The concept of “growth” in economics is multifaceted and central to understanding the progress and development of economies. It fundamentally refers to the increase in the production of goods and services within an economy over a specific period. This increase is typically measured by the Gross Domestic Product (GDP), which represents the total monetary value of all finished goods and services produced within a country’s borders in a given time frame. However, GDP is just one metric, and a comprehensive understanding of economic growth involves delving deeper into its drivers, measurement nuances, and its implications for society.

Understanding Economic Growth

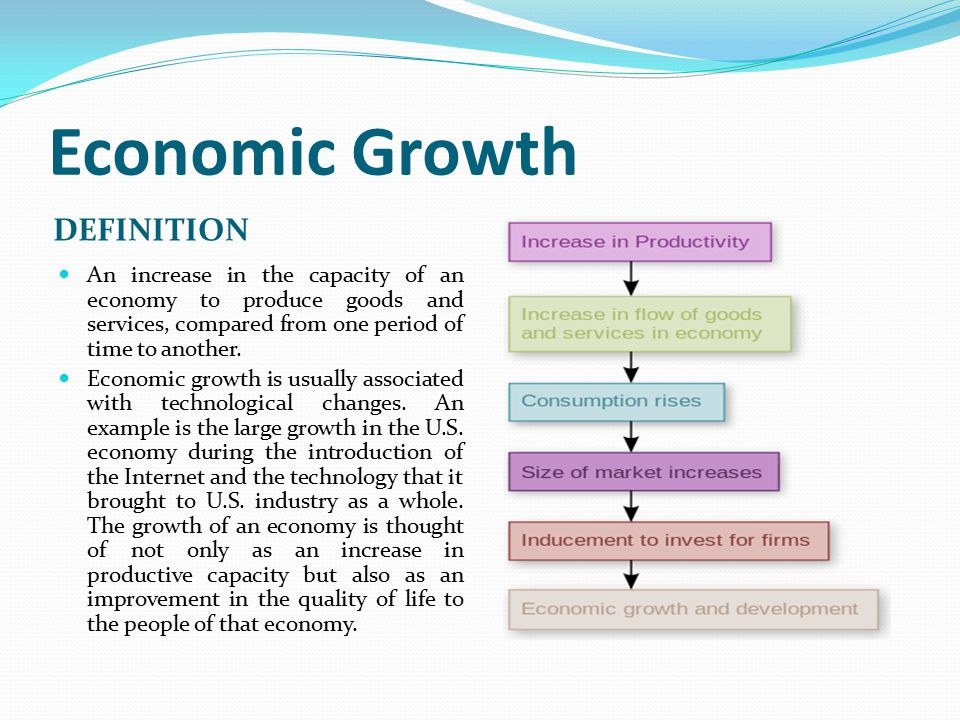

Economic growth signifies an expansion in the economy’s capacity to produce goods and services. It is not merely about an increase in the quantity of output but also about improvements in the quality and variety of goods and services available to consumers. This expansion allows for higher standards of living, increased employment opportunities, and greater overall prosperity.

Measuring Economic Growth: Beyond GDP

While GDP is the most commonly cited indicator of economic growth, it has its limitations.

Gross Domestic Product (GDP)

GDP is the sum of consumption, investment, government spending, and net exports. A positive change in GDP from one period to the next signifies economic growth. Conversely, a negative change indicates an economic contraction or recession. GDP can be measured in nominal terms (at current prices) or real terms (adjusted for inflation). Real GDP is the preferred measure for assessing growth as it removes the distorting effects of price changes.

Real GDP Growth Rate

The real GDP growth rate is the percentage change in real GDP from one period to the next. This is the most standard way economists quantify economic growth. For instance, a country experiencing a 3% real GDP growth rate means its economy produced 3% more goods and services in that period, after accounting for inflation.

Gross National Product (GNP)

GNP is similar to GDP but includes income earned by a country’s citizens and companies abroad, while excluding income earned by foreigners within the country. While less commonly used for measuring domestic growth, it provides a broader perspective on a nation’s overall economic output and earnings.

Per Capita Income

Growth in GDP does not always translate to improved living standards for every individual. Per capita income, which divides the total national income by the population, offers a better measure of the average economic well-being of individuals within an economy. A rising per capita income suggests that, on average, people are becoming wealthier.

Human Development Index (HDI)

Beyond purely economic metrics, the Human Development Index (HDI) offers a more holistic view of growth. It considers not only income but also life expectancy and educational attainment. True economic growth, in this broader sense, should lead to improvements in these crucial aspects of human well-being.

