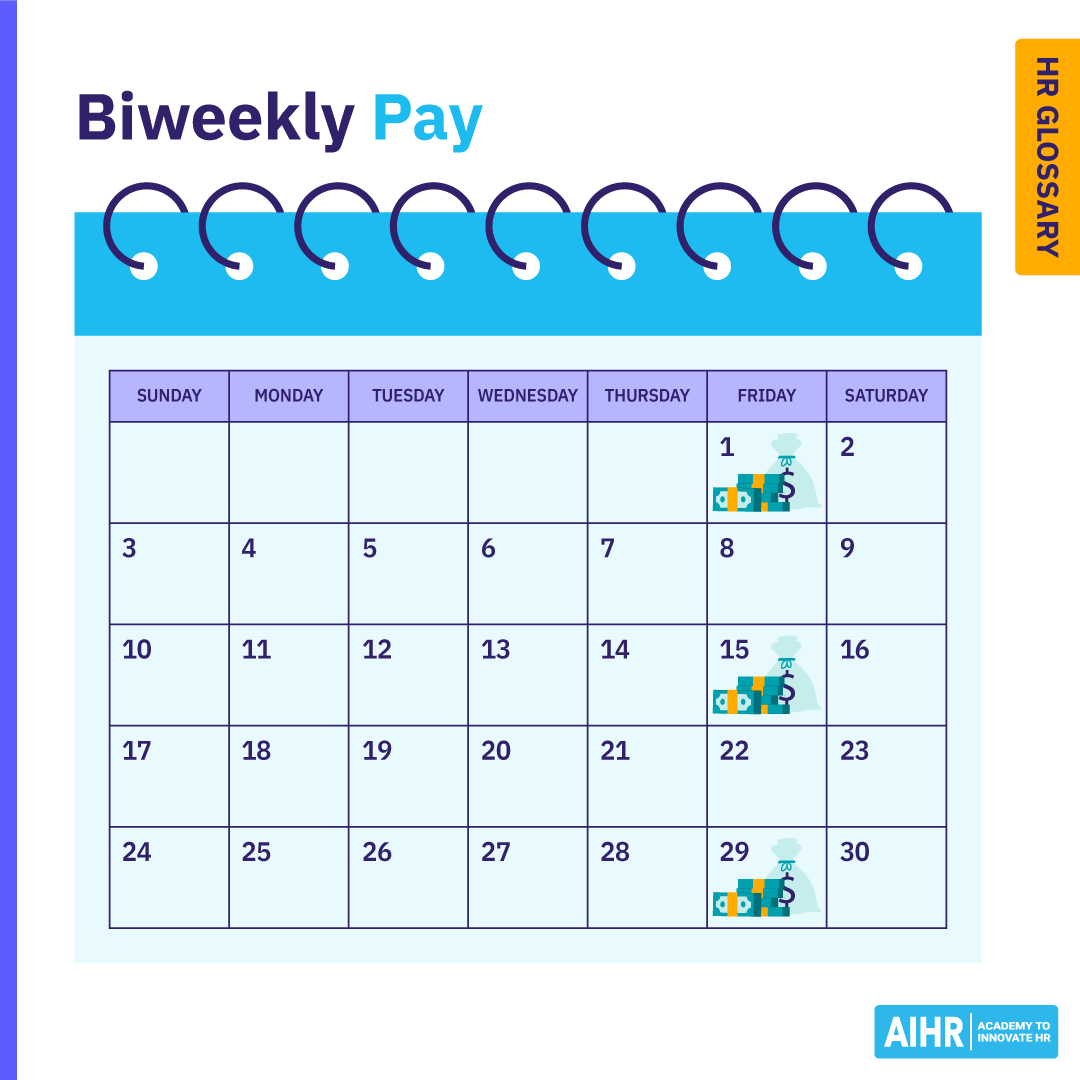

Understanding biweekly payments is fundamental for anyone involved in the financial ecosystem, particularly within industries that rely on recurring revenue streams and consistent operational funding. In essence, “biweekly” refers to a payment schedule that occurs every two weeks. This results in twenty-six (26) payment cycles per year, as opposed to the more common weekly (52 payments) or monthly (12 payments) schedules. This particular cadence offers a distinct set of advantages and considerations for both the payer and the payee.

