In the complex landscape of estate planning, the terms “will” and “trust” are often used interchangeably, leading to confusion about their distinct purposes and functionalities. While both are essential tools for managing the distribution of assets after death, they operate under fundamentally different legal frameworks and offer varying degrees of control, privacy, and efficiency. Understanding these differences is crucial for individuals seeking to ensure their wishes are honored, their loved ones are provided for, and their estate is managed with minimal complication. This exploration delves into the core distinctions between wills and trusts, examining their creation, administration, probate implications, privacy, and flexibility, ultimately providing clarity for informed decision-making in safeguarding one’s legacy.

The Fundamental Nature of Wills and Trusts

At their core, wills and trusts serve the overarching goal of asset distribution. However, their operational timelines and the legal mechanisms they employ diverge significantly.

Wills: A Testament to Intent

A will is a legal document that outlines how an individual (the testator) wishes for their property and assets to be distributed after their death. It is a directive, becoming effective only upon the testator’s demise. A will can also name guardians for minor children, specify funeral wishes, and appoint an executor to oversee the estate’s administration.

Key characteristics of a will include:

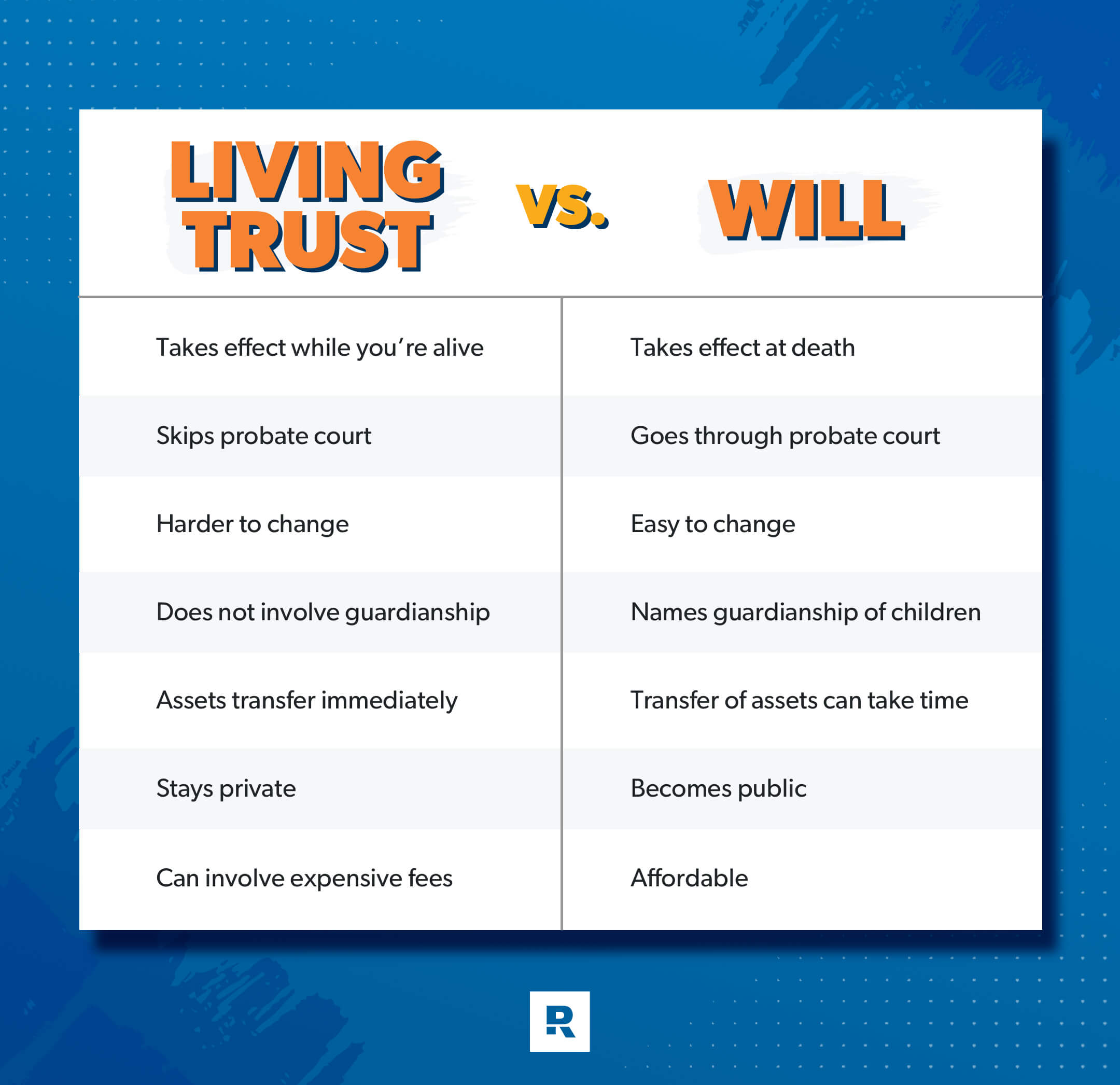

- Testamentary Effect: A will only takes legal effect after the testator’s death. Until that point, it can be altered or revoked by the testator.

