In the dynamic world of drone technology and innovation, businesses and consumers alike frequently encounter a myriad of regulatory and financial considerations. Among these, understanding local tax structures is paramount, especially for entities operating or purchasing within specific jurisdictions. This article delves into “What is Michigan Sales Tax,” specifically examining its implications and nuances for the burgeoning drone technology and innovation sector within the state. Far from being a mere administrative detail, Michigan’s sales tax framework can significantly influence investment decisions, operational costs, and the overall economic viability for companies pioneering advancements in unmanned aerial vehicles (UAVs), remote sensing, AI-driven flight, and other related innovative technologies. As Michigan actively seeks to position itself as a hub for advanced manufacturing and high-tech industries, a clear grasp of its sales tax policies is essential for fostering growth and ensuring compliance within this rapidly evolving field.

The Foundation of Michigan Sales Tax and its Relevance to Emerging Technologies

Michigan’s sales tax is a fundamental component of its state revenue, imposed on the retail sale of tangible personal property and certain services. For the drone technology and innovation sector, this broad definition immediately raises questions about what constitutes “tangible personal property” in an industry increasingly reliant on software, data, and intellectual property. Understanding the core principles of this tax is the first step for any drone manufacturer, developer, or consumer in Michigan.

Core Principles of Sales Tax Application

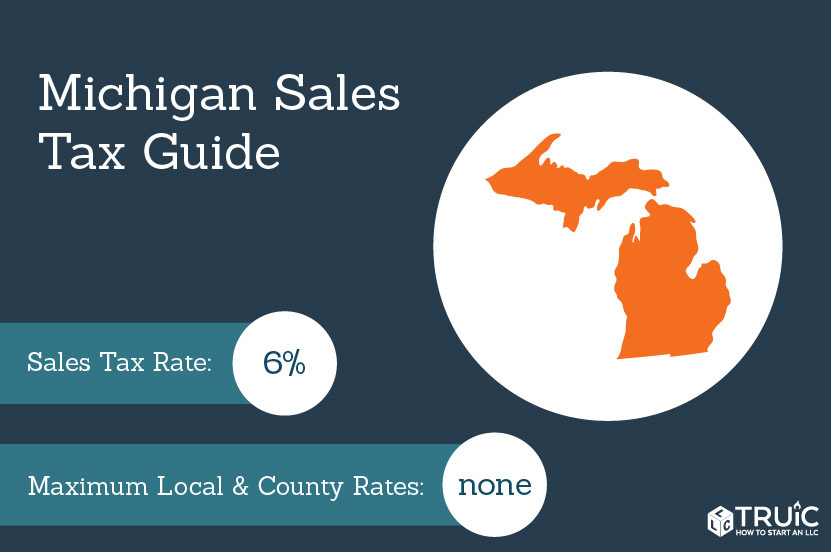

At its heart, Michigan’s sales tax is a 6% levy on the gross proceeds of all retail sales of tangible personal property. This tax is generally collected by the seller from the purchaser at the time of sale and remitted to the Michigan Department of Treasury. The burden of payment ultimately falls on the consumer, but the responsibility for collection and remittance rests with the seller. For drone technology, this means that the physical drone itself – the quadcopter, its frame, motors, propellers, and integrated hardware like cameras or sensors – is clearly tangible personal property subject to sales tax when sold at retail.

However, the “retail sale” definition is crucial. It refers to a sale for consumption or use, not for resale. This distinction becomes vital for businesses within the drone tech supply chain. A sale from a component manufacturer to a drone assembler is typically a wholesale transaction, not subject to sales tax if the assembler provides a valid resale certificate. Only the final sale to the end-user – whether an individual hobbyist, a commercial aerial mapping service, or an agricultural drone operator – incurs the sales tax.

Identifying Taxable Transactions in the Drone Sector

The challenge for the drone industry lies in identifying precisely what aspects of a transaction are taxable. While the hardware component of a drone is straightforward, many innovative drone systems involve a significant software or service element. For instance, a drone sold with pre-loaded, proprietary flight control software, or a subscription service for advanced data analytics processed by the drone, presents a more complex scenario.

If software is delivered electronically or via download, Michigan law generally considers it a non-taxable service or intangible, unless it is part of a bundled transaction where tangible personal property is the primary item. If the software is integrated into the drone hardware and is essential for its basic operation, it’s often considered part of the taxable tangible personal property. Services, such as drone piloting, data collection (e.g., mapping, inspection), or post-processing of drone-acquired data, are generally not subject to Michigan sales tax if they are distinct from the sale of the drone itself. However, if these services are mandatory and inseparable from the sale of a tangible drone system, they might be included in the taxable base. This distinction requires careful analysis, often necessitating consultation with tax professionals familiar with high-tech sales.

