Understanding Electronic Funds Transfer and its Role in the Digital Economy

The modern financial landscape is increasingly dominated by digital transactions, and at the heart of many of these exchanges lies Electronic Funds Transfer (EFT). EFT is a broad term encompassing a variety of methods by which money is moved electronically from one bank account to another. While often used interchangeably with terms like direct debit or online payments, EFT represents the overarching technological framework enabling these conveniences. This article will delve into the intricacies of EFT debit, exploring its definition, mechanisms, benefits, security considerations, and its profound impact on both consumers and businesses.

The Mechanics of EFT Debit: How Your Money Moves

At its core, an EFT debit transaction is initiated when a payer (an individual or business) authorizes a payee (another individual or business) to withdraw funds directly from their bank account. This authorization is crucial and forms the bedrock of all EFT debit transactions. Unlike credit card transactions where the cardholder initiates a payment each time, EFT debit typically involves a standing authorization, often referred to as a “mandate” or “direct debit agreement.”

Initiating the Debit: The Payer’s Authorization

The process begins with the payer granting permission to the payee to debit their account. This authorization can take several forms:

- Written Mandate: Historically, this involved signing a physical form authorizing recurring or one-off debits.

- Verbal Authorization: In many jurisdictions, a clear verbal agreement, often recorded for verification purposes, can suffice for initiating direct debits.

- Online Authorization: The most common method today involves agreeing to terms and conditions online, often during a checkout process or when setting up recurring payments for services. This usually involves providing bank account details (account number and sort code/routing number) and confirming the debit authorization through a secure portal.

Once authorized, the payee submits a request to their bank, outlining the amount to be debited and the payer’s bank account details. This request is then processed through a clearing system, typically managed by financial institutions and payment networks.

The Clearing and Settlement Process

The journey of an EFT debit transaction involves several key steps within the banking system:

- Initiation: The payee’s bank receives the debit instruction and sends it to the relevant clearing house or payment network.

- Verification: The clearing house routes the instruction to the payer’s bank for verification. This involves checking if the account exists, has sufficient funds, and if the debit authorization is valid.

- Authorization/Rejection: If all checks pass, the payer’s bank authorizes the debit. If there are insufficient funds or an invalid authorization, the transaction is typically rejected, and the payer may incur fees.

- Settlement: Once authorized, the funds are transferred from the payer’s account to the payee’s account, often through a series of interbank transfers facilitated by the central bank or payment system. This settlement can occur in real-time or in batches, depending on the payment network.

The speed of EFT debit transactions can vary. Some systems offer near real-time processing, while others may take a few business days to complete. This speed is often a key differentiator between various EFT methods.

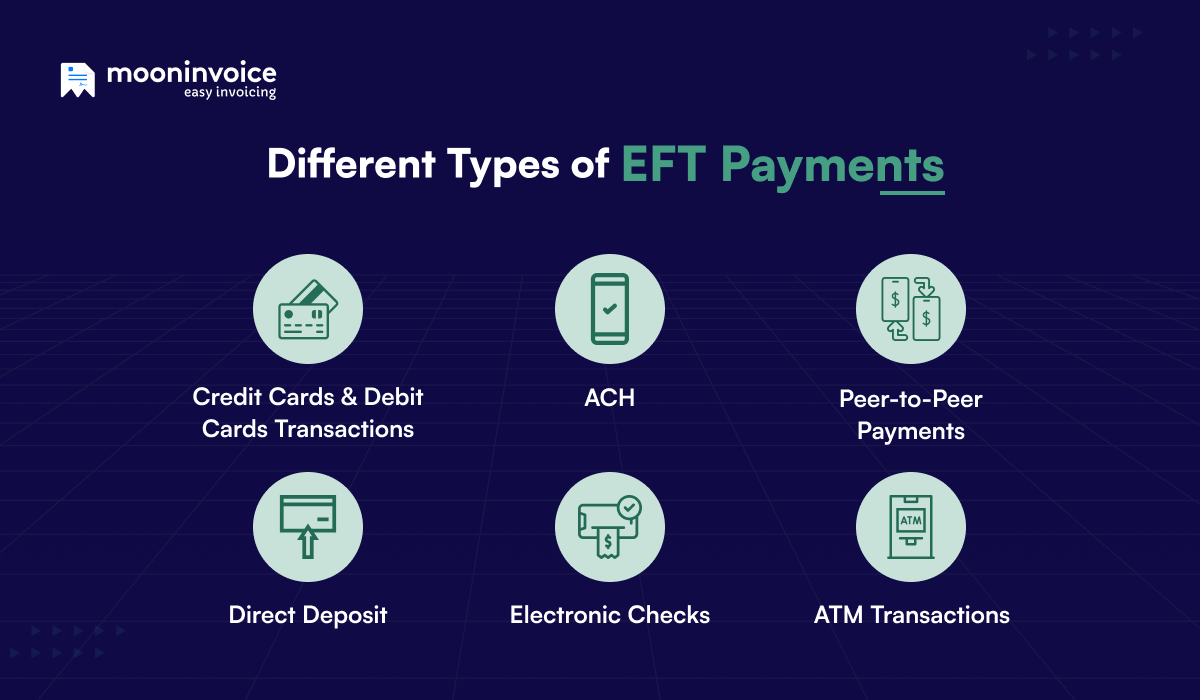

Types of EFT Debit Transactions

The umbrella term “EFT debit” encompasses a range of specific transaction types, each serving different purposes:

Recurring Payments

This is perhaps the most prevalent use of EFT debit. It involves a pre-authorized agreement for regular withdrawals from a payer’s account to a payee’s account. Common examples include:

- Utility Bills: Electricity, gas, water, and internet providers often utilize EFT debit for monthly bill payments.

