In the complex landscape of health insurance, understanding the myriad of plan types is crucial for making informed decisions about one’s healthcare and financial well-being. Among the prominent options available today, High Deductible Health Plans (HDHPs) have garnered significant attention, often debated for their cost-saving potential and their unique structure. An HDHP is, at its core, a health insurance plan characterized by a higher deductible than traditional insurance plans. This means that individuals or families must pay more out-of-pocket for medical services before their insurance coverage kicks in. However, this higher deductible is typically offset by lower monthly premiums, making HDHPs an attractive option for certain demographics.

The appeal of HDHPs extends beyond just lower monthly costs. They are often paired with Health Savings Accounts (HSAs), creating a powerful duo that not only provides coverage but also offers a tax-advantaged way to save for future medical expenses. This combination encourages consumers to be more proactive and financially savvy about their healthcare decisions, fostering a sense of ownership over their medical spending. Delving deeper into the mechanics, benefits, and considerations of HDHPs is essential for anyone evaluating their health insurance choices in today’s dynamic healthcare environment. This article aims to demystify HDHPs, providing a comprehensive overview of how they function, their advantages and disadvantages, and who might benefit most from adopting such a plan.

Understanding the Core Concepts of HDHP

To truly grasp what an HDHP entails, it’s vital to dissect its fundamental components and understand how they interact to define the plan’s structure and your financial responsibilities. Unlike conventional health insurance plans that might have lower deductibles and higher co-pays, HDHPs pivot on the principle of shifting more immediate costs to the consumer in exchange for long-term savings potential.

Defining High Deductibles

The most distinguishing feature of an HDHP is its “high deductible.” A deductible is the amount of money you must pay for covered healthcare services before your insurance company begins to pay. For a plan to qualify as an HDHP, the Internal Revenue Service (IRS) sets minimum deductible amounts and maximum out-of-pocket limits annually. For example, in a given year, a plan might need a minimum deductible of over $1,500 for an individual and over $3,000 for a family to be considered an HDHP. These figures are significantly higher than what you’d typically find in a traditional Preferred Provider Organization (PPO) or Health Maintenance Organization (HMO) plan.

The implication of a high deductible is straightforward: you are responsible for 100% of your medical costs, up to the deductible amount, for most services (excluding preventive care, which is usually covered before the deductible is met). This upfront financial responsibility encourages policyholders to be more mindful of their healthcare usage and costs.

How Deductibles, Coinsurance, and Out-of-Pocket Maximums Interact

Beyond the deductible, an HDHP operates with other financial levers that determine your overall cost sharing.

- Coinsurance: Once you’ve met your deductible, your insurance doesn’t necessarily cover 100% of subsequent costs. Instead, you’ll typically pay a percentage of the cost for covered services, known as coinsurance, while your insurance pays the rest. For instance, an 80/20 coinsurance means your plan pays 80%, and you pay 20% until you reach your out-of-pocket maximum.

- Out-of-Pocket Maximum: This is the absolute ceiling on how much you could pay for covered medical expenses in a policy year. This includes your deductible, copayments, and coinsurance. Once you reach this maximum, your insurance company pays 100% of the cost for all covered services for the remainder of the year. The IRS also sets maximum limits for the out-of-pocket maximum for HDHPs, which are higher than for many traditional plans but provide a crucial safety net against catastrophic medical bills.

Understanding these components together reveals the full financial picture of an HDHP. You pay your deductible first, then coinsurance until you hit your out-of-pocket maximum, at which point your plan covers everything. This structure places a significant initial burden on the insured but provides complete coverage once the annual limit is reached.

The Symbiotic Relationship with Health Savings Accounts (HSAs)

One of the most compelling aspects of HDHPs is their eligibility for pairing with a Health Savings Account (HSA). This combination is often cited as a key benefit, transforming a simple insurance plan into a powerful financial tool for healthcare management and long-term savings.

What is an HSA and How Does it Work?

