In the realm of personal finance and everyday transactions, two ubiquitous plastic rectangles often find themselves in our wallets: the credit card and the debit card. While they may look strikingly similar and often serve the same primary purpose – facilitating purchases – their underlying mechanisms, implications, and the way they interact with your money are fundamentally different. Understanding these distinctions is not merely an academic exercise; it’s crucial for informed financial decision-making, effective budgeting, and safeguarding your financial well-being. This exploration delves into the core differences between credit cards and debit cards, shedding light on their operational principles, benefits, drawbacks, and the strategic considerations that should guide their usage.

The Core Mechanism: How They Work

At their heart, credit cards and debit cards represent distinct financial relationships between the cardholder, a financial institution (usually a bank), and the merchant. The fundamental difference lies in the source of funds used for a transaction.

Debit Cards: Accessing Your Own Money

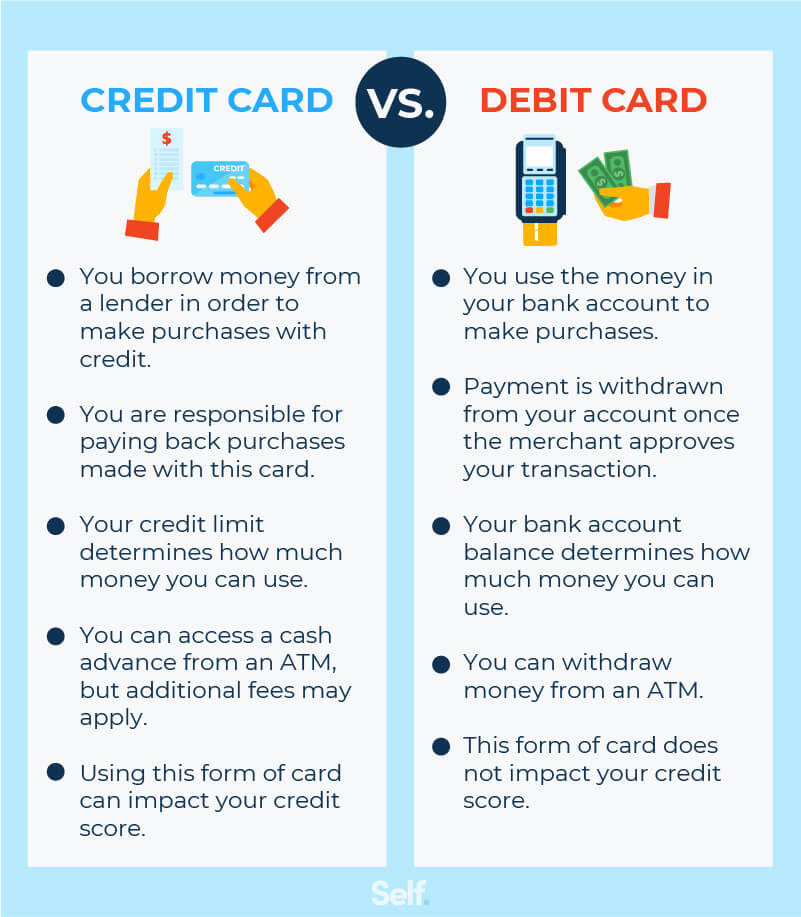

A debit card is directly linked to your checking account or savings account. When you swipe, insert, or tap your debit card for a purchase, the funds are immediately deducted from your available balance in that account. It’s akin to writing a check or withdrawing cash; you are spending money that you already possess. The transaction is processed in real-time, and your account balance is updated accordingly, typically within a few business days, though often appearing as pending immediately.

Direct Account Linkage

The defining characteristic of a debit card is its direct tether to a bank account. This linkage means that the spending limit is inherently constrained by the amount of money currently held within that account. If you attempt a purchase that exceeds your available balance, the transaction will likely be declined, unless you have opted for overdraft protection, which typically incurs fees.

Transaction Processing

When a debit card transaction is initiated, a request is sent to your bank through a payment network (like Visa or Mastercard). The bank verifies if sufficient funds are available in your account. If they are, the funds are authorized and then transferred from your account to the merchant’s account. This process is generally swift, making debit cards convenient for everyday spending.