The Biweekly Payment Structure in Detail

The biweekly payment structure is built around a simple arithmetic: dividing the total annual amount to be paid by twenty-six. For individuals receiving a salary, this means their annual income is split into twenty-six equal installments. While seemingly straightforward, this can have subtle but significant impacts on budgeting and financial planning.

Understanding the “Extra Paycheck” Phenomenon

A common point of interest and occasional confusion with biweekly payments arises from the fact that most years have fifty-two weeks. When you divide fifty-two by two, you get twenty-six. However, because the number of weeks in a year is not perfectly divisible by two in such a way that every month ends neatly on a payment day, there are often two years in a seven-year cycle where a biweekly payer will issue twenty-seven paychecks. This “extra paycheck” can be a welcome bonus for recipients, providing an opportunity for accelerated debt repayment, increased savings, or discretionary spending. However, it’s crucial for individuals to recognize this is not free money but rather an advance of their annual salary. Financial planners often advise recipients to either save this extra check or allocate it strategically rather than treating it as unexpected income.

Implications for Budgeting

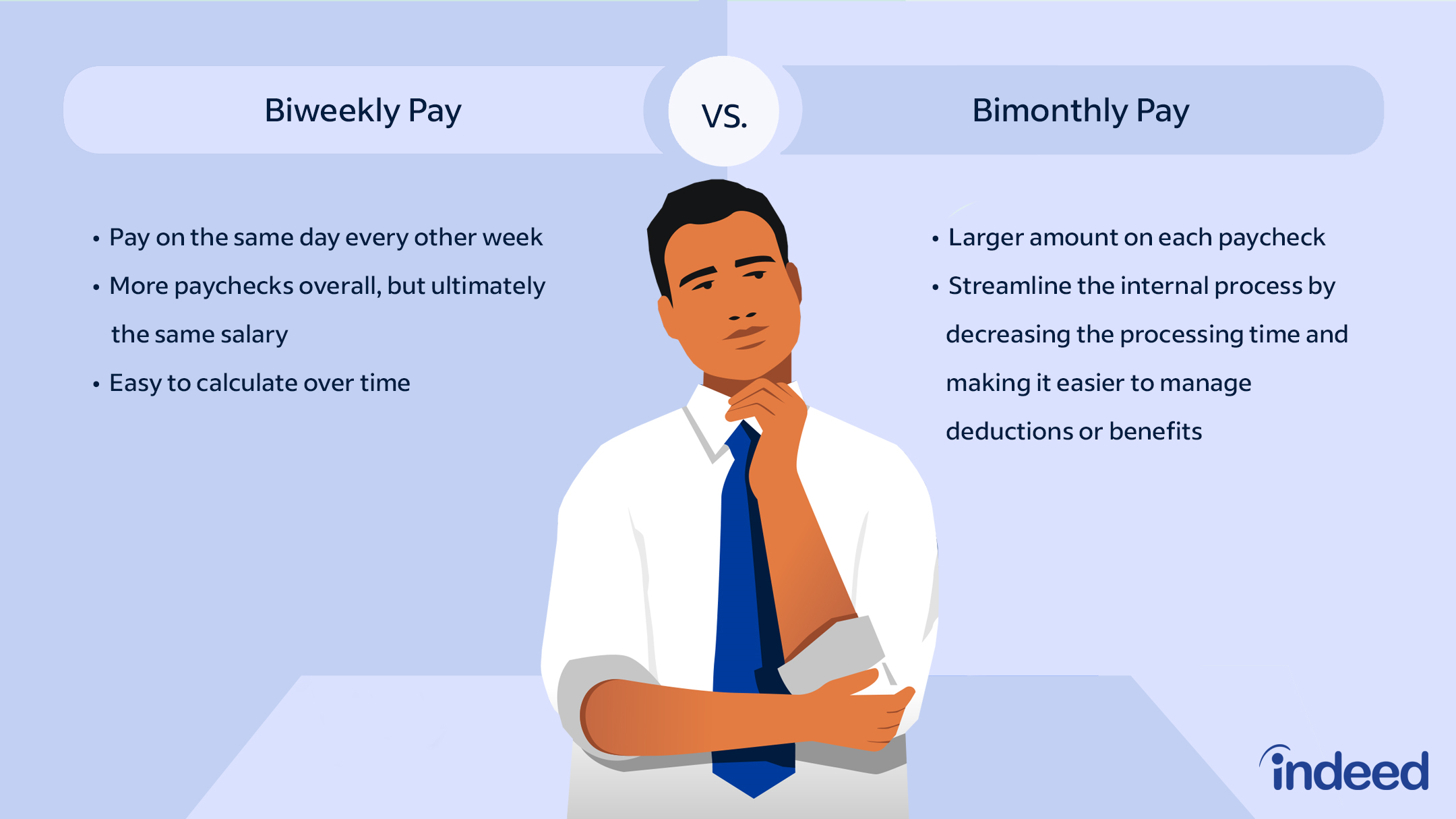

For individuals paid biweekly, budgeting requires careful attention to the timing of income. Unlike monthly payments, where a fixed amount arrives predictably each month, biweekly payments mean that some months will have two paychecks, and others will have three. This fluctuation necessitates a more flexible budgeting approach. Many find it beneficial to budget based on a “three-paycheck month” and then use the surplus from two-paycheck months for savings or to meet financial goals. Alternatively, some choose to average their income over the month, setting aside the extra funds from three-paycheck months to supplement the months with only two.

Employer Perspectives and Advantages

From an employer’s standpoint, implementing a biweekly payroll system offers several administrative and financial benefits.

Cash Flow Management

