In the intricate world of finance, managing future risks and securing prices for assets or commodities is paramount for businesses and investors alike. Among the myriad of derivative instruments designed for this purpose, the forward contract stands out as a fundamental yet highly versatile tool. At its core, a forward contract is a customized agreement between two parties to buy or sell an asset at a specified price on a future date. Unlike its more standardized cousin, the futures contract, forwards are typically over-the-counter (OTC) agreements, tailor-made to meet the specific needs of the contracting parties.

Understanding forward contracts is essential for anyone navigating global commerce, commodity markets, or even foreign exchange. They represent a critical mechanism for hedging against adverse price movements, allowing businesses to lock in costs or revenues, and enabling speculators to bet on future market directions. This exploration delves into the mechanics, applications, advantages, and challenges associated with forward contracts, highlighting their indispensable role in modern financial ecosystems driven by continuous technological advancements.

The Fundamentals of Forward Contracts

To truly grasp the significance of forward contracts, it’s crucial to first understand their basic construction and the elements that define them. These agreements are built upon a simple premise: two parties commit to a future transaction today, but the actual exchange of assets and cash occurs later.

Defining the Agreement

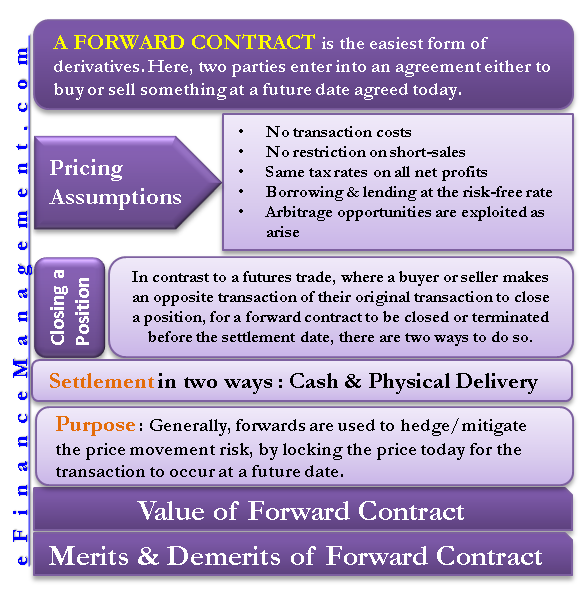

A forward contract is a legally binding agreement between a buyer and a seller to trade a specific asset at a predetermined price on a specified future date. This means that all the crucial terms – the asset, its quantity, the price, and the delivery date – are fixed at the inception of the contract. For instance, a coffee roaster might enter into a forward contract to buy 1,000 bags of coffee beans from a farmer in six months at a price of $X per bag. Regardless of whether the market price for coffee beans rises or falls over those six months, the roaster and the farmer are obligated to complete the transaction at $X per bag.

The primary objective for entering into such an agreement often stems from a desire to mitigate risk. The roaster hedges against a potential increase in coffee bean prices, ensuring stable input costs. The farmer, conversely, hedges against a potential decrease in prices, guaranteeing a certain revenue for their harvest. This mutual benefit for risk management forms the cornerstone of forward contract utility.

Key Characteristics and Underlying Assets

Forward contracts possess several distinguishing characteristics that differentiate them from other financial instruments. Their most prominent feature is their customization. Every aspect of a forward contract can be negotiated and tailored to the specific requirements of the parties involved. This flexibility extends to the size of the contract, the quality of the asset, the delivery location, and the precise settlement date.

The underlying assets for forward contracts are incredibly diverse. They can include:

- Commodities: Agricultural products (wheat, corn, coffee), energy (oil, natural gas), metals (gold, silver, copper).

- Currencies: Agreements to exchange one currency for another at a future date at a pre-agreed exchange rate. This is particularly common in international trade to hedge against foreign exchange risk.

- Interest Rates: Often used by financial institutions to lock in future interest rates.

- Equities: Agreements to buy or sell shares of a company at a future date.

Crucially, forward contracts are typically settled physically or in cash. Physical settlement involves the actual delivery of the underlying asset from the seller to the buyer. Cash settlement, on the other hand, involves the payment of the difference between the contract price and the market price of the asset on the settlement date, without the actual exchange of the asset itself. The choice of settlement method is also negotiated at the outset.

The Over-the-Counter Nature

Perhaps the most significant characteristic of forward contracts is their over-the-counter (OTC) nature. Unlike futures contracts which are traded on organized exchanges, forward contracts are privately negotiated between two parties or through a financial intermediary (like a bank). This direct negotiation is what allows for the high degree of customization mentioned earlier.

The OTC environment offers flexibility but also introduces certain implications. Because there is no central clearinghouse overseeing these transactions, forward contracts are subject to counterparty risk. This is the risk that one of the parties to the contract will default on their obligation before settlement. The absence of an exchange also means less transparency regarding prices and trading volumes compared to exchange-traded derivatives. However, the ability to create bespoke agreements often outweighs these concerns for participants seeking highly specific hedging solutions.

