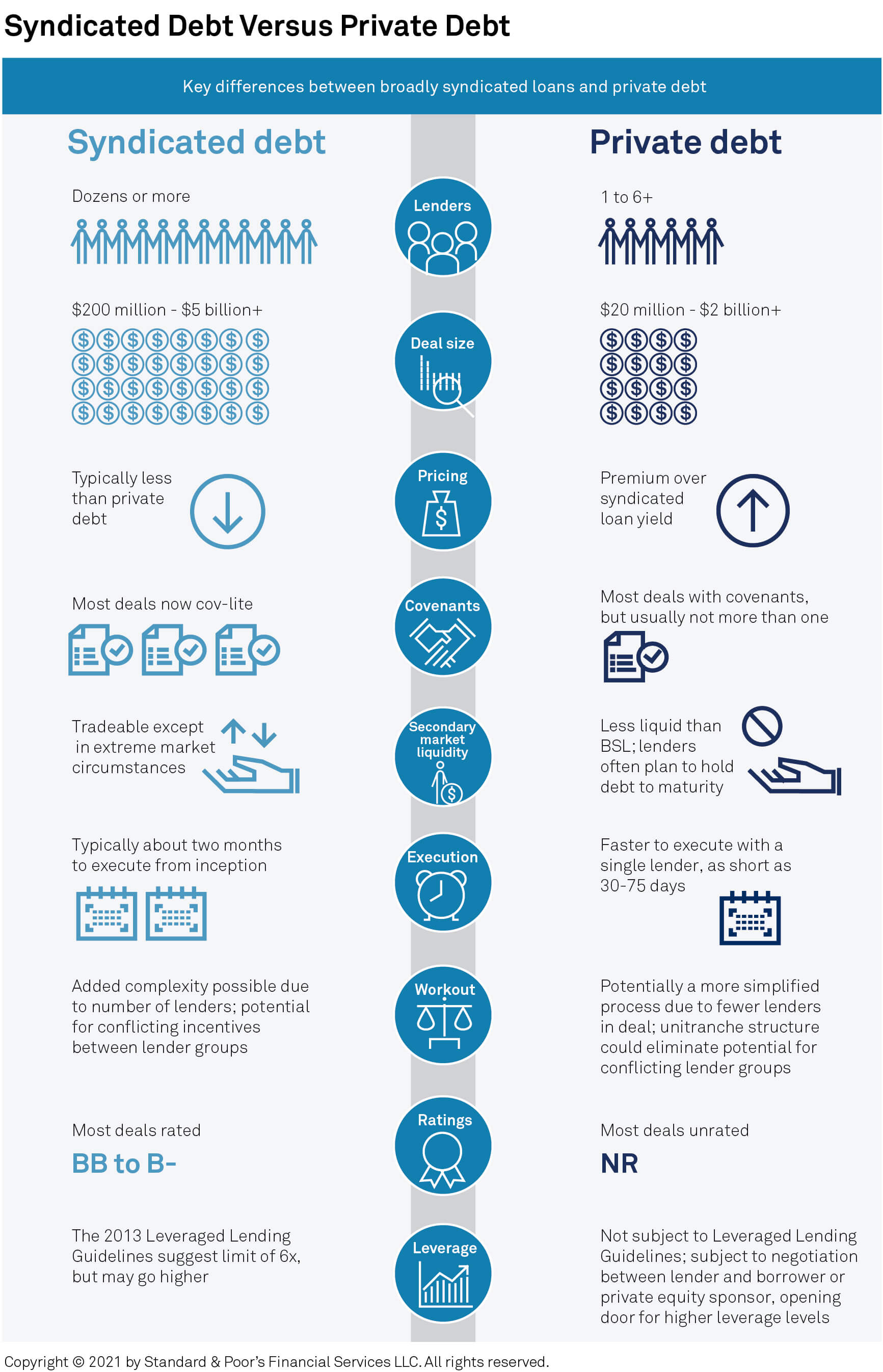

At its core, private debt refers to debt instruments that are not publicly traded on exchanges. Unlike corporate bonds or government securities, which are readily accessible to a broad range of investors, private debt is typically held by a select group of sophisticated investors, such as pension funds, insurance companies, private equity firms, and high-net-worth individuals. This exclusivity stems from several factors, including the complexity of the instruments, the higher minimum investment requirements, and the less regulated nature of these transactions compared to public markets.