One of the primary advantages for businesses is improved cash flow management. By distributing payroll every two weeks, companies can align their outgoing cash for wages more closely with their incoming revenue streams, especially if their own business cycle operates on a similar semi-monthly or bi-weekly basis. This can lead to more efficient working capital utilization and reduced reliance on short-term financing.

Reduced Administrative Burden (Compared to Weekly)

While weekly payroll processing involves more frequent transactions and thus a higher administrative burden, biweekly processing strikes a balance. It offers more frequent payroll runs than monthly, which can be advantageous for employee morale and immediate financial needs, without the intensive administrative overhead of a weekly system. This allows payroll departments to manage their workload more effectively, reducing the potential for errors and streamlining the overall process.

Employee Morale and Retention

For employees, receiving a paycheck every two weeks can be a significant factor in their financial well-being and job satisfaction. It provides a more immediate reward for their labor compared to waiting a full month. This consistent cash flow helps employees meet their short-term financial obligations more easily, potentially reducing financial stress and improving morale. In a competitive job market, offering a biweekly payroll option can also be a subtle but effective tool for attracting and retaining talent.

Tax Withholding Considerations

Tax withholding can also be influenced by the biweekly payment schedule. Tax tables are typically designed based on the frequency of payment. When using biweekly tax tables, the amount withheld per paycheck is generally lower than if the same annual salary were paid weekly, because the employer is prorating the annual tax liability across twenty-six pay periods rather than fifty-two. This can result in a larger net paycheck for the employee. However, it’s crucial that the total annual withholding accurately reflects the individual’s tax liability. Over-withholding can lead to a large refund at tax time, effectively a loan to the government, while under-withholding can result in an unexpected tax bill. Therefore, individuals paid biweekly should review their tax withholdings periodically, especially if their financial situation or tax bracket changes.

Biweekly Payments in Different Contexts

The concept of “paid biweekly” extends beyond traditional employee salaries and can be found in various financial arrangements, including loan repayments, alimony, and rental agreements.