Credit Cards: Borrowing Funds

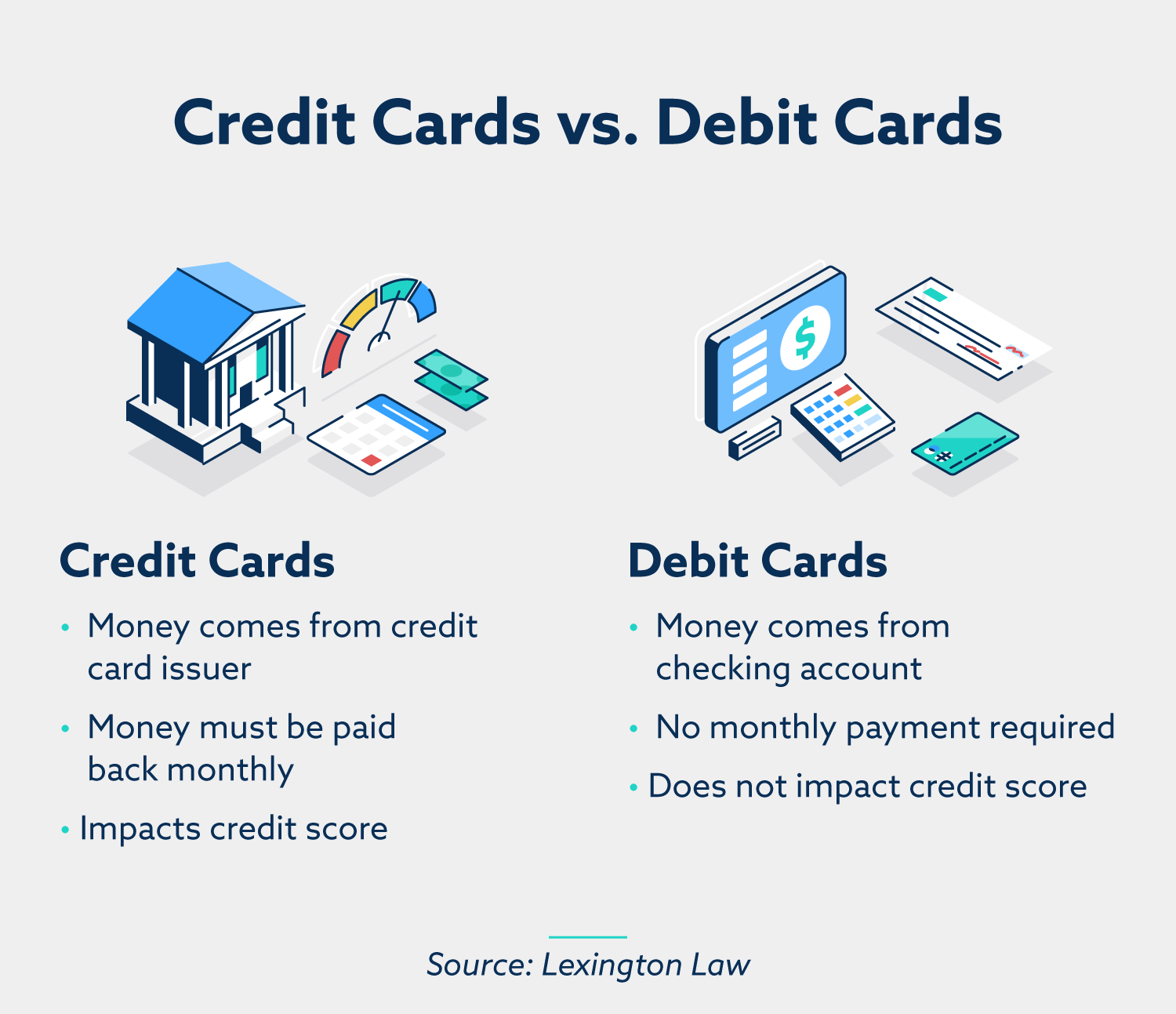

A credit card, on the other hand, allows you to borrow money from the card issuer (a bank or financial institution) up to a pre-approved credit limit to make purchases. When you use a credit card, you are essentially taking out a short-term loan. The issuer pays the merchant on your behalf, and you are then obligated to repay the borrowed amount to the credit card company.