An HSA is a tax-advantaged savings account that can be used for qualified medical expenses. To be eligible for an HSA, you must be enrolled in an HDHP and have no other disqualifying health coverage. The funds contributed to an HSA are tax-deductible, meaning they reduce your taxable income. The money in the account grows tax-free, and withdrawals for qualified medical expenses are also tax-free. This triple tax advantage makes HSAs incredibly attractive.

You can contribute money to your HSA, and so can your employer. These funds never expire, rolling over year after year, even if you change employers or health plans. This portability and longevity distinguish HSAs from Flexible Spending Accounts (FSAs), which typically operate on a “use it or lose it” basis annually. The ability to invest HSA funds, much like a 401(k) or IRA, further enhances their long-term savings potential, making them a retirement savings vehicle for healthcare costs.

Maximizing the Benefits of the HDHP-HSA Combo

The synergy between an HDHP and an HSA is profound. With an HDHP, you face higher out-of-pocket costs before your insurance kicks in. The HSA provides a dedicated, tax-advantaged fund to cover these costs. For individuals who anticipate low medical expenses, they can let their HSA funds grow, potentially investing them, and save them for future healthcare needs, including those in retirement. For those who do incur significant medical costs, the HSA acts as a readily available reservoir of tax-free money to meet their deductible and coinsurance obligations.

This combination encourages consumers to be more engaged with their healthcare decisions. Since they are often paying cash directly from their HSA for services, they have a stronger incentive to shop around for services, compare prices, and question billing. This market-driven approach can lead to more cost-effective healthcare choices. Furthermore, the lower premiums of an HDHP can free up funds that can then be contributed to the HSA, reinforcing the savings cycle.