Strategic Applications and Market Dynamics

Forward contracts are not merely academic constructs; they are practical tools employed by a wide array of market participants for distinct strategic purposes. Their primary utility lies in managing exposure to price fluctuations, but they also serve as vehicles for speculative ventures.

Hedging Against Market Volatility

The most common and arguably most important application of forward contracts is hedging. Hedging is a strategy designed to reduce the risk of adverse price movements in an asset. For businesses engaged in international trade or commodity-dependent industries, locking in future prices can provide significant stability and predictability.

Consider an airline that needs to purchase jet fuel in six months. The price of oil is notoriously volatile. To protect against a potential spike in fuel costs, the airline could enter into a forward contract with an oil supplier or a financial institution to buy a specific quantity of jet fuel at a predetermined price in six months. If the market price of jet fuel rises significantly, the airline benefits from the lower, locked-in price. Conversely, if prices fall, the airline would have paid more than the market rate, but it achieved its primary goal: certainty of cost. This certainty allows for better financial planning and budget management, insulating the business from unpredictable market swings.

Similarly, a multinational corporation expecting to receive a large payment in a foreign currency in three months faces currency risk. If the foreign currency depreciates against its domestic currency, the value of the payment in domestic terms will decrease. By entering into a forward contract to sell the foreign currency at a fixed exchange rate in three months, the corporation eliminates this risk, ensuring a predictable domestic currency inflow.

Speculation and Market Participation

While hedging aims to reduce risk, forward contracts can also be used for speculation – profiting from anticipated price movements. A speculator who believes the price of a certain commodity or currency will increase in the future might enter into a forward contract to buy that asset at today’s agreed-upon price. If their prediction is correct, they can then buy the asset at the lower contract price and immediately sell it in the open market at the higher prevailing price, realizing a profit.

Conversely, a speculator expecting a price decrease could enter a forward contract to sell an asset at today’s agreed price. If the price indeed falls, they can acquire the asset at the lower market price and deliver it against their forward contract, making a profit. Speculators play a crucial role in financial markets by providing liquidity and helping to ensure efficient pricing. However, speculation inherently carries high risk, as incorrect predictions can lead to significant losses.

Understanding Counterparty Risk

The OTC nature of forward contracts makes counterparty risk a critical consideration. Unlike exchange-traded futures, which are guaranteed by a clearinghouse, forward contracts rely solely on the creditworthiness of the two parties involved. Counterparty risk is the risk that one party to the contract will fail to fulfill their obligation.

For example, if the coffee farmer in our earlier example faces financial distress and cannot deliver the beans, or if the roaster goes bankrupt and cannot pay, the contract may default. Mitigating counterparty risk often involves due diligence on the part of both parties, assessing the financial stability and reputation of their counterparty. In some cases, collateral requirements or credit support annexes (CSAs) might be included in the agreement, particularly when dealing with financial institutions. Financial intermediaries, such as large banks, often act as counterparties in forward contracts, leveraging their strong credit ratings to facilitate transactions for a wider range of clients.

Forward Contracts vs. Futures Contracts

While frequently discussed interchangeably due to their similar function, forward and futures contracts possess fundamental differences that dictate their usage and market environment. Both are agreements to buy or sell an asset at a predetermined price on a future date, but their structural and operational distinctions are significant.

Customization vs. Standardization

The most salient difference lies in their degree of customization. Forward contracts are highly customizable. Every term, including the asset quantity, quality, delivery location, and settlement date, can be individually negotiated between the two parties. This flexibility makes them ideal for hedging very specific, often unique, exposures.

In contrast, futures contracts are highly standardized. They specify a standard quantity and quality of the underlying asset, along with fixed delivery months and locations. This standardization is necessary because futures contracts are traded on organized exchanges. Traders buy and sell these uniform contracts, allowing for a liquid and transparent market. This means a company looking to hedge with futures must often adjust its exposure to fit the standardized contract sizes, which might not perfectly match its specific needs.

Settlement and Margin Requirements

Another key distinction is the settlement process and associated margin requirements. Futures contracts typically require participants to maintain a margin account with the exchange or broker. This involves depositing a certain amount of money (initial margin) and topping it up if losses occur (maintenance margin). The market-to-market process, where gains and losses are settled daily, ensures that large debts do not accumulate and significantly reduces counterparty risk.

Forward contracts, being private agreements, generally do not involve daily market-to-market adjustments or margin calls. Instead, the full obligation of the contract is typically settled on the expiration date. While this avoids the daily cash flow implications of margin calls, it concentrates the counterparty risk to the final settlement date, as discussed earlier. For this reason, assessing the creditworthiness of the counterparty is critical in forward contracts.

Regulatory Frameworks and Market Access

The environments in which these derivatives trade also differ significantly. Futures contracts are traded on regulated exchanges (e.g., CME Group, ICE Futures), which operate under strict regulatory oversight. This ensures price transparency, orderly trading, and reduced risk of manipulation. Anyone can access the futures market through a brokerage account, provided they meet certain financial requirements.