Drivers of Economic Growth

Several fundamental factors contribute to sustained economic growth:

Capital Accumulation

This refers to the increase in the stock of physical capital, such as machinery, buildings, and infrastructure, as well as human capital, which encompasses the skills, knowledge, and health of the workforce. Investment in new and improved capital allows for greater productivity and output.

Technological Advancements

Innovation and technological progress are powerful engines of growth. New technologies can lead to more efficient production methods, the creation of new goods and services, and the opening of new markets. Research and development (R&D) play a critical role in fostering these advancements.

Labor Force Growth

An increase in the size of the labor force, through population growth or increased participation rates, can contribute to economic growth by expanding the potential for production. However, growth in output per worker is generally considered more sustainable and indicative of genuine progress.

Natural Resources

The availability and effective utilization of natural resources can support economic growth, particularly in certain sectors. However, over-reliance on natural resources without diversification can lead to vulnerability and hinder long-term sustainable growth.

Institutional Quality

Strong institutions, including well-functioning legal systems, secure property rights, low levels of corruption, and efficient governance, are crucial for fostering an environment conducive to investment and innovation, thereby driving economic growth.

Types and Stages of Economic Growth

Economic growth is not a monolithic phenomenon; it manifests in different ways and can be observed across various stages of development.

Extensive vs. Intensive Growth

Extensive Growth

This type of growth occurs when an economy increases its output by using more inputs – more labor, more capital, more land. It’s like expanding a farm by clearing more land and hiring more workers. While it can lead to an overall increase in GDP, it doesn’t necessarily improve productivity or efficiency.

Intensive Growth

In contrast, intensive growth is driven by improvements in productivity and efficiency. This means producing more output with the same or fewer inputs. This is typically achieved through technological advancements, better management practices, and an educated and skilled workforce. Intensive growth is generally considered more sustainable and leads to higher per capita incomes.

Economic Development vs. Economic Growth

It is important to distinguish between economic growth and economic development.

Economic Growth

As discussed, economic growth is primarily concerned with the quantitative increase in the production of goods and services, often measured by GDP.

Economic Development

Economic development is a broader concept that encompasses qualitative improvements in the well-being of a population. It includes not only economic growth but also advancements in education, healthcare, poverty reduction, environmental sustainability, and social equity. A country can experience economic growth without significant economic development if the benefits are not widely shared or if it leads to negative externalities like environmental degradation.

Stages of Economic Growth

Economists have proposed various models to describe the stages of economic growth. One influential model is Walt Rostow’s Stages of Economic Growth, which outlines five stages:

Traditional Society

Characterized by subsistence agriculture, limited technology, and a rigid social structure.

Preconditions for Take-off

Emergence of an entrepreneurial class, increased investment in infrastructure, and development of new industries.

Take-off

Rapid industrialization, sustained investment, and significant technological advancements leading to self-sustaining growth.

Drive to Maturity

Diversification of the economy, continued technological progress, and rising standards of living.

Age of High Mass Consumption

Shift towards durable consumer goods and services, with a focus on welfare and individual pursuits.

Challenges and Implications of Economic Growth

While economic growth is generally desirable, it also presents challenges and has significant implications.

Distribution of Wealth and Income Inequality

One of the key challenges of economic growth is ensuring that its benefits are equitably distributed. Rapid growth can sometimes exacerbate income inequality if the gains accrue disproportionately to certain segments of the population, leading to social tensions.

Environmental Sustainability

Many traditional drivers of economic growth, such as industrialization and increased consumption, can lead to significant environmental consequences, including pollution, resource depletion, and climate change. Sustainable economic growth seeks to balance economic progress with environmental protection.

Inflation

Rapid economic growth can sometimes lead to inflationary pressures if the demand for goods and services outstrips the economy’s ability to supply them. Central banks often manage monetary policy to control inflation.

The Role of Government

Governments play a crucial role in fostering economic growth through various policies, including investing in education and infrastructure, promoting research and development, ensuring macroeconomic stability, and implementing regulations that encourage fair competition and protect consumers and the environment.

Conclusion

In essence, economic growth is the engine that drives improvements in the material well-being of societies. It is a complex phenomenon driven by a combination of factors, from capital accumulation and technological innovation to institutional strength and the effective utilization of resources. While GDP serves as a primary indicator, a nuanced understanding requires considering per capita income, human development, and the qualitative aspects of progress. Navigating the challenges of inequality, environmental sustainability, and inflation is paramount to ensuring that economic growth translates into widespread and lasting prosperity for all.