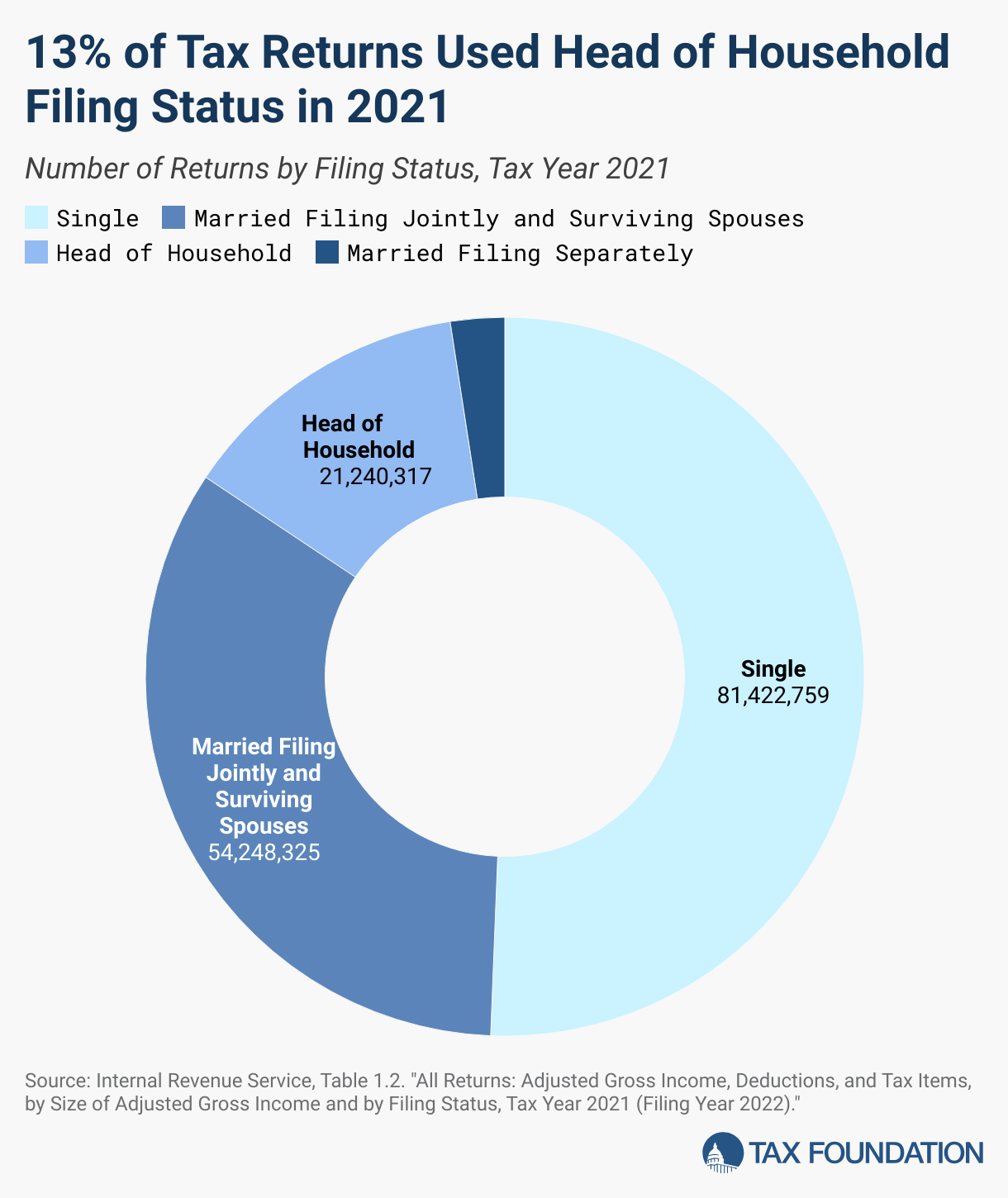

The U.S. tax system offers several filing statuses that individuals can use when preparing their tax returns. These statuses significantly impact the tax brackets, standard deduction amounts, and overall tax liability. Among these, the Head of Household filing status is a particularly advantageous option for certain unmarried taxpayers who support a qualifying child. Understanding the criteria and benefits of this status is crucial for optimizing tax outcomes. This guide delves into the intricacies of the Head of Household filing status, exploring who qualifies, the requirements, and how it compares to other common filing statuses.