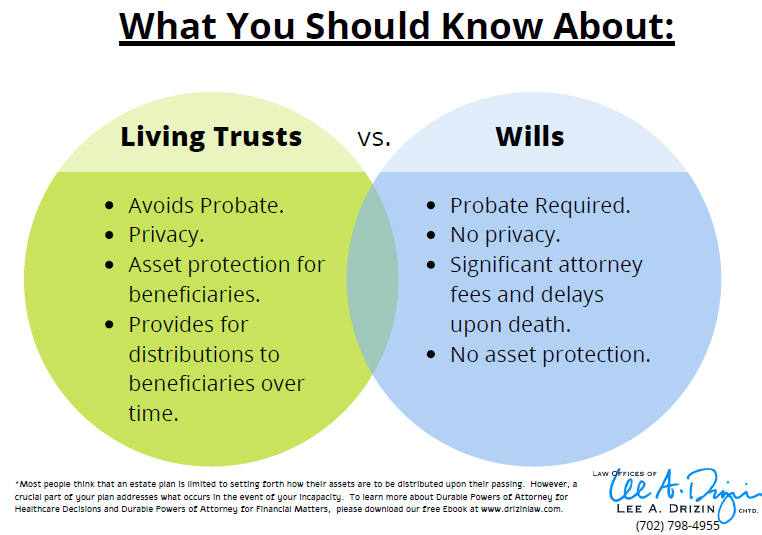

- Probate Requirement: In most jurisdictions, a will must undergo a legal process known as probate. Probate is a court-supervised procedure that validates the will, settles debts and taxes, and distributes the remaining assets to the beneficiaries. This process can be time-consuming, costly, and public.

- Public Record: Once filed with the probate court, a will becomes a public document, accessible to anyone. This means details about the testator’s assets, beneficiaries, and distribution plans are publicly available.

- Appointment of Executor: A will designates an executor, who is responsible for carrying out the testator’s instructions, including gathering assets, paying debts, and distributing property.

- Guardianship Nomination: For individuals with minor children, a will is the primary document for nominating guardians who will care for them in the event of the parents’ death.

Trusts: A Living Arrangement for Assets

A trust, on the other hand, is a legal arrangement where a grantor (or settlor) transfers assets to a trustee, who then manages these assets for the benefit of designated beneficiaries. Unlike a will, a trust can be established and become effective during the grantor’s lifetime. This distinction allows trusts to serve a broader range of purposes, including asset management, probate avoidance, and ongoing wealth preservation.

Key characteristics of a trust include:

- Inter Vivos (Living) Trusts: These trusts are created and become effective during the grantor’s lifetime. They can be revocable or irrevocable.

- Revocable Trusts: The grantor retains control over the assets and can modify or revoke the trust at any time. Assets in a revocable trust typically do not avoid estate taxes but do avoid probate.

- Irrevocable Trusts: Once established, the grantor generally relinquishes control over the assets, and the trust cannot be easily modified or revoked. These trusts can offer benefits in terms of estate tax reduction and asset protection.

- Testamentary Trusts: These trusts are created through a will and only become effective after the testator’s death and the will has gone through probate. Their primary purpose is to manage assets for beneficiaries according to the terms set forth in the will.

- Probate Avoidance (for Living Trusts): Assets properly transferred into a living trust (revocable or irrevocable) during the grantor’s lifetime bypass the probate process entirely. This leads to a faster, more private, and often less expensive distribution of assets.

- Privacy: Trusts are generally private documents. The terms of a trust, its assets, and its beneficiaries are not typically made public, offering a significant advantage in terms of privacy compared to a will.

- Ongoing Management: Trusts can be structured to provide for the ongoing management and distribution of assets over an extended period, even for generations, offering greater flexibility in how beneficiaries receive their inheritance.

Probate: The Crucial Differentiator

Perhaps the most significant functional difference between a will and a living trust lies in their interaction with the probate process.

The Probate Landscape for Wills

When an individual dies with a valid will, the executor must initiate probate proceedings. This process typically involves:

- Filing the Will: The will is submitted to the appropriate probate court.

- Appointment of Executor: The court officially appoints the named executor or, if none is named or qualified, appoints an administrator.

- Notification of Heirs and Creditors: Beneficiaries and known creditors are formally notified of the probate proceedings.

- Inventory and Appraisal of Assets: The executor must identify, gather, and appraise all assets belonging to the deceased’s estate.

- Payment of Debts and Taxes: Outstanding debts, funeral expenses, and any applicable estate or inheritance taxes are paid from the estate’s assets.

- Distribution of Remaining Assets: Once all obligations are settled, the remaining assets are distributed to the beneficiaries according to the terms of the will.

The probate process can be lengthy, often taking several months to over a year, depending on the complexity of the estate and court dockets. It can also incur substantial costs, including court fees, attorney fees, appraiser fees, and executor fees, all of which reduce the net value of the inheritance. Furthermore, the public nature of probate means that financial details of the estate and its beneficiaries become part of the public record.

