Estate tax, often a misunderstood but crucial aspect of financial planning, refers to a tax levied on the transfer of a deceased person’s assets to their heirs. It’s not a tax on the income of the deceased during their lifetime, nor is it typically a tax on the inheritance received by the beneficiaries (that’s usually referred to as inheritance tax, which is distinct and levied by some states). Instead, estate tax is a tax on the gross estate – the total value of everything a person owned at the time of their death, before any debts, expenses, or exemptions are considered.

The “estate tax percentage” is therefore not a single, fixed rate that applies universally. It’s a complex calculation that depends on numerous factors, including the total value of the estate, applicable federal and state exemptions, deductions, and any specific tax laws in place at the time of death. Understanding this complexity is vital for effective estate planning, ensuring that assets are distributed according to one’s wishes with minimal tax burden.

Understanding the Fundamentals of Estate Tax

At its core, estate tax is a wealth transfer tax. It aims to prevent the indefinite accumulation of wealth within families and to generate revenue for the government. While it can sound daunting, it’s important to note that estate tax is a relatively narrow tax, impacting only a small percentage of the wealthiest estates in most jurisdictions.

Federal Estate Tax: The Primary Consideration

The federal estate tax is the most significant consideration for most individuals. The United States has a federal estate tax system with a high exemption threshold. This means that only estates exceeding a certain value are subject to this tax.

The Federal Exemption Amount and its Impact

The federal estate tax exemption is the amount of an estate that can be passed on to heirs without incurring federal estate tax. This exemption amount is adjusted annually for inflation. For example, in 2024, the federal estate tax exemption is $13.61 million per individual. This means that an individual can leave up to $13.61 million to their heirs tax-free at the federal level. For married couples, this exemption can effectively be doubled through proper estate planning, allowing them to pass on a combined $27.22 million tax-free.

Any portion of an estate that exceeds this exemption amount is subject to federal estate tax. The tax rates themselves are progressive, meaning that higher portions of the taxable estate are taxed at higher rates. Currently, the top federal estate tax rate is 40%.

Lifetime Gift Tax Exclusion

A crucial element linked to the federal estate tax is the lifetime gift tax exclusion. This exclusion allows individuals to gift assets to others during their lifetime without incurring gift tax. The amount of this lifetime exclusion is unified with the estate tax exemption. This means that any amount used for lifetime gifts reduces the amount available for the estate tax exemption at death. For instance, if someone gifts $5 million during their lifetime, their remaining estate tax exemption would be $8.61 million (using the 2024 exemption as an example). This provision encourages individuals to utilize their wealth during their lives while still providing tax-advantaged transfers.