Pre-approved Credit Limit

Credit card issuers evaluate your creditworthiness before extending credit. Based on factors like your credit history, income, and debt-to-income ratio, they establish a credit limit – the maximum amount you can borrow on the card. This limit provides a buffer, allowing you to make purchases even if you don’t have the immediate funds available.

Repayment Obligation and Interest

Unlike debit cards, credit card purchases do not immediately deplete your bank account. Instead, you receive a monthly statement detailing your purchases and the total amount owed. You have the option to pay the entire balance by the due date to avoid interest charges, or you can make a minimum payment and carry the remaining balance over to the next billing cycle. If you carry a balance, you will be charged interest, calculated based on your Annual Percentage Rate (APR). This interest can significantly increase the cost of your purchases over time.

Key Distinctions and Implications

Beyond their fundamental operational differences, credit and debit cards diverge in several critical areas that impact user experience, financial health, and consumer protection.

Financial Impact and Debt

Debit Cards: Preventing Debt

Because debit cards draw directly from your existing funds, they are an excellent tool for preventing debt accumulation. Spending is limited by your available balance, which encourages responsible spending habits and helps users stay within their budgetary means. There’s no risk of accruing interest charges or falling into a debt spiral if used prudently.

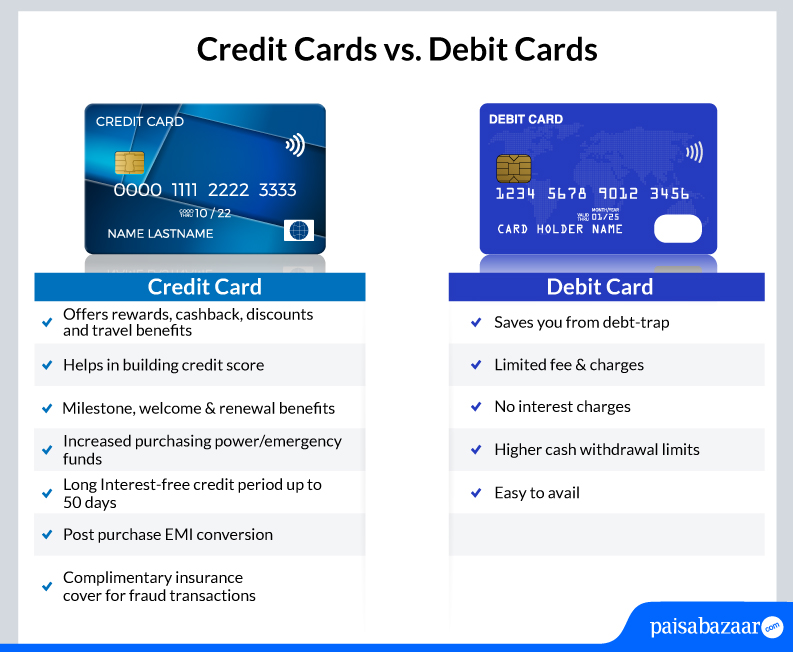

Credit Cards: Building Credit and Potential Debt

Credit cards offer a powerful mechanism for building credit history. Responsible usage – making timely payments and keeping credit utilization low – can significantly improve your credit score, which is vital for securing loans, mortgages, and even renting an apartment. However, this same feature, if misused, can lead to substantial debt. High-interest rates on unpaid balances can make it difficult to escape a cycle of debt, impacting long-term financial stability.

Fees and Charges

Debit Card Fees

Debit cards generally have fewer fees associated with them compared to credit cards. Common fees might include ATM withdrawal fees (especially if using an out-of-network ATM), overdraft fees if you spend more than you have in your account and have opted for this service, and sometimes monthly maintenance fees for the associated checking account.

Credit Card Fees

Credit cards can come with a wider array of fees. These often include annual fees (especially for premium rewards cards), late payment fees, over-limit fees (though less common now due to regulations), foreign transaction fees for purchases made outside your home country, balance transfer fees, and cash advance fees. The most significant “fee” for many users, however, is the interest charged on balances that are not paid in full each month.

Consumer Protections and Fraud Liability

Debit Card Protections

Consumer protections for debit cards are present but can be less robust than for credit cards. Under U.S. law (the Electronic Fund Transfer Act), your liability for unauthorized transactions on a debit card is limited, but it depends on how quickly you report the loss or theft. If you report it before any unauthorized transactions occur, you generally have no liability. If you report it within two business days of learning about the loss or theft, your maximum liability is $50. If you report it between two and sixty business days, your liability can be up to $500. Reporting after sixty business days could mean unlimited liability. It’s crucial to act swiftly.