Understanding the Head of Household Filing Status

The Head of Household (HOH) filing status is designed for unmarried individuals who pay more than half the costs of keeping up a home for the year and who have a qualifying child living with them for more than half the year. This status is not simply for single individuals; it recognizes the financial responsibilities undertaken by those who are the primary caregivers for dependents. The IRS provides this status as a way to offer tax relief and acknowledge the significant financial burden of maintaining a household for a dependent.

Key Eligibility Requirements

To qualify for the Head of Household status, a taxpayer must meet a specific set of criteria, which can be broadly categorized into three main areas: marital status, household upkeep costs, and the presence of a qualifying person.

Marital Status

The most fundamental requirement is that the taxpayer must be considered unmarried on the last day of the tax year. This generally means that the taxpayer is not married, is separated from their spouse but not divorced, or is a surviving spouse. Divorced individuals who have not remarried can qualify if they meet the other criteria. Similarly, individuals who are legally separated under a decree of separation or a decree of divorce are considered unmarried for tax purposes.

Household Upkeep Costs

A crucial element of qualifying for HOH status is demonstrating that the taxpayer pays more than half the cost of keeping up a home for the entire year. “Keeping up a home” refers to the expenses incurred to maintain the taxpayer’s main home, which is also the main home of a qualifying person. These costs include expenses such as:

- Rent or mortgage interest

- Property taxes

- Homeowners insurance

- Utilities (electricity, gas, water, etc.)

- Repairs and maintenance

- Food eaten in the home

- Other household expenses directly related to the upkeep of the home

It’s important to note that the costs of clothing, education, medical care, and life insurance are generally not considered household upkeep costs, even if paid for the qualifying person. The taxpayer must prove they contributed more than 50% of these expenses. If another individual (such as a non-custodial parent or relative) also contributes to these costs, the taxpayer must ensure their contribution exceeds the other party’s.

The Qualifying Person

The presence of a qualifying person is perhaps the most defining characteristic of the Head of Household status. Generally, this person must be one of the taxpayer’s children (son, daughter, stepchild, foster child, or a descendant of any of them) whom the taxpayer can claim as a dependent.

- Living with the Taxpayer: The qualifying child must have lived with the taxpayer in the main home for more than half of the tax year. There are exceptions to this rule for temporary absences due to illness, education, business, or military service.

- Not Meeting Certain Joint Return Tests: The qualifying child cannot have filed a joint return for the tax year, unless the joint return was filed only to claim a refund of withheld income tax or estimated tax paid.

- Dependence Test: The taxpayer must be able to claim the child as a dependent. This usually means the child received more than half of their support from the taxpayer and meets certain other dependency tests.

- Parental Relationship: The child must be the taxpayer’s son, daughter, stepchild, foster child, or a descendant of any of them (such as a grandchild).

Other Qualifying Persons: In some limited circumstances, a taxpayer may qualify for Head of Household status if they have another relative who lives with them for the entire year and whom the taxpayer can claim as a dependent, even if that person is not their child. This typically applies if the taxpayer is supporting a parent. In such cases, the taxpayer must also provide more than half the cost of keeping up the home for that relative, and that relative must be their mother, father, brother, sister, grandfather, grandmother, aunt, or uncle, or a child of any of them.

Common Scenarios for Qualifying

Several common scenarios illustrate who might qualify for the Head of Household filing status:

- Divorced or Separated Parents with Custody: A divorced or separated parent who has physical custody of their child for more than half the year and pays more than half of the household expenses generally qualifies. Even if the non-custodial parent claims the child as a dependent using a Multiple Support Agreement or for other reasons, the custodial parent may still qualify if they meet the other HOH criteria.

- Unmarried Parents Living Together: If an unmarried couple lives together with their child, and one parent meets the HOH requirements (i.e., pays more than half the household costs and the child lives with them), they can file as Head of Household. The other parent would likely file as Single.