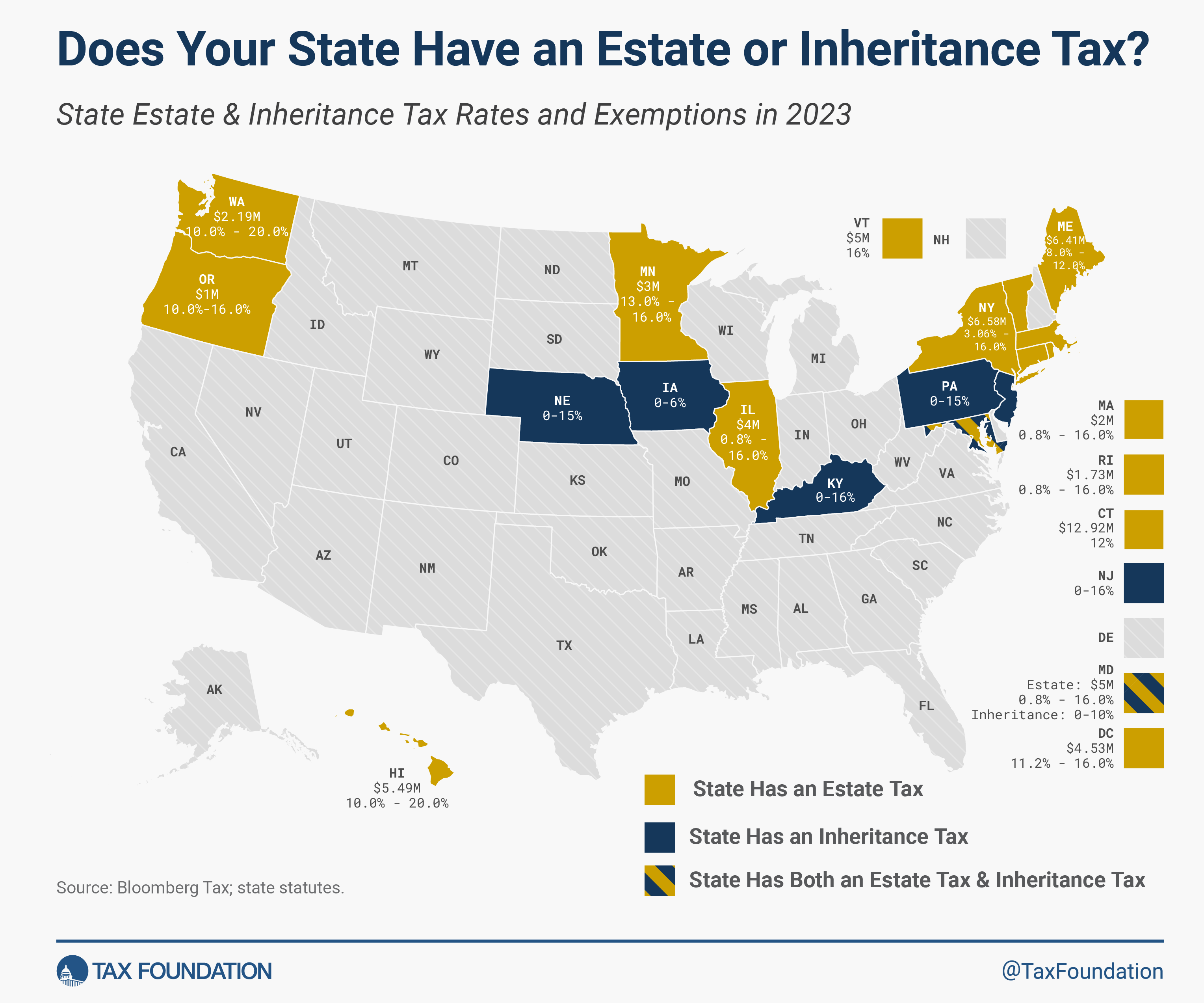

State Estate and Inheritance Taxes: A Layered Approach

Beyond the federal estate tax, many states have their own estate tax or inheritance tax laws. It’s crucial to understand that these are separate from the federal tax and operate independently.

State Estate Tax Variations

Some states impose their own estate tax, which is levied on the estate of a deceased resident or on property within the state owned by a non-resident. These state estate taxes often have much lower exemption thresholds than the federal estate tax. For example, a state might have an estate tax exemption of $1 million or even less. This means that an estate that is not subject to federal estate tax might still be liable for state estate tax. The tax rates also vary significantly by state, with some states having progressive rates similar to the federal system, while others may have flat rates.

The Distinction of Inheritance Tax

Inheritance tax, on the other hand, is levied on the heirs who receive assets from an estate. The tax is based on the value of the inheritance and the relationship of the heir to the deceased. Close relatives, such as spouses and children, often receive preferential tax treatment or are exempt entirely, while more distant relatives or unrelated beneficiaries may face higher tax rates. Only a handful of states currently impose an inheritance tax. It’s essential to research the specific laws of the state where the deceased was a resident and where beneficiaries reside to understand potential inheritance tax liabilities.

Calculating the Estate Tax Percentage: A Multi-faceted Process

Determining the actual “estate tax percentage” is far from a simple multiplication problem. It involves a thorough valuation of assets, careful consideration of deductions, and an understanding of applicable tax brackets.

Step 1: Determining the Gross Estate Value

The first and most critical step is to accurately value all assets owned by the deceased at the time of their death. This includes a wide range of assets:

- Real Estate: Homes, land, commercial properties. Valuations are typically based on fair market value, often determined by professional appraisals.

- Financial Assets: Stocks, bonds, mutual funds, bank accounts, retirement accounts (IRAs, 401(k)s – the value of which may be taxable depending on the account type and beneficiary).

- Personal Property: Vehicles, jewelry, art, collectibles, furniture. Again, appraisals may be necessary for significant items.

- Business Interests: Ownership stakes in private or public companies.

- Life Insurance Proceeds: If the deceased owned the life insurance policy or had incidents of ownership, the death benefit is typically included in the gross estate.

- Other Assets: Any other property of value, such as intellectual property rights or digital assets.

Step 2: Identifying Allowable Deductions

Once the gross estate is determined, certain deductions can be subtracted to arrive at the taxable estate. These deductions are crucial for reducing the overall tax liability.

- Debts and Expenses: Mortgages, credit card debts, personal loans, and final expenses such as funeral costs and burial expenses are deductible.

- Administrative Expenses: Costs associated with settling the estate, including legal fees, accounting fees, appraisal fees, and executor fees, can also be deducted.

- Marital Deduction: This is a significant deduction that allows unlimited transfers of assets to a surviving spouse, either outright or through certain types of trusts, without incurring estate tax. This is a powerful tool for deferring estate tax until the death of the surviving spouse.