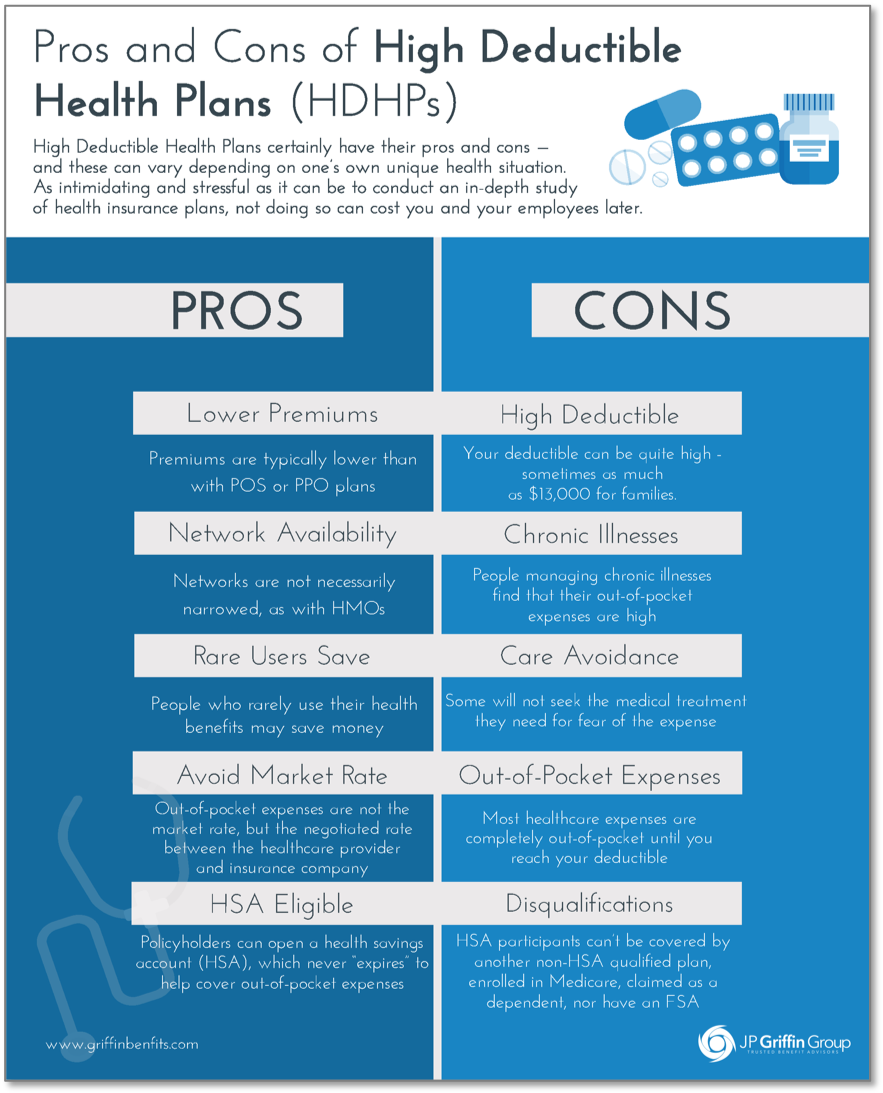

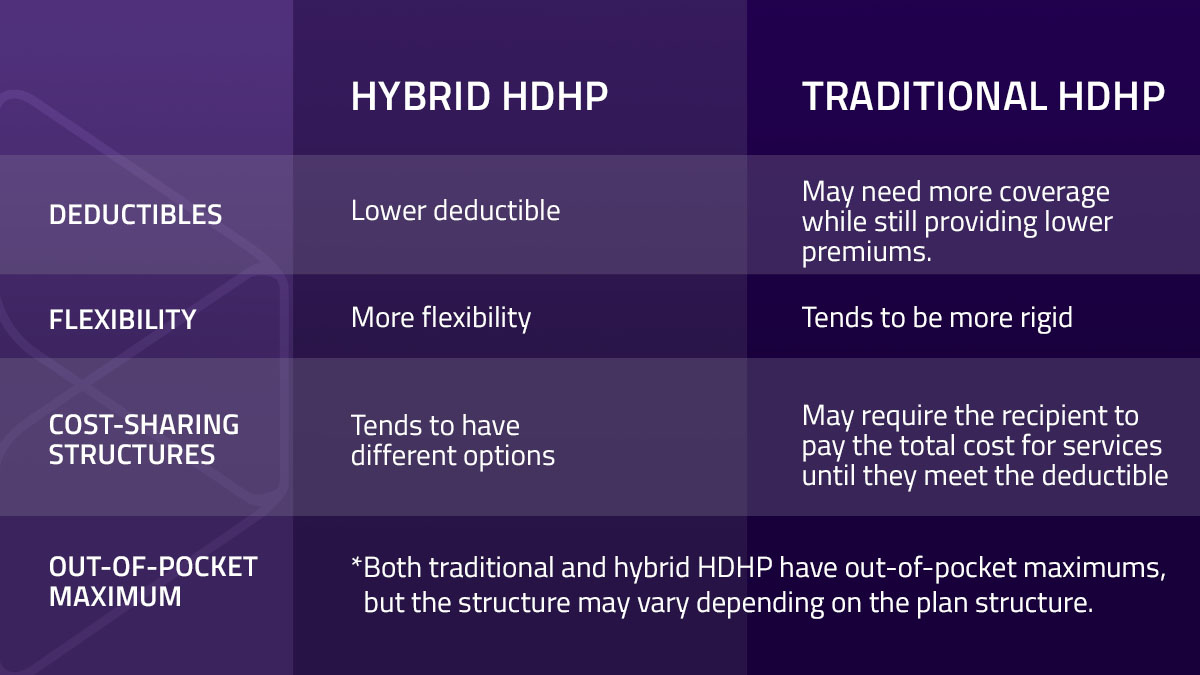

Weighing the Advantages and Disadvantages of HDHPs

Like any financial or insurance product, HDHPs come with a distinct set of pros and cons that make them suitable for some individuals and families, but less ideal for others. A balanced perspective is essential for making an informed choice.

Key Advantages: Cost Savings and Financial Control

The primary advantage of an HDHP is often the lower monthly premiums. For many, especially younger individuals or those with consistently good health, these lower upfront costs represent significant savings over a year. These savings can then be channeled into an HSA, amplifying the financial benefits.