Loan and Mortgage Repayments

Many mortgage lenders offer borrowers the option to make biweekly payments on their loans. This is often pitched as a way to pay off a mortgage faster and save on interest. The typical biweekly mortgage plan involves setting up an automatic payment for half of the monthly mortgage payment every two weeks. Since there are twenty-six biweekly periods in a year, this results in twenty-six half-payments, which is equivalent to thirteen full monthly payments annually, instead of the standard twelve. This extra payment each year is applied directly to the principal balance, accelerating the loan’s amortization schedule. Over the life of a 30-year mortgage, this can shave several years off the repayment term and save tens of thousands of dollars in interest. It’s important for borrowers to understand the specifics of such plans, as some may charge administrative fees. A more direct and often fee-free approach is to simply make one extra monthly principal payment per year, or to divide the monthly payment by twelve and add that amount to each monthly payment.

Alimony and Child Support

In some jurisdictions, alimony or child support payments may be structured on a biweekly basis. This can provide a more consistent and manageable income stream for the recipient, helping them to budget for recurring expenses more effectively. For the payer, it can align with their own payroll cycles, making it easier to meet their obligations without financial strain. The court orders typically specify the exact amount and frequency of these payments, and adherence to the schedule is legally mandated.

Rental Agreements and Subscription Services

While less common for residential leases, some commercial rental agreements or short-term property rentals might be structured with biweekly payment terms. Similarly, some subscription-based services, particularly those with higher-priced tiers or for business-to-business clients, might offer biweekly billing cycles as an alternative to monthly payments. This can be a strategic choice for companies looking to manage their recurring expenses more closely with their operational cash flow.

Advantages and Disadvantages Summarized

The biweekly payment schedule, while offering distinct benefits, also comes with its own set of drawbacks that warrant careful consideration.

Advantages:

- Accelerated Debt Payoff: The potential for an “extra paycheck” or the structure of biweekly loan payments can lead to faster debt reduction and significant interest savings over time.

- Improved Cash Flow for Employers: Businesses can better align payroll expenses with revenue cycles, enhancing working capital management.

- More Frequent Access to Funds for Employees: Compared to monthly payments, biweekly income provides employees with more regular access to their earnings, aiding in short-term financial planning and reducing the likelihood of running out of money between pay periods.

- Potential for Increased Savings: The extra funds from a third paycheck in some months can be a powerful catalyst for boosting savings rates or investing.

- Simplified Budgeting (with adaptation): Once individuals adapt to the rhythm of biweekly payments, particularly by budgeting for the less frequent three-paycheck months, it can lead to a more structured financial approach.

Disadvantages:

- Budgeting Complexity: The variation in the number of paychecks per month can initially make budgeting more challenging for individuals who are not accustomed to it or who prefer a fixed monthly income.

- Potential for Overspending: The psychological impact of receiving a larger amount of money more frequently might lead some individuals to overspend if they do not maintain strict financial discipline.

- Administrative Overhead for Employers (vs. Monthly): While less than weekly, biweekly payroll processing still requires more frequent administrative effort than a monthly system.

- Tax Withholding Nuances: While generally resulting in lower per-paycheck withholding, it’s crucial for individuals to ensure their annual tax liability is met to avoid penalties.

- Misunderstanding of “Extra Paycheck”: Some recipients may mistakenly view the occasional third paycheck as a bonus, leading to unsustainable spending habits rather than recognizing it as an advance of their annual salary.

In conclusion, the biweekly payment schedule is a prevalent financial structure that offers a unique rhythm of income and expenditure. Whether for employees receiving their wages, individuals managing loan repayments, or businesses structuring their payroll, understanding the mechanics of biweekly payments—from the mathematical implications of twenty-six pay periods to the behavioral impacts on budgeting and financial planning—is essential for navigating personal and corporate finances effectively. By embracing its structure and planning accordingly, individuals and organizations can leverage the benefits of this payment cadence to achieve greater financial stability and meet their long-term objectives.