- Loan Repayments: Mortgages, car loans, and personal loan installments are frequently debited automatically.

- Subscription Services: Streaming services, gym memberships, and software subscriptions rely heavily on recurring EFT debits to ensure seamless service continuity.

- Rent and Lease Payments: Landlords and property management companies often arrange for rent to be debited from tenants’ accounts.

The primary advantage of recurring EFT debit for both parties is predictability and convenience. Payers avoid late fees and the hassle of manual payments, while payees ensure consistent cash flow.

One-Off Payments

While recurring payments are common, EFT debit can also be used for single, one-time transactions. This is often seen in situations where a customer purchases a product or service and agrees to have the payment debited directly from their bank account at the point of sale, rather than using a credit or debit card. This is particularly useful for:

- Online Purchases: Some e-commerce platforms offer EFT debit as a payment option for immediate purchases.

- Service Agreements: When agreeing to a specific service, like a one-time repair or consultation, EFT debit can be used for immediate payment.

- Donations: Charities and non-profit organizations may offer EFT debit for one-time donations.

Payroll Direct Deposit

While technically an EFT credit to the employee’s account, the underlying mechanism of EFT is vital here. Employers use EFT to deposit salaries and wages directly into employees’ bank accounts, eliminating the need for paper checks. This streamlines payroll processing for businesses and provides a secure and convenient way for employees to receive their earnings.

Benefits of EFT Debit for Consumers and Businesses

The widespread adoption of EFT debit is driven by a multitude of benefits for both individuals and organizations:

For Consumers:

- Convenience: Eliminates the need to remember payment due dates, write checks, or manually initiate payments each time.

- Time-Saving: Frees up time that would otherwise be spent on managing and making payments.

- Avoidance of Late Fees: Ensures timely payments, thereby avoiding costly late charges.

- Budgeting Aid: Predictable outflows can simplify budgeting and financial planning.

- Security: Reduces the risk associated with carrying cash or mailing checks.

For Businesses:

- Improved Cash Flow: Predictable and timely receipt of funds leads to more stable and reliable cash flow.

- Reduced Administrative Costs: Automates payment collection, significantly lowering costs associated with invoicing, chasing payments, and processing checks.

- Increased Efficiency: Streamlines accounts receivable processes, allowing staff to focus on more strategic tasks.

- Enhanced Customer Relationships: Offers a convenient payment option that can improve customer satisfaction and reduce payment friction.

- Reduced Risk of Bad Debt: Direct debit payments are generally more secure than other payment methods, reducing the risk of non-payment.

- Environmental Benefits: Reduces paper usage and transportation associated with traditional payment methods.

Security and Fraud Prevention in EFT Debit

While EFT debit offers numerous advantages, security and fraud prevention are paramount. Financial institutions and regulatory bodies have implemented robust measures to protect both payers and payees.

Key Security Measures:

- Strong Authentication: For online authorizations, multi-factor authentication (MFA) is increasingly used to verify the payer’s identity.

- Encryption: Data transmitted during EFT transactions is encrypted to prevent interception and tampering.

- Tokenization: Sensitive bank account details are often replaced with unique tokens, so the actual account number is not stored or transmitted directly.

- Regulatory Oversight: EFT systems are subject to strict regulations and compliance standards (e.g., PSD2 in Europe, NACHA rules in the US) that dictate security protocols and consumer protection rights.

- Consumer Protection Rights: In many regions, consumers have specific rights regarding direct debits. This often includes the ability to cancel a direct debit at any time and a “Direct Debit Guarantee” that protects against unauthorized or incorrect debits, providing a mechanism for refunds.

- Monitoring and Auditing: Banks and payment processors constantly monitor transactions for suspicious activity and conduct regular audits to ensure compliance and identify potential vulnerabilities.

Despite these measures, fraud can still occur. Common types of EFT debit fraud include:

- Unauthorized Debits: Where a payee debits an account without proper authorization. This can be due to identity theft or outright fraudulent schemes.

- Phishing Scams: Where fraudsters trick individuals into revealing their bank account details and authorization codes.

- Account Takeover: Where a fraudster gains access to a legitimate account and initiates fraudulent debits.

It is crucial for consumers to remain vigilant, regularly review their bank statements, and report any suspicious transactions immediately to their bank. Businesses must also implement strong internal controls to prevent internal fraud and ensure proper authorization processes are followed.

The Future of EFT Debit: Innovation and Integration

The evolution of EFT debit is far from over. Emerging technologies and evolving consumer expectations are shaping its future:

- Real-Time Payments (RTP): The push towards instant payment systems means that EFT debit transactions could become truly instantaneous, with funds available to the payee within seconds.

- Open Banking and APIs: Application Programming Interfaces (APIs) associated with open banking initiatives are enabling greater integration of EFT debit capabilities into various platforms and applications, making payments even more seamless.

- Biometric Authentication: The use of fingerprints, facial recognition, and other biometric data for authorizing payments is likely to become more prevalent, enhancing security and user experience.

- Artificial Intelligence (AI) and Machine Learning (ML): AI and ML are being used to detect fraudulent transactions more effectively and to personalize payment experiences for consumers.

- Cross-Border EFT: Efforts are underway to make cross-border EFT debit more efficient and cost-effective, further facilitating global commerce.

In conclusion, EFT debit is a fundamental pillar of the modern digital economy, enabling a vast array of financial transactions with unparalleled convenience and efficiency. From recurring bills to online purchases and payroll, its impact is pervasive. As technology continues to advance, EFT debit will undoubtedly become even more sophisticated, secure, and integrated into our daily financial lives, reinforcing its role as a cornerstone of seamless, electronic commerce.