Trusts and Probate Avoidance

Assets held within a properly funded living trust (revocable or irrevocable) bypass the probate process altogether. When the grantor of a living trust dies, the successor trustee, as named in the trust document, takes over management and distribution of the trust assets according to the trust’s provisions. This process is generally:

- Faster: Without the court’s involvement, asset distribution can occur much more quickly, often within weeks or months.

- More Private: The terms of the trust and the distribution of assets remain confidential, shielded from public scrutiny.

- Less Expensive: While there are costs associated with setting up and administering a trust, these are typically lower than the cumulative costs of probate, especially for larger or more complex estates.

- Continuity of Management: For assets that require ongoing management (e.g., rental properties, businesses), a trust ensures seamless continuation of operations without interruption.

It is important to note that even if an individual has a living trust, they should still have a “pour-over will.” This type of will ensures that any assets not specifically transferred into the trust during the grantor’s lifetime are “poured over” into the trust upon death, thus going through probate but ultimately being distributed according to the trust’s terms.

Privacy and Control: A Tale of Two Documents

The level of privacy and the degree of control over assets before and after death are significant considerations when choosing between a will and a trust.

Wills and Public Disclosure

As previously mentioned, wills become public documents once they enter probate. This means that anyone can access information about the deceased’s assets, debts, and who inherits what. For individuals who value discretion and wish to keep their financial affairs private, this public disclosure can be a considerable drawback. The specific details of family financial matters, gifts to specific individuals, or charitable contributions become readily available to the general public.

Trusts and Confidentiality

Living trusts, in contrast, are private legal instruments. The details of the trust, including the assets it holds, the beneficiaries, and the distribution plan, remain confidential among the trustee, beneficiaries, and legal counsel. This privacy is particularly beneficial for individuals with substantial wealth, those who wish to avoid potential disputes among beneficiaries, or those who simply prefer their financial matters to remain their own.

Control During Life and After Death

- Wills: While a will clearly dictates how assets will be distributed after death, it offers no control over those assets during the testator’s lifetime. The testator can freely manage, sell, or gift their assets as they see fit.

- Revocable Trusts: A revocable living trust provides a unique blend of control and future planning. During the grantor’s lifetime, they typically serve as the trustee and can manage, invest, and even revoke the trust, retaining full control over the assets. Upon their incapacitation or death, the successor trustee steps in to manage and distribute the assets according to the trust’s instructions, providing a mechanism for seamless management without court intervention.

- Irrevocable Trusts: These trusts involve a relinquishing of control. Once assets are transferred into an irrevocable trust, the grantor generally loses the ability to alter or revoke the trust or reclaim the assets. This loss of control is often a trade-off for benefits like estate tax reduction and asset protection from creditors.

Flexibility and Special Circumstances

Both wills and trusts offer varying degrees of flexibility, particularly when addressing complex family situations or specific asset management needs.

Wills for Guardianship and Basic Distribution

Wills are the primary legal document for appointing guardians for minor children. This is a critical function that trusts cannot directly fulfill. Wills are also effective for straightforward asset distribution to adult beneficiaries who are capable of managing their inheritance.

Trusts for Complex Beneficiary Needs and Asset Management

Trusts offer significantly more flexibility in managing and distributing assets, especially for beneficiaries who may require specialized care or ongoing financial support. Examples include:

- Spendthrift Trusts: These trusts protect beneficiaries from their own poor financial management by restricting their access to the principal and controlling how and when funds are distributed.

- Special Needs Trusts: These trusts are designed to provide for a disabled individual’s needs without jeopardizing their eligibility for government benefits like Supplemental Security Income (SSI) or Medicaid.

- Minors’ Trusts: While a will can appoint guardians, a trust can manage and distribute assets for minors over a longer period, with specific instructions on how the funds should be used for their education, healthcare, or general well-being.

- Charitable Trusts: These trusts allow for planned giving to charitable organizations, often providing tax benefits to the grantor.

- Asset Protection: Certain types of trusts, particularly irrevocable ones, can shield assets from creditors and legal judgments.

Conclusion: A Complementary Relationship

In conclusion, while both wills and trusts are indispensable tools in estate planning, they serve distinct roles and offer different advantages. A will is a fundamental document for appointing guardians, expressing final wishes, and directing asset distribution, but it typically requires probate and becomes a public record. Living trusts, on the other hand, excel at probate avoidance, offering privacy and streamlined asset management, and can provide sophisticated mechanisms for managing and distributing assets over time.

For many individuals, the most robust estate plan involves both a will and a trust. A well-drafted will can act as a safety net, ensuring that any assets inadvertently left out of the trust are still distributed according to one’s wishes through a pour-over provision. The decision of whether to prioritize a will, a trust, or a combination of both should be made in consultation with an experienced estate planning attorney who can assess individual circumstances, goals, and financial situations to create a comprehensive and effective plan for safeguarding one’s legacy.