The Spectrum of Private Debt

The world of private debt is not monolithic; it encompasses a diverse range of lending structures and strategies, each tailored to meet specific financing needs and risk appetites. Understanding these distinctions is key to appreciating the breadth and depth of this financial sector.

Direct Lending

Perhaps the most straightforward form of private debt, direct lending involves a private lender (often a specialized fund or financial institution) providing a loan directly to a company. This bypasses traditional intermediaries like banks, allowing for more tailored loan terms, faster execution, and potentially more flexible covenants. Direct lending has surged in popularity, especially for small and medium-sized enterprises (SMEs) that may struggle to access capital through conventional banking channels or find public markets too cumbersome. Lenders in this space often focus on specific industries or company sizes, developing specialized expertise to assess risk and structure loans effectively.

Middle Market Lending

A significant portion of direct lending activity occurs within the middle market. These are companies that are too large to be considered small businesses but too small to access public debt markets. They often possess strong growth potential but may require bespoke financing solutions that traditional banks are unwilling or unable to provide due to regulatory constraints or a lack of specific industry knowledge. Middle market lenders step in to fill this void, offering term loans, revolving credit facilities, and sometimes mezzanine financing.

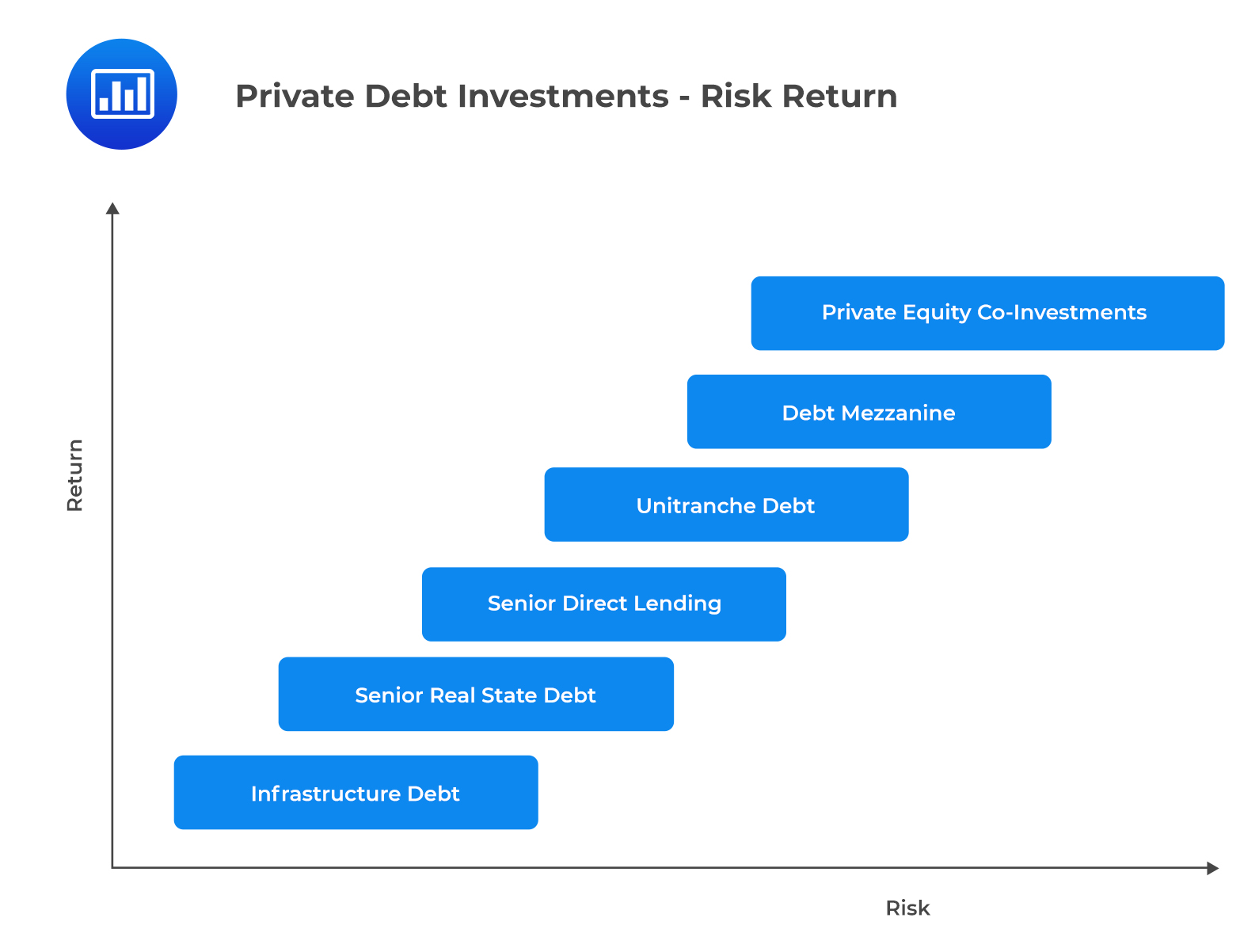

Unitranche Facilities

A popular structure within direct lending is the unitranche facility. This combines senior and subordinated debt into a single loan, simplifying the capital structure for the borrower and often providing a more unified point of contact for the lender. Unitranche facilities can offer greater flexibility and speed compared to negotiating separate senior and subordinated tranches with multiple lenders.

Mezzanine Debt

Mezzanine debt occupies a unique position in the capital structure, sitting between senior debt (like bank loans) and equity. It typically carries a higher interest rate than senior debt to compensate for its subordinated position, meaning it gets repaid after senior debt in the event of a default. Mezzanine debt often includes an “equity kicker,” such as warrants or options, giving the lender the potential to participate in the upside if the company performs well. This type of financing is often used by companies undertaking acquisitions, management buyouts, or significant growth initiatives where traditional debt is insufficient.