- Charitable Deduction: Bequests made to qualified charitable organizations are fully deductible, providing an incentive for philanthropic giving.

Step 3: Applying Exemptions and Calculating Tax

After subtracting all allowable deductions, the result is the taxable estate. This is the amount on which estate tax is calculated.

- Federal Tax Calculation: For federal estate tax, the taxable estate is first considered against the applicable federal exemption amount. If the taxable estate exceeds the exemption, tax is calculated on the excess amount using the progressive federal tax rates, with a top rate of 40%.

- State Tax Calculation: If the estate is subject to state estate tax, a separate calculation is performed based on the state’s specific exemption thresholds and tax rates. The state tax is calculated on the value of the estate that exceeds the state exemption, after considering any state-level deductions.

- Inheritance Tax Calculation (if applicable): If an inheritance tax applies, the tax is calculated on the value of the assets received by each individual beneficiary, with rates often varying based on their relationship to the deceased.

The “estate tax percentage” isn’t a single number but rather the effective tax rate that results from these complex calculations. It’s the total tax paid divided by the total value of the taxable estate, or in some analyses, the total tax paid divided by the gross estate.

Strategies to Mitigate Estate Tax Liability

While estate tax is a reality for some, proactive estate planning can significantly reduce or even eliminate the tax burden on your heirs.

Gifting Strategies During Lifetime

As mentioned, the lifetime gift tax exclusion is a powerful tool. By strategically gifting assets during your lifetime, you can reduce the size of your taxable estate at death. This is particularly effective for substantial wealth, as it allows you to transfer assets while they are still growing, potentially avoiding future estate tax on that growth.

Utilizing Trusts

Various types of trusts can be instrumental in estate tax planning.

- Irrevocable Trusts: These trusts, once established, cannot be altered or revoked. Assets transferred into an irrevocable trust are generally removed from the grantor’s taxable estate. Common examples include:

- Irrevocable Life Insurance Trusts (ILITs): These trusts can own life insurance policies, preventing the death benefit from being included in the grantor’s estate.

- Grantor Retained Annuity Trusts (GRATs): These allow for the transfer of appreciating assets to beneficiaries with minimal gift or estate tax.

- Dynasty Trusts: These are designed to last for multiple generations, providing long-term asset protection and tax deferral.

- Marital Trusts: For married couples, various marital trusts, such as bypass trusts (also known as credit shelter trusts) and qualified terminable interest property (QTIP) trusts, can effectively utilize both spouses’ estate tax exemptions, allowing for the transfer of a larger amount of assets tax-free.

Charitable Giving Strategies

For those with philanthropic intentions, charitable giving can serve a dual purpose. Bequests to qualified charities are tax-deductible, reducing the taxable estate. Furthermore, more complex charitable giving vehicles like Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) can provide income to beneficiaries for a period while ultimately benefiting a charity, offering tax advantages along the way.

Strategic Use of Portability

For married couples, the concept of “portability” is crucial. It allows the surviving spouse to utilize any unused portion of the deceased spouse’s federal estate tax exemption. This means that a surviving spouse can potentially access both their own exemption and their deceased spouse’s unused exemption, significantly increasing the amount that can be passed on tax-free. However, portability must be elected on a timely filed estate tax return (Form 706) by the deceased spouse’s executor.

The Evolving Landscape of Estate Tax

Estate tax laws are not static. They are subject to changes in legislation, economic conditions, and political priorities.

Legislative Changes and Future Projections

Congress periodically reviews and adjusts estate tax laws. The exemption amounts, tax rates, and available deductions can all be modified. For instance, the significantly higher federal estate tax exemption that has been in place in recent years is scheduled to revert to lower levels at the end of 2025 unless Congress acts to extend the current provisions. This constant flux underscores the importance of staying informed and working with experienced estate planning professionals.

The Importance of Professional Guidance

Navigating the intricacies of estate tax requires specialized knowledge. Attempting to plan without professional assistance can lead to costly mistakes, unintended tax consequences, and a failure to achieve your estate planning goals.

- Estate Planning Attorneys: These legal professionals can advise on wills, trusts, and other legal instruments necessary for effective estate transfer.

- Certified Public Accountants (CPAs) and Enrolled Agents (EAs): These financial experts can help with tax calculations, compliance, and strategizing to minimize tax liabilities.

- Financial Advisors: They can assist in assessing your overall financial picture, valuing assets, and developing investment strategies that align with your estate planning objectives.

By understanding the fundamentals of estate tax, the methods of calculation, and the available strategies for mitigation, individuals can take proactive steps to ensure their legacy is preserved and passed on efficiently to their loved ones. The “estate tax percentage” is not a fixed number but a variable outcome of meticulous planning and adherence to the ever-evolving tax landscape.