Secondly, HDHPs, particularly when paired with an HSA, offer unparalleled financial control and tax advantages. The triple tax benefit of HSAs (tax-deductible contributions, tax-free growth, tax-free withdrawals for medical expenses) is a powerful incentive. The ability to save and invest these funds for future medical needs, including retirement, provides a long-term financial planning tool.

Lastly, HDHPs can promote consumer engagement and cost awareness. Because you’re paying more out-of-pocket initially, you’re likely to be more attuned to the cost of services, potentially leading you to seek out lower-cost providers or question unnecessary procedures.

Potential Disadvantages and Risks

Despite their benefits, HDHPs are not without their drawbacks. The most significant is the high out-of-pocket financial burden before the deductible is met. For individuals or families with chronic conditions, unexpected illnesses, or frequent medical needs, meeting a high deductible can be a substantial financial strain, particularly early in the plan year. This could lead some to delay necessary medical care to avoid immediate costs, potentially exacerbating health issues.

Another concern is the complexity and learning curve. Understanding deductibles, coinsurance, out-of-pocket maximums, and the nuances of an HSA can be more challenging than a traditional plan with fixed co-pays. Misunderstanding these elements can lead to unexpected bills.

Finally, while HDHPs offer lower premiums, the total potential cost (premiums plus out-of-pocket maximum) can still be significant for those who end up needing extensive care, though the HSA can mitigate this if properly funded.

Who Should Consider an HDHP?

Deciding whether an HDHP is the right choice involves a careful assessment of one’s health status, financial situation, and risk tolerance. There are specific profiles for whom HDHPs tend to be an excellent fit, and others for whom they might pose significant challenges.

Ideal Candidates for HDHPs

HDHPs are often an excellent choice for healthy individuals and families who anticipate minimal medical expenses throughout the year. If you rarely visit the doctor beyond annual check-ups and generally don’t require prescription medications, the lower monthly premiums can lead to substantial savings. These individuals can effectively use the HSA to save for future, potentially larger, medical costs without frequently drawing from it in the present.

They are also highly beneficial for those who can afford to cover their deductible out-of-pocket if an unexpected medical event occurs. Having an emergency fund or being disciplined about contributing to an HSA to cover the deductible is crucial. This financial preparedness mitigates the primary risk associated with HDHPs.

Furthermore, individuals focused on long-term tax-advantaged savings will find the HSA component particularly appealing. The ability to invest funds and have them grow tax-free, then withdrawn tax-free for medical expenses, makes it a powerful retirement planning tool specifically for healthcare costs.

When an HDHP Might Not Be the Best Fit

Conversely, HDHPs may not be the optimal choice for individuals or families with chronic health conditions or those who anticipate frequent doctor visits, ongoing prescriptions, or regular medical procedures. For these groups, meeting a high deductible annually could result in significant upfront costs that outweigh the savings from lower premiums. The financial burden could be constant and substantial, potentially leading to deferral of necessary care.

Similarly, individuals with limited disposable income or no emergency savings may struggle with an HDHP. Without the financial buffer to cover the deductible, an unexpected illness or injury could lead to considerable financial distress or unmanageable debt. In such cases, a plan with higher premiums but lower deductibles and predictable co-pays might offer more financial security and peace of mind.

Lastly, those who prefer the predictability and simplicity of traditional plans with lower co-pays for every visit might find HDHPs less appealing. The emphasis on consumer engagement and cost awareness in HDHPs might feel like an added burden for those who prefer their insurance to handle most of the financial complexities from the outset.

In conclusion, HDHPs offer a distinctive approach to health insurance, emphasizing consumer involvement, cost awareness, and tax-advantaged savings, particularly through their association with HSAs. While they present an opportunity for significant savings and financial control for some, their high deductible structure demands careful consideration of one’s health status and financial preparedness. Understanding the nuances of HDHPs is paramount for anyone navigating the intricate world of health insurance and seeking a plan that aligns with their personal health and financial goals.