Credit Card Protections

Credit cards generally offer stronger consumer protections. Under the Fair Credit Billing Act (FCBA) in the U.S., your liability for unauthorized charges on a credit card is capped at $50, and most major credit card issuers have a $0 liability policy for fraudulent activity. This means if your card is stolen and used fraudulently, you typically won’t have to pay for those unauthorized charges. Furthermore, credit cards offer dispute resolution processes, allowing you to contest charges for goods or services that were not delivered or were misrepresented.

Rewards and Benefits

Debit Card Rewards

Debit cards typically offer very limited or no rewards programs. Some may offer minor cash-back incentives or points tied to specific retailers, but these are far less common and less lucrative than credit card rewards.

Credit Card Rewards

Credit cards are often a primary tool for earning rewards. These can include:

- Cash Back: A percentage of your spending returned to you as cash or statement credit.

- Travel Rewards: Points or miles that can be redeemed for flights, hotel stays, car rentals, and other travel expenses.

- Points Programs: Flexible points that can be redeemed for a variety of rewards, including merchandise, gift cards, travel, and statement credits.

- Perks and Benefits: Many credit cards offer additional benefits such as travel insurance, purchase protection, extended warranties, airport lounge access, and concierge services, particularly for premium cards.

Strategic Use and Financial Planning

The choice between using a credit card or a debit card, or how to strategically combine them, depends heavily on individual financial habits, goals, and risk tolerance.

For Budgeting and Spending Control

Debit Card for Strict Budgeting

If your primary financial goal is to stick to a rigid budget and avoid any form of debt, a debit card is the most straightforward choice. It ensures you only spend money you actually have, acting as a natural brake on impulsive purchases. It’s an excellent tool for students, individuals working to overcome debt, or anyone who finds managing finances challenging.

Credit Card as a Spending “Enforcer” (with discipline)

While counterintuitive, a credit card can also be used for strict budgeting, provided there is unwavering discipline. By treating your credit card like a debit card – only spending what you can afford to pay off in full by the due date – you can still control your spending. The benefit here is the potential to earn rewards and build credit while maintaining budgetary control. However, this requires a high level of self-control and a clear understanding of your financial limits.

For Building Credit and Improving Financial Standing

Credit Card is Essential

For anyone looking to build or improve their credit score, a credit card is indispensable. A good credit score is a cornerstone of financial health, enabling access to better loan terms, lower interest rates, and greater financial opportunities. Responsible credit card usage is the most direct and accessible way to achieve this.

Debit Card’s Limited Role

Debit cards do not contribute to building credit history because they do not involve borrowing. While essential for daily transactions, they play no role in credit building.

For Large Purchases and Emergencies

Credit Card for Flexibility and Protection

For significant purchases or unexpected emergencies, a credit card can offer crucial flexibility. It allows you to make the purchase or cover the emergency expense even if immediate funds are not readily available. The added benefit of purchase protection and extended warranties on many credit cards can provide peace of mind for expensive items. If managed responsibly, you can pay down the balance over time, potentially with manageable interest if you can secure a low APR or a 0% introductory offer.

Debit Card for Immediate Cash Needs

If you need immediate cash access for an emergency where credit isn’t an option or desired, a debit card allows you to withdraw funds from your checking account at an ATM, subject to daily withdrawal limits.

Conclusion

The distinction between credit cards and debit cards is profound, extending far beyond their superficial appearance. Debit cards offer a direct connection to your own funds, promoting disciplined spending and debt avoidance, making them ideal for day-to-day budgeting. Credit cards, conversely, leverage borrowed funds, providing the opportunity to build credit, earn rewards, and gain robust consumer protections, but at the potential cost of debt and interest if not managed with strict financial discipline. Understanding these differences empowers individuals to make informed choices, leverage the unique advantages of each card type, and ultimately navigate their financial journey with greater confidence and security. The optimal approach often involves a strategic combination of both, utilizing debit cards for predictable expenses and credit cards for strategic financial growth and benefit acquisition, all while maintaining a firm grip on one’s budgetary responsibilities.