Venture Debt

Venture debt is specifically designed for venture capital-backed startups and early-stage growth companies. These companies often have high growth potential but may not yet be profitable or possess the collateral typically required by traditional lenders. Venture debt provides them with non-dilutive financing, meaning it doesn’t require them to give up equity. It can be used to extend runway, fund operational expenses, or bridge financing gaps between equity rounds. Lenders of venture debt typically have a deep understanding of the venture capital ecosystem and assess risk based on the company’s technology, market traction, and the strength of its venture capital backers.

Special Situations and Distressed Debt

This segment of private debt involves lending to companies facing financial distress or undergoing significant restructuring. Investors in this area often have a high-risk tolerance and deep expertise in turnarounds, distressed asset management, and complex legal frameworks. They might provide financing to enable a company to continue operations during bankruptcy proceedings, fund a restructuring plan, or acquire distressed assets at a discount. This type of investing requires a keen eye for value and a willingness to navigate challenging corporate environments.

Real Estate Debt

While often considered a distinct asset class, private debt also plays a significant role in real estate financing. This includes private loans for commercial property acquisitions, development projects, bridge loans for interim financing, and distressed real estate situations. These loans are typically secured by the underlying real estate assets and are structured based on the property’s value, income-generating potential, and market conditions.

The Appeal of Private Debt

The burgeoning growth of private debt is driven by several compelling factors for both borrowers and lenders.

For Borrowers

- Flexibility and Customization: Private debt allows for highly customized loan terms, covenants, and repayment schedules that can be precisely tailored to a company’s specific needs and cash flow cycle. This contrasts with the often standardized terms of public debt.

- Speed and Efficiency: The private negotiation process can often be faster than the lengthy syndication processes involved in public debt offerings, allowing companies to secure funding more quickly.