Sales Tax Impact on Drone Manufacturers and Innovative Tech Developers

For companies engaged in the manufacturing and development of drone technology within Michigan, sales tax compliance extends beyond simply collecting tax on final sales. It impacts their entire supply chain, from sourcing raw materials to selling advanced systems, and navigating intricate rules regarding intercompany transactions and the treatment of intellectual property.

Sourcing Rules for Drone Component Sales

Manufacturers often source components from various suppliers, both in and out of Michigan. Michigan’s sourcing rules determine where a sale is considered to have occurred, which in turn dictates whether Michigan sales tax applies. Generally, if the tangible personal property (e.g., drone components like microprocessors, specialized camera modules, or carbon fiber frames) is received by the purchaser in Michigan, then Michigan sales tax is due, assuming it’s a retail sale. If a Michigan-based drone manufacturer purchases components from an out-of-state supplier, and these components are shipped directly to the manufacturer in Michigan for use in their production process, the manufacturer would typically provide a resale certificate, exempting the transaction from sales tax. This exemption is critical for avoiding cascading taxes within the production chain, as the tax is intended to be applied only once at the retail level.

However, manufacturers must maintain meticulous records of resale certificates and ensure that purchased items are indeed intended for resale or direct incorporation into products for resale. Misclassifications can lead to audits and penalties, emphasizing the need for robust internal compliance procedures.

Taxable Services vs. Non-Taxable Intellectual Property

A significant challenge for innovative tech developers in the drone space is differentiating between taxable services and non-taxable intellectual property (IP). The creation of custom software, algorithms for autonomous flight, AI models for image recognition, or specialized drone designs often falls under the umbrella of IP. When a drone tech company licenses or sells these intangible assets, such transactions are typically not subject to Michigan sales tax, as they do not involve the transfer of tangible personal property.

However, if the IP is delivered on a tangible medium (e.g., a USB drive, a CD-ROM) and the medium itself is sold, or if the IP is bundled inextricably with a tangible product whose primary value is the IP, careful consideration is needed. For example, if a company develops a unique drone design and sells the blueprints as a physical document, that physical document might be taxable. More commonly, if a custom software solution is sold embedded within a specialized drone controller, the entire package could be subject to sales tax. Developers must structure their contracts and invoicing to clearly separate tangible goods from intangible IP or services to ensure accurate tax treatment and avoid unintended liabilities.

Consumer and Business Perspectives: Purchasing Drones and Advanced Systems in Michigan

For both individual consumers and businesses acquiring drones or advanced drone systems in Michigan, understanding sales tax obligations is essential for budgeting and compliance. The nature of the purchaser and the intended use of the drone significantly influence whether sales tax is applied and how.

Understanding End-User Sales Tax Liabilities

When an individual in Michigan purchases a drone, whether for recreational flying, photography, or educational purposes, from a retail store or an online vendor, they are typically liable for the 6% Michigan sales tax. This applies to the drone itself, as well as any accessories (batteries, propellers, controllers, carrying cases) and often pre-packaged software that comes with it. If the purchase is made from an out-of-state vendor that does not collect Michigan sales tax, the consumer is generally responsible for remitting a corresponding use tax to the state. The use tax is Michigan’s counterpart to sales tax, levied on items purchased out-of-state for use, storage, or consumption within Michigan, where sales tax was not paid. While often overlooked by individual consumers for smaller purchases, it is a legal obligation that can be enforced, particularly for larger-ticket items like advanced drone systems.

Business-to-Business Transactions and Resale Certificates

For businesses that purchase drones or drone components, the application of sales tax depends on their role and the intended use. A company purchasing drones to use in its own operations (e.g., a construction firm buying drones for site surveying, or a security company using them for surveillance) is the end-user and must pay sales tax on the purchase.

However, if a business purchases drones or components with the intent to resell them in their original form or as part of a larger drone system, they can typically claim a sales tax exemption by providing a valid resale certificate to their supplier. This certificate attests that the purchaser is a registered seller and the items are being acquired for resale, thus shifting the sales tax obligation to the final retail sale. Businesses acting as distributors, resellers, or integrators of drone technology rely heavily on this mechanism to avoid paying sales tax multiple times on the same item within the supply chain. Accurate documentation and proper issuance of resale certificates are critical to avoid tax liabilities and potential audits for both the buyer and the seller.