Forward contracts, as OTC instruments, are not traded on exchanges and are subject to less direct regulation. While large financial institutions that act as counterparties are heavily regulated, the individual forward agreements themselves are essentially private contracts. This lack of centralized oversight contributes to the customization but also means less transparency for the broader market and a greater reliance on bilateral trust and legal enforcement of the contract terms. Access to forward markets is typically through financial intermediaries, and often requires a pre-existing relationship and credit assessment.

Advantages, Disadvantages, and Real-World Examples

Forward contracts, like any financial instrument, come with a distinct set of benefits and drawbacks that users must carefully weigh before engaging. Their practical application spans various industries, providing tailored solutions for diverse risk management challenges.

Benefits for Risk Management and Flexibility

The primary advantage of forward contracts lies in their unparalleled flexibility and customization. Businesses can precisely tailor the contract terms—asset quantity, quality, delivery date, and location—to match their exact operational needs. This makes them highly effective for hedging specific, non-standard exposures that might not be addressable with standardized futures contracts. For instance, a small-scale farmer might negotiate a forward contract for a specific grade of grain unique to their region, something a major exchange might not list.

Furthermore, forward contracts can provide price certainty without the need for daily cash settlements associated with futures. For companies that prefer to avoid the unpredictable liquidity demands of margin calls, waiting until the settlement date for the full transaction can be an attractive feature for cash flow management. They also allow for direct negotiation, potentially leading to better terms for both parties in a bespoke deal.

Inherent Challenges and Considerations

Despite their benefits, forward contracts are not without their limitations and risks. The most significant is counterparty risk, as discussed. The absence of a central clearinghouse means that if the other party defaults, the non-defaulting party could suffer significant financial losses. This risk is particularly acute for smaller entities dealing with less financially robust counterparties.

Another disadvantage is the lack of liquidity. Because forward contracts are customized and privately negotiated, they cannot be easily sold or transferred to another party before their expiration. This illiquidity makes it difficult for a party to exit their position or adjust their hedge if market conditions or their needs change unexpectedly.

Finally, there is price discovery and transparency. In an OTC market, prices for forward contracts are not publicly disseminated in the same way as exchange-traded futures. This can make it challenging for parties to ensure they are getting a fair price, potentially leading to less optimal contract terms compared to a transparent, competitive exchange environment.

Practical Scenarios Across Industries

Forward contracts are ubiquitous in various sectors:

- Aviation: An airline locks in the price of jet fuel for its future operational needs, mitigating the impact of volatile oil prices.

- Agriculture: A grain elevator operator agrees to buy a farmer’s harvest at a fixed price upon delivery in several months, providing price certainty for both.

- Manufacturing: An electronics manufacturer enters a forward contract to purchase a specific quantity of rare earth metals from a supplier at a fixed price, safeguarding against supply chain disruptions and price hikes.

- International Trade: An importer agrees to buy goods from an overseas supplier, anticipating payment in Euros in three months. To hedge against the Euro weakening against their home currency, they enter a forward contract to sell Euros at a fixed rate for future delivery, ensuring predictable costs in their local currency.

The Evolving Landscape: Tech and Innovation in Forward Contracts

Even as a traditional financial instrument, forward contracts are not immune to the transformative power of technology and innovation. In an increasingly digitized global economy, technology plays a pivotal role in enhancing the efficiency, accessibility, and risk management associated with these agreements.

Digitalization and Efficiency

The rise of financial technology (FinTech) has significantly impacted how forward contracts are negotiated, executed, and managed. Digital platforms facilitate faster and more secure communication between parties, streamline the documentation process, and automate settlement procedures. Smart contract technology, leveraging blockchain, holds the potential to further revolutionize forward contracts by embedding agreement terms directly into code. This could automatically trigger settlement conditions, reduce reliance on intermediaries, and enhance transparency and immutability, thereby mitigating certain aspects of counterparty risk.

Electronic trading systems, while more common for futures, are also evolving to support the negotiation and execution of more complex, customized OTC derivatives. This allows for broader market access and potentially more competitive pricing, even for bespoke forward contracts.

Advanced Analytics and Risk Modeling

Modern technology also brings sophisticated analytical tools to the forefront of forward contract management. Advanced algorithms and machine learning models can process vast amounts of market data to provide more accurate price forecasts, enabling better decision-making for hedging and speculative strategies. These tools can also enhance risk modeling, allowing financial institutions and corporations to more precisely assess and manage their exposure to counterparty risk and market volatility.

Furthermore, regulatory technologies (RegTech) are being deployed to improve compliance and reporting for OTC derivatives. While forward contracts are less regulated than futures, authorities are increasingly seeking greater transparency in OTC markets to prevent systemic risks. Technology assists firms in meeting these evolving regulatory requirements, ensuring that the benefits of customization do not come at the expense of market stability. The innovation in data analytics also allows for better valuation of these non-standard contracts, addressing one of the inherent challenges of OTC products.

In conclusion, the forward contract remains a cornerstone of risk management and speculation in global financial markets. Its unique blend of customization and direct negotiation offers powerful benefits for specific hedging needs, though it demands careful consideration of counterparty risk and liquidity. As technology continues to advance, the landscape of forward contracts is evolving, with digitalization and advanced analytics enhancing their efficiency, accessibility, and resilience, ensuring their continued relevance in the future of finance.