- Access to Capital: For companies that may not qualify for traditional bank loans or find public markets inaccessible, private debt provides a vital avenue for raising capital, particularly for growth initiatives, acquisitions, or working capital needs.

- Confidentiality: Private debt transactions are not subject to the same public disclosure requirements as publicly traded securities, offering borrowers a greater degree of confidentiality.

- Non-Dilutive Financing: For venture-backed companies, venture debt offers a way to raise capital without diluting existing equity stakes.

For Lenders (Investors)

- Attractive Yields: Private debt typically offers higher interest rates and yields compared to traditional fixed-income investments like government bonds or investment-grade corporate bonds. This is compensation for the illiquidity, higher risk, and complexity involved.

- Diversification: Private debt can offer diversification benefits to an investment portfolio, as its performance may not be perfectly correlated with public equity or bond markets.

- Access to Niche Markets: It provides access to financing opportunities in sectors or for companies that might be overlooked by traditional lenders or public markets.

- Active Management and Control: In some private debt structures, lenders can have more direct involvement and influence over the borrower’s operations and financial health through covenants and direct communication.

- Illiquidity Premium: Investors are rewarded for tying up their capital for longer periods, as private debt is generally illiquid and cannot be easily sold on short notice.

Risks and Considerations

Despite its attractiveness, private debt is not without its risks, and a thorough understanding of these is paramount for all participants.

For Borrowers

- Higher Cost: The flexibility and bespoke nature of private debt often come with a higher interest rate than senior secured bank loans.

- Covenants and Restrictions: While flexible, private debt agreements can include stringent covenants that restrict a company’s operational or financial flexibility. Violating these covenants can have severe consequences.

- Illiquidity: If a borrower wishes to refinance or repay the debt early, there may be prepayment penalties, or it might be difficult to find alternative financing if market conditions change.

- Dependence on a Single Lender: In direct lending, borrowers may become heavily reliant on a single lender or a small group of lenders, which can create leverage for the lender in future negotiations.

For Lenders (Investors)

- Illiquidity: This is the most significant risk. Private debt investments are difficult to sell quickly, meaning capital can be locked up for years.

- Credit Risk: The fundamental risk is that the borrower will default on their obligations, leading to a loss of capital. This risk can be amplified in private debt due to less transparency and potentially higher risk profiles of borrowers.

- Valuation Challenges: Determining the fair market value of private debt can be complex due to the lack of readily available market prices.

- Complexity and Due Diligence: Structuring and managing private debt deals requires significant expertise, extensive due diligence, and ongoing monitoring.

- Regulatory and Legal Risks: While less regulated than public markets, private debt is still subject to various legal and regulatory frameworks that can evolve.

- Interest Rate Risk: Like all debt instruments, private debt is subject to interest rate fluctuations, though floating-rate loans can mitigate some of this risk.

The Evolving Landscape of Private Debt

The private debt market has witnessed substantial growth over the past decade, fueled by several trends. Following the 2008 financial crisis, increased regulatory scrutiny on traditional banks led them to reduce their lending activities. This created a void that private debt providers were eager to fill. Furthermore, institutional investors, seeking higher returns in a low-interest-rate environment, have increasingly allocated capital to private markets, including private debt.

The rise of specialized private debt funds, often managed by experienced professionals, has democratized access for institutional investors. Technology is also playing an increasing role, with data analytics and AI being used to enhance due diligence, portfolio management, and risk assessment. As the market matures, we are seeing greater segmentation, with funds specializing in specific geographies, industries, and debt types.

In conclusion, private debt represents a dynamic and integral component of the modern financial system. It provides essential capital for businesses of all sizes, fostering innovation and economic growth. For investors, it offers the potential for attractive returns and portfolio diversification, albeit with commensurate risks. As the financial landscape continues to evolve, private debt is poised to remain a significant and influential force, shaping the way companies are funded and the way capital is deployed. Understanding its nuances is increasingly important for anyone seeking a comprehensive view of the global economy.