Navigating Exemptions and Incentives for R&D and Strategic Investments

Michigan, recognizing the importance of fostering innovation and manufacturing, offers several exemptions and incentives that can significantly benefit the drone technology sector. Understanding and properly utilizing these provisions can reduce operational costs and encourage strategic investments in research and development.

Manufacturing Exemptions and Their Application to Drone Production

One of the most significant exemptions for drone manufacturers in Michigan is the industrial processing exemption. This exemption applies to tangible personal property (e.g., machinery, equipment, tools, electricity, and even certain supplies) that is used or consumed in the industrial processing of other tangible personal property that is ultimately offered for sale at retail. For drone manufacturers, this means that the specialized robots, 3D printers, assembly line equipment, testing apparatus, and even the electricity consumed in the direct manufacturing process of drones can be exempt from sales tax.

To qualify, the equipment or property must be directly used in the transformation of raw materials or components into a finished product. This can include everything from the initial fabrication of drone frames to the final assembly and testing of the integrated flight systems. Properly claiming this exemption requires precise identification of eligible assets and maintaining detailed records to substantiate the claim. It’s a powerful incentive that reduces the capital expenditure and ongoing operational costs for drone manufacturing facilities in Michigan, making the state a more attractive location for production.

Potential Tax Relief for Innovative Research and Development

While Michigan does not have a broad sales tax exemption specifically for research and development (R&D) activities, certain aspects of R&D within the drone sector may still qualify for existing exemptions. For example, if R&D involves prototyping or the creation of tangible personal property that is ultimately intended for sale, some of the materials and equipment used in that “industrial processing” phase could potentially qualify for the manufacturing exemption, even if the R&D process itself is preliminary. Additionally, services related to R&D, being generally non-taxable, offer a natural form of tax relief.

Furthermore, Michigan offers various business tax incentives (like the Michigan Business Tax credit for R&D, though the MBT has been replaced by the Corporate Income Tax for most businesses, some credits remain or are replaced by similar programs) that indirectly support innovation. While these are not sales tax exemptions, they contribute to a more favorable overall fiscal environment for tech companies. Businesses heavily invested in drone R&D should actively explore all available state and local incentives, including those related to job creation, capital investment, and technological advancement, to maximize their financial advantages within Michigan’s competitive landscape.

Future Trends: Fiscal Policy, Economic Development, and Michigan’s Drone Industry

The intersection of fiscal policy and the burgeoning drone industry in Michigan is dynamic, influenced by technological advancements, evolving regulatory frameworks, and the state’s strategic economic development goals. Anticipating these future trends is crucial for businesses looking to thrive in this innovative sector.

The Role of Tax Policy in Fostering Innovation Hubs

Michigan’s economic development strategies increasingly focus on attracting and retaining high-tech industries, including advanced manufacturing, mobility, and aerospace—sectors where drone technology plays a pivotal role. As such, future fiscal policies may become even more finely tuned to support innovation. This could manifest as targeted sales tax exemptions for specific emerging technologies, R&D equipment, or specialized software and services critical to the drone ecosystem. Policymakers recognize that a favorable tax environment can be a significant differentiator in attracting investment and talent. Therefore, advocates for the drone industry in Michigan should actively engage with state legislative bodies to highlight the unique needs and contributions of the sector, potentially influencing future tax reforms that directly benefit drone tech companies. Streamlined processes for claiming exemptions and clearer guidance on complex digital and service transactions could also emerge, reducing compliance burdens.

Anticipating Changes and Opportunities for Drone Tech Companies

As drone technology continues its rapid evolution, so too will the economic landscape and, potentially, the tax code. The increasing prevalence of drone-as-a-service models, where companies lease or provide drones along with operational support and data analytics, could prompt new interpretations or specific guidance regarding sales vs. service taxation. The growth of autonomous drone fleets and the integration of AI could also bring new considerations for what constitutes taxable software or intellectual property versus an embedded, non-taxable functionality.

For drone tech companies in Michigan, this dynamic environment presents both challenges and opportunities. Proactive engagement with tax professionals, industry associations, and state regulatory bodies will be essential to stay ahead of changes. Companies that effectively navigate the current sales tax framework, anticipate future shifts, and strategically leverage available exemptions and incentives will be better positioned to innovate, grow, and contribute to Michigan’s aspirations as a leading hub for advanced technological development. The sustained success of the drone industry in Michigan hinges not just on technological prowess, but also on astute financial and regulatory management.