- Widowers with Dependent Children: A surviving spouse who has not remarried and maintains a home for their dependent child can qualify for Head of Household status for the two tax years following the year of their spouse’s death, provided they meet the other criteria. Before that, they might qualify for the more favorable Qualifying Widow(er) status.

- Individuals Supporting an Elderly Parent: If a taxpayer provides a home for an unmarried parent and pays more than half the cost of keeping up that home for the entire year, and the parent is their dependent, they may qualify for Head of Household status, even if the parent doesn’t live with them. For example, if a taxpayer pays for a parent’s assisted living facility and can claim the parent as a dependent.

Benefits of Head of Household Filing Status

The Head of Household filing status offers significant tax advantages compared to the Single filing status. These benefits primarily stem from:

- Lower Tax Rates: The tax brackets for Head of Household filers are wider and more favorable than those for single filers. This means that a larger portion of income is taxed at lower rates, resulting in a lower overall tax liability.

- Higher Standard Deduction: The standard deduction amount for Head of Household filers is higher than for single filers. The standard deduction is a fixed dollar amount that reduces a taxpayer’s taxable income. A higher standard deduction directly translates to more income being shielded from taxation.

- Certain Tax Credits: Some tax credits may be more accessible or offer higher benefits to taxpayers filing as Head of Household, though this is not a universal rule and depends on the specific credit.

For instance, imagine two unmarried individuals with the same income and no dependents. If one qualifies for Head of Household and the other files as Single, the Head of Household filer will almost certainly pay less tax due to the more favorable tax brackets and higher standard deduction.

Head of Household vs. Other Filing Statuses

Understanding how Head of Household compares to other filing statuses is essential for making informed decisions.

- Single: This status is for unmarried individuals who do not qualify for Head of Household or Qualifying Widow(er) status. It generally has the least favorable tax brackets and the lowest standard deduction among the common statuses.

- Married Filing Separately (MFS): This status is for married individuals who choose to file separate tax returns. While it offers individual control over tax liability, it often results in higher taxes and fewer available deductions and credits compared to Married Filing Jointly. It is rarely more advantageous than HOH for an unmarried person.

- Married Filing Jointly (MFJ): This status is for married couples who file one tax return together. It typically offers the most favorable tax rates and highest standard deduction, but it is only available to married couples.

- Qualifying Widow(er) with Dependent Child: This status is available to a surviving spouse who has not remarried and who has a dependent child. It allows the survivor to use the most favorable tax rates and standard deduction for married couples for up to two years after the death of their spouse, provided they meet specific criteria. It is generally more beneficial than Head of Household for those who qualify.

If a taxpayer meets the criteria for Head of Household, it is almost always more advantageous to file as HOH than as Single. The benefits are substantial enough to significantly reduce tax burdens.

Common Pitfalls and Considerations

Despite its advantages, the Head of Household status can be a source of confusion and errors.

- Misinterpreting “Unmarried”: Individuals who are legally married but separated may mistakenly believe they qualify as unmarried. However, unless a legal decree of separation or divorce is in place, they are still considered married.

- Inaccurate Household Cost Calculations: Underestimating or miscalculating household upkeep costs is a common error. Taxpayers must diligently track all eligible expenses to ensure they meet the “more than half” requirement.

- Dependence Rules: Confusion around the complex rules for claiming a dependent can lead to improper HOH filings. It’s crucial to understand who qualifies as a dependent and under what conditions.

- Temporary Absences: Taxpayers may not realize that temporary absences of a qualifying child from the home (e.g., for college) do not necessarily disqualify them from HOH status, provided the home remains the child’s principal residence.

It is often advisable to use tax preparation software or consult a tax professional to ensure accurate filing, especially when navigating the nuances of the Head of Household status. The IRS provides extensive resources and publications, such as Publication 501, Dependents, Standard Deduction, and Filing Information, which can offer further clarification. By understanding and correctly applying the criteria, eligible taxpayers can effectively utilize the Head of Household filing status to their financial advantage.